The European fund industry enjoyed inflows over the course of December 2024.

These inflows occurred in a mainly positive market environment. While most equity markets were on the rise despite the high valuations of the market leaders over the course of the month, some bond segments faced the impacts from rising rates as yield curves have somewhat started to normalize. This might also be the reason why investors are somewhat nervous and reacting quickly on any news that may impact the current market environment negatively. That said, the election of Donald Trump as the next U.S. president had a positive impact on the U.S. equity market and the U.S. dollar.

That said, investors are not only focusing on economic news, as the increasing geopolitical tensions in the Middle East—especially the developments around the Red Sea—are seen as a risk for the general economic growth in Western countries since these tensions have the potential to drive up the price of oil. In addition, a number of shipping companies these days avoid the passage of the Suez channel. It is, therefore, to be expected that prolonged delivery times will cause some tensions for the still vulnerable delivery chains.

Market sentiment was also further driven by the expectations of investors for future central bank decisions. Since the different regions of the world are showing different growth patterns, investors expect less activity from the U.S. Federal Reserve, while they expect much more interest rate cuts from the European Central Bank. As a result, such different central bank activity may lead to a stronger U.S. dollar compared to the euro and other leading currencies. With regard to this, any statement from the Fed and other central banks may have the power to move the bond market in one or the other direction. In addition, fears of increasing debt in the U.S. might be the driver for further increasing interest rates on the long end of the yield curve, which hold back inflows into medium and long-term bond ETFs, while the still inverted yield curves might be the drivers for the inflows into money market ETFs.

That said, inverted yield curves and especially long-term inverted yield curves are seen as an early indicator for a possible recession. However, there are no signs for a recession in the U.S. and most other major economies visible yet. But even as it looks like the yield curves are slowly normalizing, this does not mean that there is no recession possible in the major economies around the globe. This is especially true as some major economies lack economic growth and may need lower interest rates as stimulus. Despite these headwinds, the positive effects of lower interest rates seem to be more important for investors than the current state of some economies.

Mutual funds (+€28.8 bn) and ETFs (+€31.3 bn) enjoyed inflows for the month. In fact, the flows into ETFs in December 2024 marked a new all-time high for monthly inflows into these products in Europe. This flow pattern led to overall estimated net inflows of €60.2 bn over the course of December 2024.

