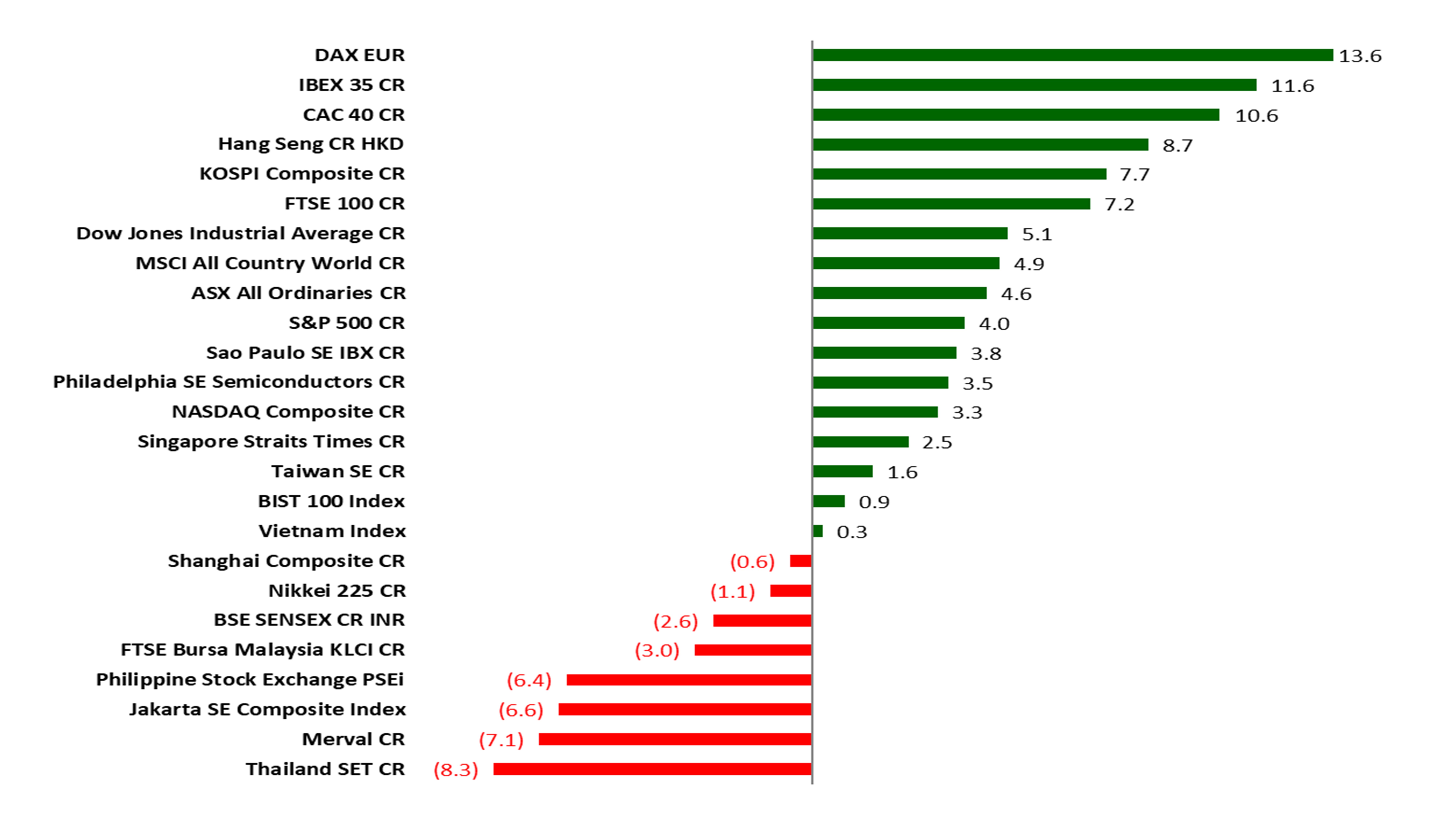

According to LSEG Lipper’s statistics, as of February 14th 2025, European stocks have been soaring, with gains surpassing those of U.S. stocks and other major global markets. In less than two months, the German stock market has risen by 13.6% while Spain soared by 11.6%, France by 10.6%, and the UK stock market has also seen a rise of 7.2%.