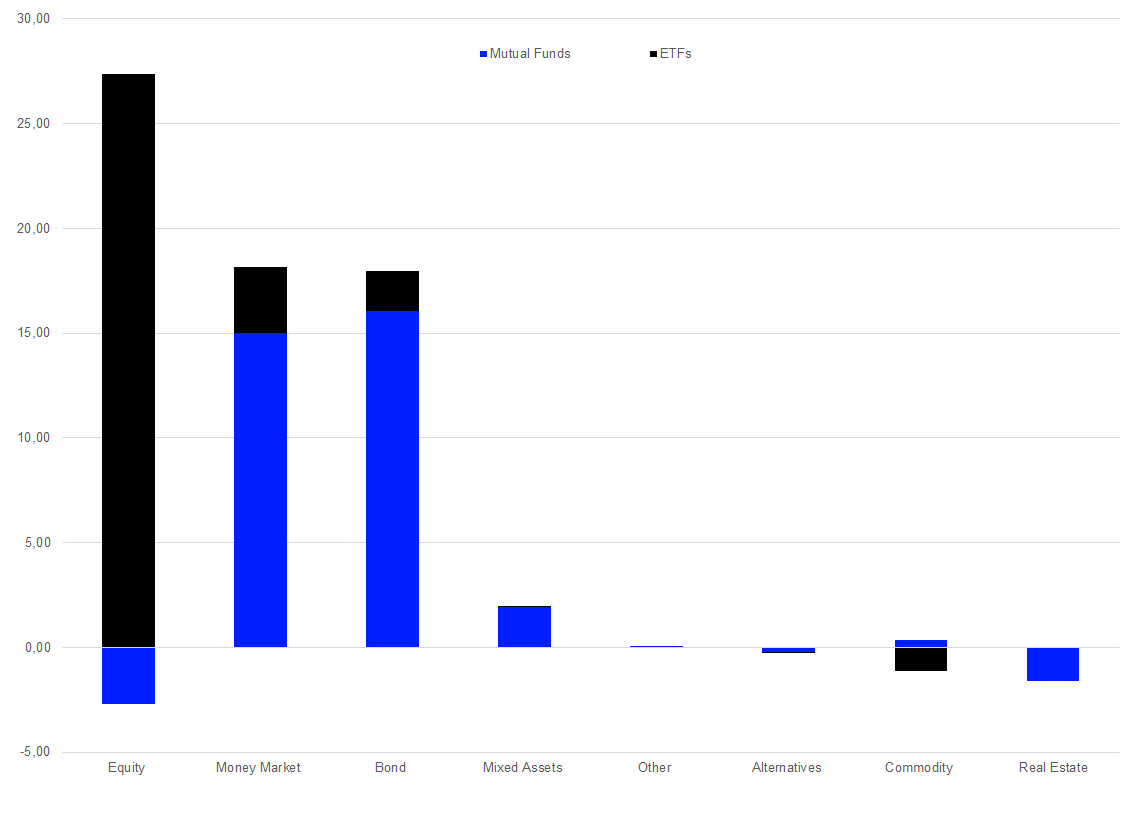

Asset Type Flows December 2024

In more detail, equity funds (+€24.7 bn) were the best-selling asset type overall for December 2024. The category was followed by money market funds (+€18.2 bn), bond funds (+€18.0 bn), mixed-assets funds (+€2.0 bn), and “other” funds (+€0.03 bn), while alternatives funds (-€0.3 bn), commodities funds (-€0.8 bn), and real estate funds (-€1,6 bn) faced outflows.

Graph 1: Estimated Net Flows by Asset and Product Type – December 2024 (in bn EUR)

Source: LSEG Lipper

Asset Type Flows Year to Date

The flow pattern for December drove the estimated overall net flows in the European fund industry up to €620.2 bn for the year 2024 so far.

On closer inspection, mutual funds (+€363.9 bn) and ETFs (+€256.4 bn) enjoyed inflows over the course of 2024. That said, the inflows into ETFs over the course of 2024 mark a new all-time-high for annual inflows into ETFs in Europe. Nevertheless, these inflows within a positive but still somewhat uncertain market environment are not considered unusual and might be a sign that European investors are somewhat in risk-on mode.

With regard to the still somewhat inverted yield curves for the Eurozone and other major economies in the world, it is somewhat surprising that European investors favored bond products over the course of the year. That said, the inflows into bonds might be seen as a sign that European investors adjusted their portfolios to the new environment with regard to the interest rate policies of central banks around the globe since the major central banks have further lowered their interest rates despite somewhat different economic environments in the respective regions/countries.

Overall, long-term investment products (+€345.9 bn) and money market funds (+€274.4 bn) enjoyed inflows for the year so far. That said, the estimated net flows for equities were dominated by the inflows into ETFs, while the inflows into bond and money market funds were dominated by mutual funds.

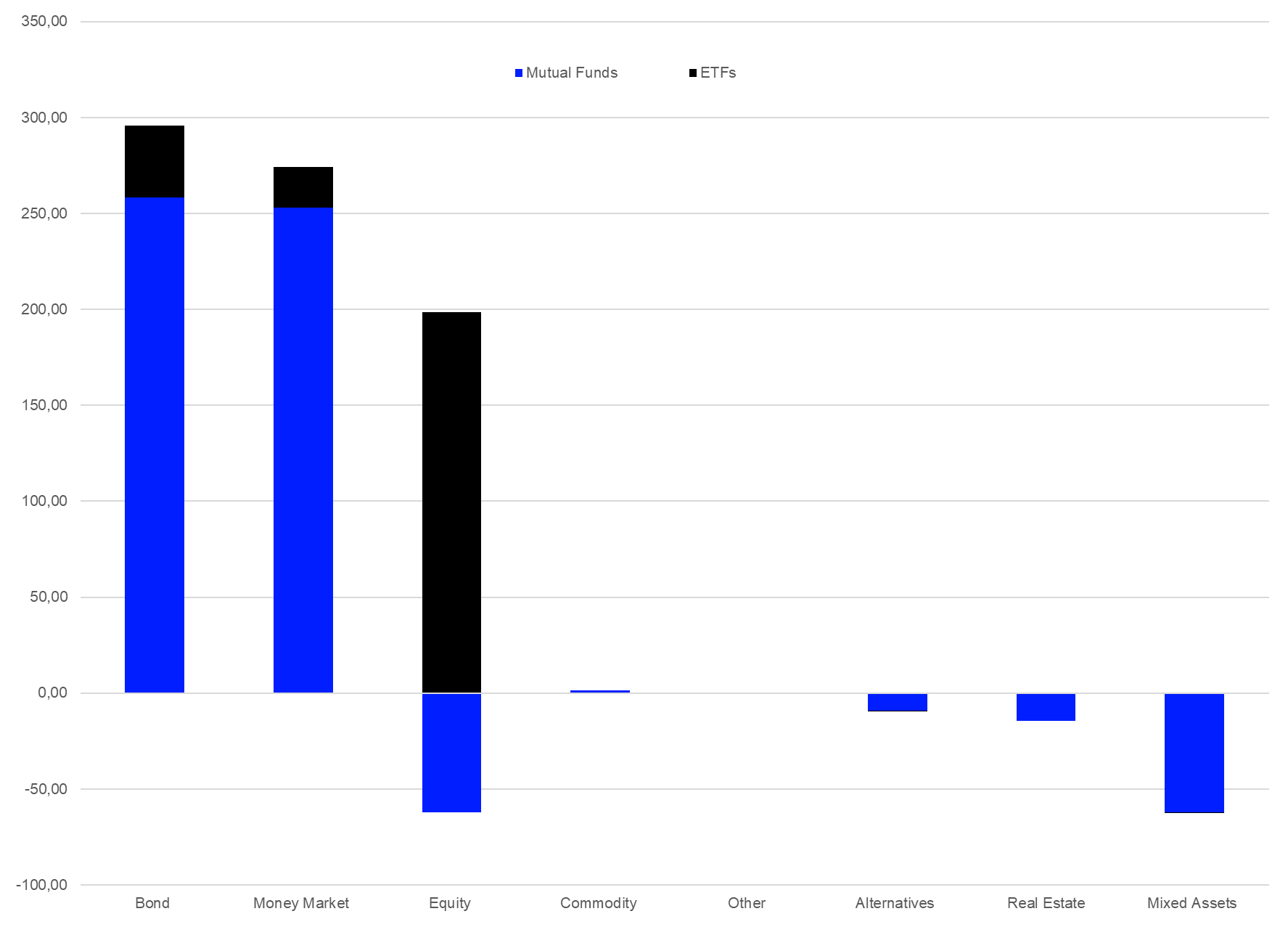

Taking a closer look, bond funds (+€295.9 bn) were the asset type with the highest estimated net inflows overall for 2024. It is followed by money market funds (+€274.4 bn), equity funds (+€136.3 bn), and commodities funds (+€0.8 bn). On the other side of the table, “other” funds (-€0.1 bn), alternatives funds (-€9.7 bn), real estate funds (-€14.7 bn), and mixed-assets funds (-€66.7 bn) faced outflows for the year so far.

Graph 2: Estimated Net Sales by Asset and Product Type, January 1 – December 31, 2024 (Euro Billions)

Source: LSEG Lipper

The high outflows from mixed-assets funds might be caused by investors who used fixed-income funds to achieve their income goals during the low interest rate environment, switching their market exposure back to bonds given the current interest rate environment.

In addition, one needs to bear in mind that the flows in money market products are impacted by a combination of asset allocation decisions of portfolio managers and corporate actions such as cash dividends or cash payments since money market funds are also used by corporations as replacements for cash accounts.