European Market Analysis

In terms of fundamentals, the European economy is not performing well, and it can even be said to be lackluster. Germany, the largest economy in the Eurozone, has been severely impacted by both the manufacturing and construction sectors. According to data from the Federal Statistical Office of Germany (Destatis), Germany’s GDP is expected to decline by 0.3% in 2023 and again by 0.2% in 2024, marking two consecutive years of economic recession. The economic difficulties in Germany stem from its heavy reliance on the U.S. market, exports to China, and an over-dependence on Russian natural gas to sustain industrial operations. The Ifo Institute for Economic Research has warned that if Germany does not implement economic policy reforms, it will struggle to escape stagnation by 2025. Goldman Sachs believes that the tariff war initiated by Trump will damage Europe’s economic standing, with Germany being particularly vulnerable. It is estimated that Germany’s economy can grow by at most 0.5% this year, significantly lower than the previous estimate of 0.9%. After the collapse of Chancellor Scholz’s “traffic light coalition,” he failed to pass a confidence vote in parliament. Germany is scheduled to hold elections on February 23 of this year. According to a poll by the German polling agency INSA, the largest opposition party, the Christian Democratic Union, is leading significantly with a support rate of 30%. Its leader, Friedrich Merz, is very likely to become the new Chancellor of Germany. The far-right Alternative for Germany (AfD) party also has a high support rate of 22%, making it the second-largest party in Germany, while Scholz’s Social Democratic Party has only 15.5% support.

Since last summer, France has been in a state of political turmoil due to President Macron’s decision to call for early elections. Prime Minister Barnier resigned after a budgetary no-confidence motion was passed. Macron has faced pressure from both the left and the far-right, which has at times left him constrained. According to the National Institute of Statistics and Economic Studies (INSEE), buoyed by the upcoming Paris Olympics, France’s GDP is expected to grow by 1.1% for the entire year. The newly appointed French Prime Minister Francois Bayrou has also survived a no-confidence motion, and the national budget for this year has finally been passed amidst significant challenges, leading to a stabilization of the political situation in France. However, due to potential deterioration in the job market, GDP estimates for the first and second quarters of this year may only reach 0.2%.

The European Central Bank (ECB) has revised its forecast for the Eurozone’s consumer price index (CPI) this year from an initial estimate of 2.5% down to 2.4%, and for next year, it has been further downgraded from 2.2% to 2.1%. Additionally, the GDP expectations for this year and next have been lowered by 0.1% and 0.2% to 0.7% and 1.1%, respectively. Despite the lackluster economic performance, the slowdown in inflation has led to a more decisive and clear path of interest rate cuts in Europe compared to the U.S. Federal Reserve. On January 30, the ECB lowered its benchmark deposit rate by 25 basis points to 2.75%, marking the fifth rate cut since June of last year. Recent statements from ECB officials suggest that inflation in the Eurozone is expected to gradually ease by 2025, and the economic growth outlook for the Eurozone is relatively weak and stagnant compared to the U.S., indicating that the ECB may further cut rates, with expectations of two more reductions to bring the rate to a neutral level between 1.75% and 2.25%. In the UK, the inflation rate in December slowed to an annual increase of 2.5%, below market expectations, and the Bank of England also cut rates by 25 basis points to 4.5% on February 6, which will help promote economic growth and provide liquidity to the stock market.