Given the still somewhat inverted yield curves, it can be assumed that a number of investors use money market products as a replacement for cash accounts, and in some cases even bonds, since money market products offer a comparably high yield within the current interest rate environment. Therefore, it can be expected that the inflows in money market products may revert once the yield curves have normalized.

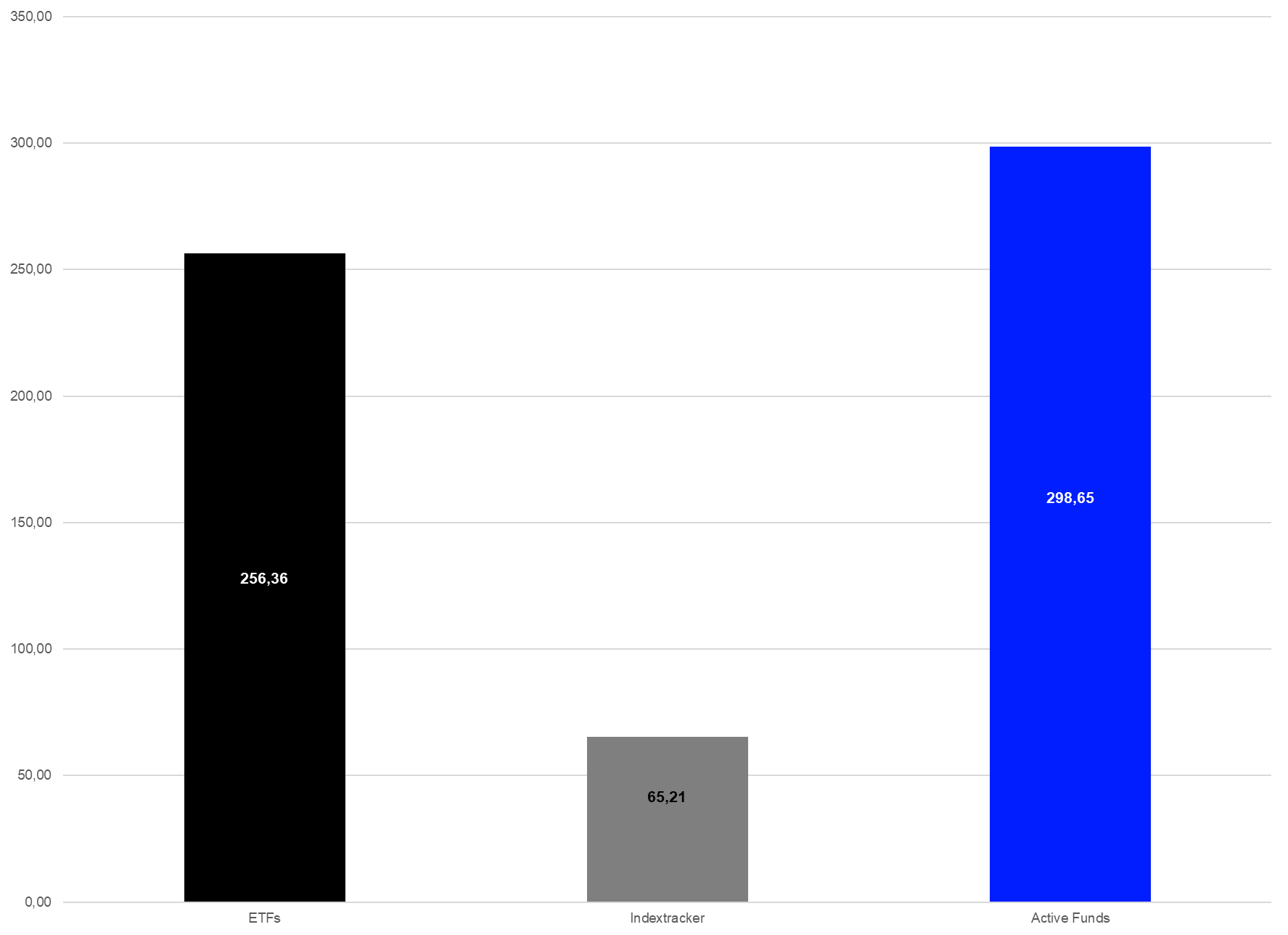

Fund Flows Active vs Passive Products

The trend toward passive investment vehicles is widely discussed by market observers and asset managers, so it is worthwhile to highlight this topic, especially as not all passive products are ETFs. In fact, the flows into ETFs (+€256.4 bn) were outpacing the flows into passive index mutual funds (+€65.2 bn) by a large margin. In line with this, actively managed long-term mutual funds had inflows of €47.0 bn for 2024.

Graph 3: Estimated Net Flows by Management Approach and Product Type (January 1 – December 31, 2024)

Source: LSEG Lipper

Some market observers may speculate that European investors are selling actively managed equity products and buying back passive products, especially within the Lipper global classification Equity U.S. Generally speaking, one could agree with this thesis by looking at the high-level numbers, but since this can’t be proven by facts I would not totally agree with this assumption.

Fund Flows by Lipper Global Classifications, December 2024

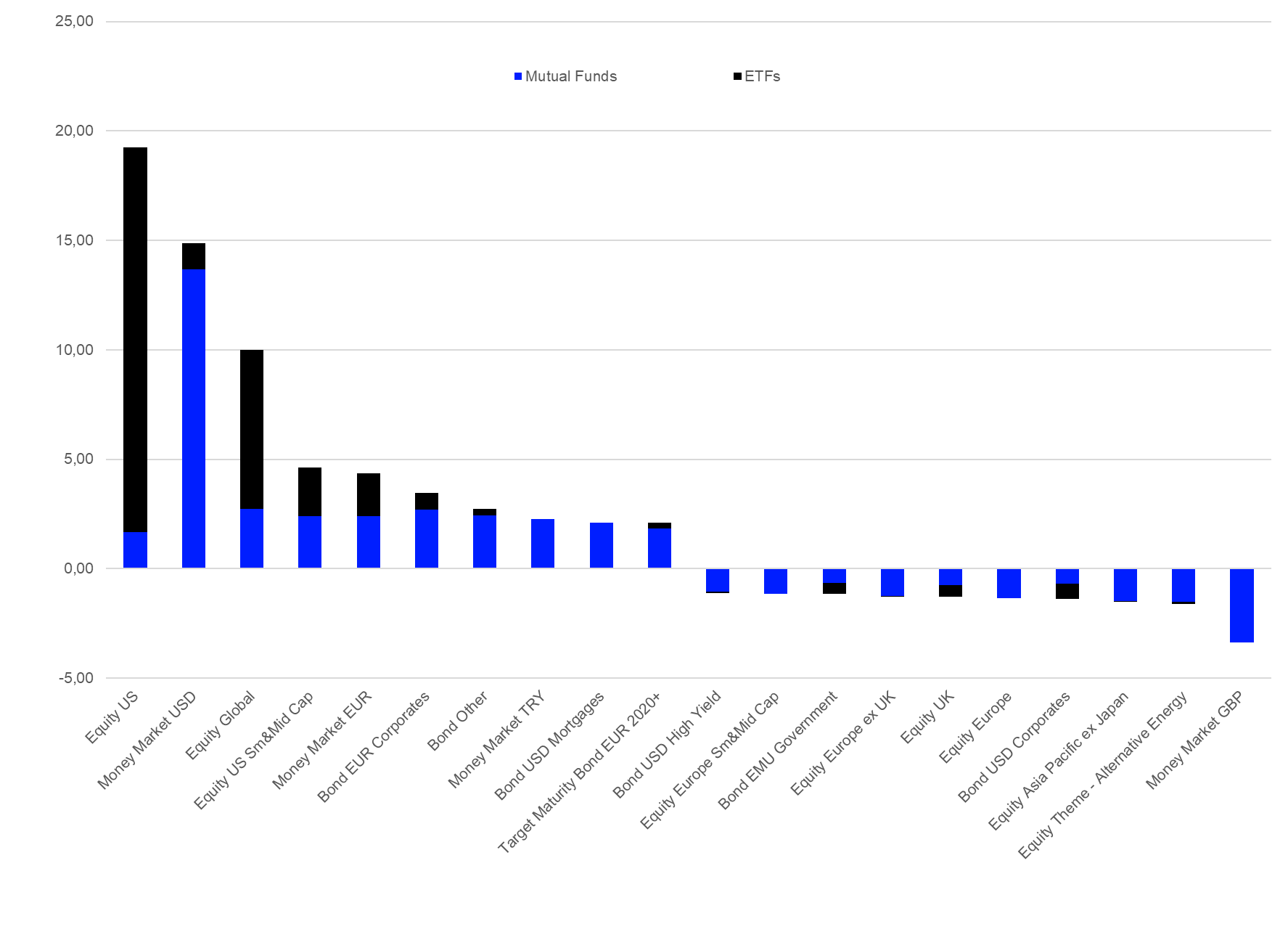

Given the general fund flows trend in Europe for December, it was not surprising that Equity U.S. (+€19.3 bn) dominated the table of the 10 best-selling peer groups by estimated net flows for December. The classification was followed by Money Market USD (+€14.9 bn), Equity Global (+€10.0 bn), Equity U.S. Small & Mid Cap (+€4.6 bn), and Money Market EUR (+€4.4 bn).

Graph 4: Ten Best- and Worst Lipper Global Classifications by Estimated Net Sales, December 2024 (Euro Billions)

Source: LSEG Lipper

On the other side of the table, Money Market GBP (-€3.4 bn) faced the highest estimated net outflows for December, bettered by Equity Theme – Alternative Energy (-€1.6 bn) and Equity Asia Pacific ex Japan (-€1.5 bn).

A closer look at the best and worst Lipper Global Classifications by estimated net sales for December shows that European investors are in a mixed mood with regard to their risk appetite over the course of the month. On one hand, European investors increased their positions in bonds and equities. On the other hand, they also bought money market products, which are considered as safe haven products.