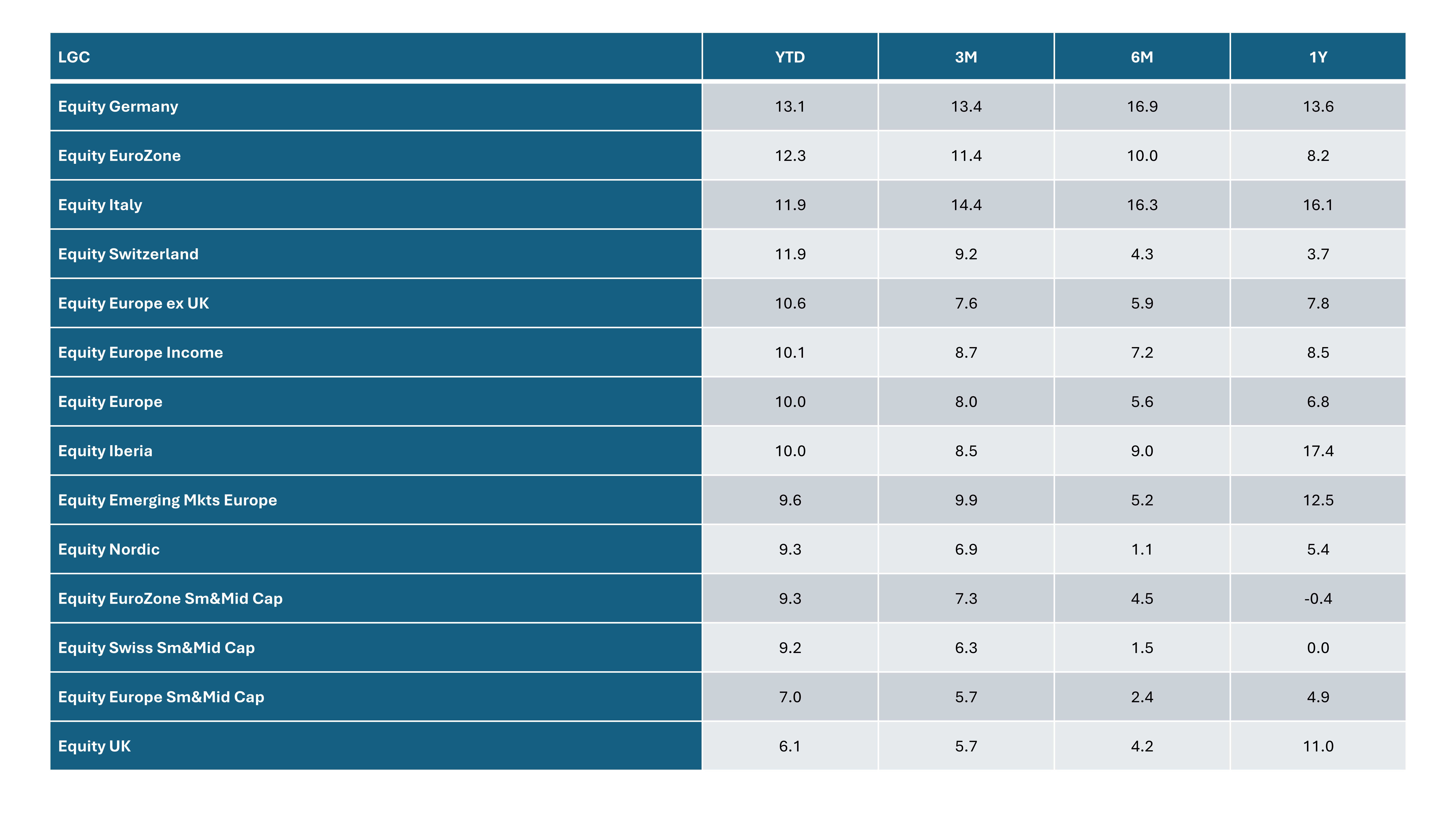

European Funds RFS Taiwan Performance Analysis

According to LSEG Lipper’s statistics, there are many types of actively managed European equity funds registered for sale in Taiwan. Among them, Equity Germany have achieved an outstanding average performance of 13.1% for the year-to-date period (as of 2025/2/14), while Equity Eurozone, Italy and Swiss posted an average performance of 12.3%, 11.9% and 11.9%, respectively. Equity Euro posted an average performance of 10%, and Equity UK posted an average performance of 5.1%.

All types of European equity funds RFS in Taiwan

source: LSEG Lipper, as of 2025/2/14

Outlook

The U.S. economy remains strong, leading to a surge in demand for high-value products such as machinery, equipment, vehicles, and high-tech goods from Europe. If high tariffs are implemented, European exporters will face significant cost pressures, particularly in the automotive and machinery sectors, which will be the most directly affected. However, after imposing a 25% tariff on steel and aluminum imports, Trump stated that he would impose reciprocal tariffs on all countries that levy tariffs on the U.S., but he is considering exempting reciprocal tariffs for industries such as automobiles and pharmaceuticals. As a result, European stocks have reacted positively. Nevertheless, investors should be aware that these tariff policies may prompt a restructuring of global supply chains, potentially weakening the competitiveness of the EU manufacturing sector. The rise in import prices will drive up overall prices in the Eurozone, significantly increasing imported inflationary pressures and posing challenges to the European Central Bank’s monetary policy.