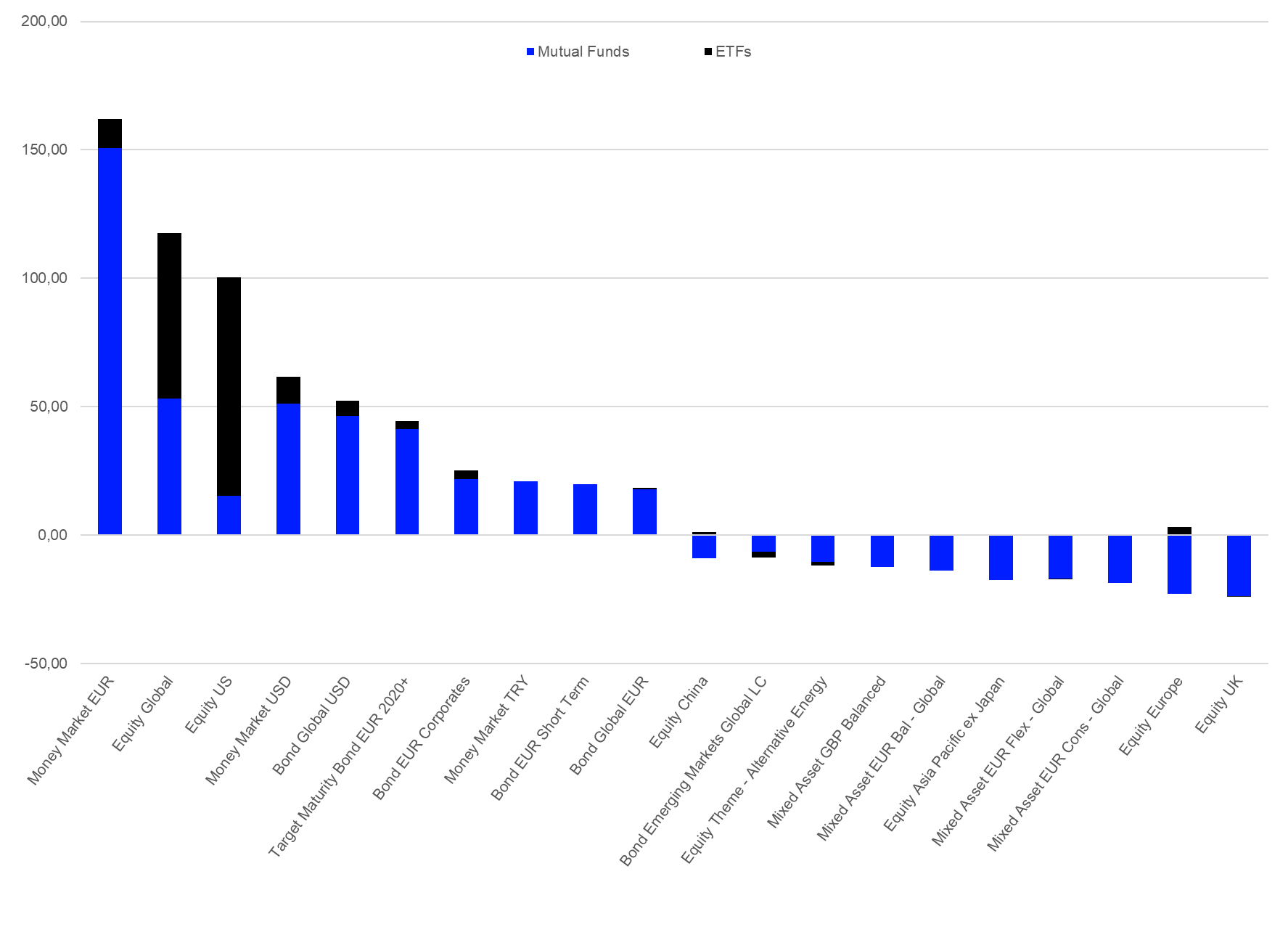

Fund Flows by Lipper Global Classifications, Year to Date

A closer look at the best and worst Lipper Global Classifications by estimated net sales for 2024 also shows that European investors are somewhat in a mixed mood with regard to their risk appetite since bond and money market classifications are dominating the table of the best-selling Lipper Global Classifications.

As graph 2 shows, mixed-assets products faced the highest outflows over the course of the year 2024, while bond and money market products enjoyed the highest estimated net inflows. Given the overall trend it was not surprising that the table of the best-selling Lipper Global Classifications is dominated by bond and money market classifications, while equity and mixed-assets classifications dominated the other side of the table.

In more detail, Money Market EUR (+€162.2 bn) was the best-selling Lipper global classification for the year so far. It was followed by Equity Global (+€117.6 bn), Equity U.S. (+€100.3 bn), Money Market USD (+€61.7 bn), and Bond Global USD (+€52.3 bn).

Graph 5: Ten Best- and Worst Lipper Global Classifications by Estimated Net Sales, January 1 – December 31, 2024 (Euro Billions)

Source: LSEG Lipper

Given the current market environment, it was not surprising to see so many mixed-assets classifications on the opposite side of the table since European investors seem to be readjusting their portfolios to the new environment in the bond markets after the central banks around the globe lowered their interest rates and may continue to do so in the foreseeable future. The same might be somewhat true for equity classifications since investors adapt their portfolios to a new regime of divided economic growth trends in the different major regions/countries around the globe. Equity U.K. (-€23.8 bn) faced the highest outflows for the year. It was bettered by Equity Europe (-€19.9 bn), Mixed Asset EUR Conservative – Global (-€18.6 bn), Mixed Asset EUR Flexible – Global (-€17.1 bn), and Equity Asia Pacific ex Japan (-€17.1 bn).

As mentioned above, it is noteworthy that the estimated flows in money market sectors are not only a reflection of asset allocation decisions of investors since these products are also used by corporates as a replacement for cash accounts. In addition, it is also important to recall that the yield curves in the Eurozone and other parts of the world are still somewhat inverted, which means that money market instruments offer a higher yield than medium- or long-term bonds.

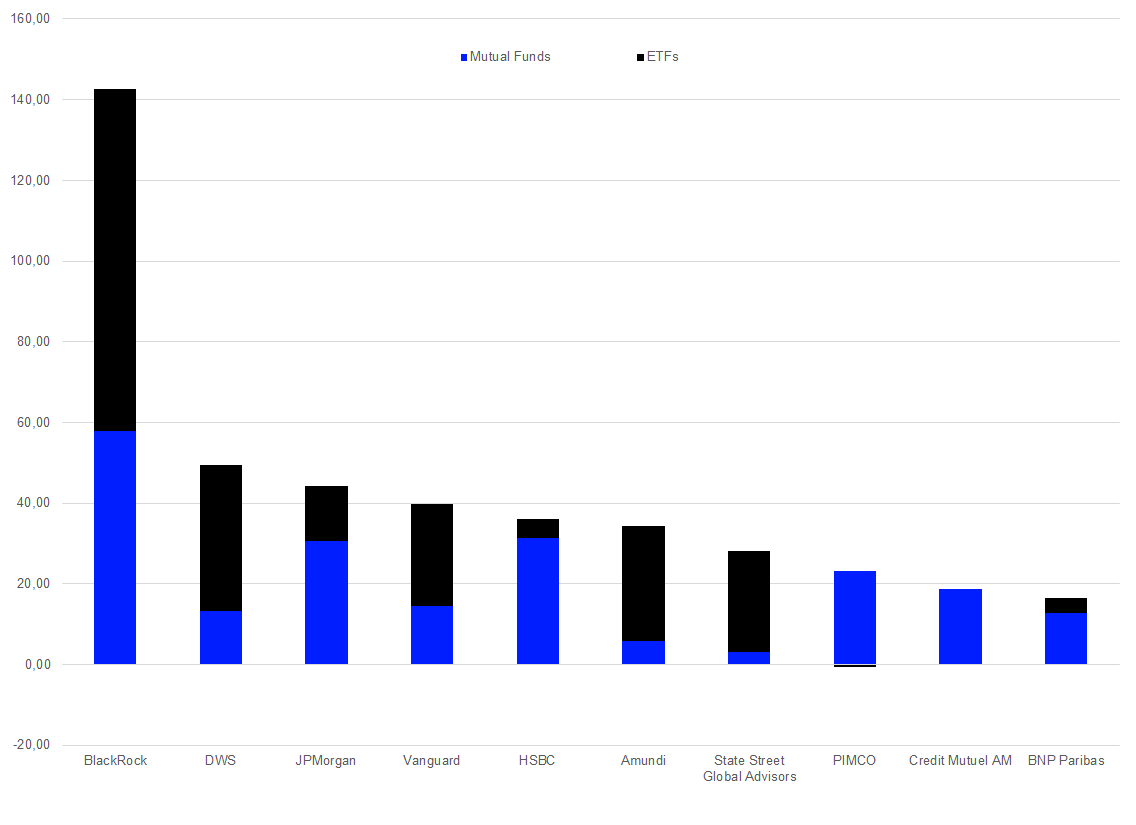

Fund Flows by Promoters, December 2024

BlackRock (+€13.7 bn) was the best-selling fund promoter in Europe for December, ahead of number two promoter JPMorgan (+€11.5 bn), Morgan Stanley (+€7.3 bn), Amundi (+€6.0 bn), and DWS Group (+€5.2 bn). Given the product ranges of the 10-top promoters and the overall fund flow trends, it was not surprising to see that ETFs played a vital role for the positions of the leading fund promoters in Europe.

Graph 6: Ten Best-Selling Fund Promoters in Europe, December 2024 (Euro Millions)

Source: LSEG Lipper

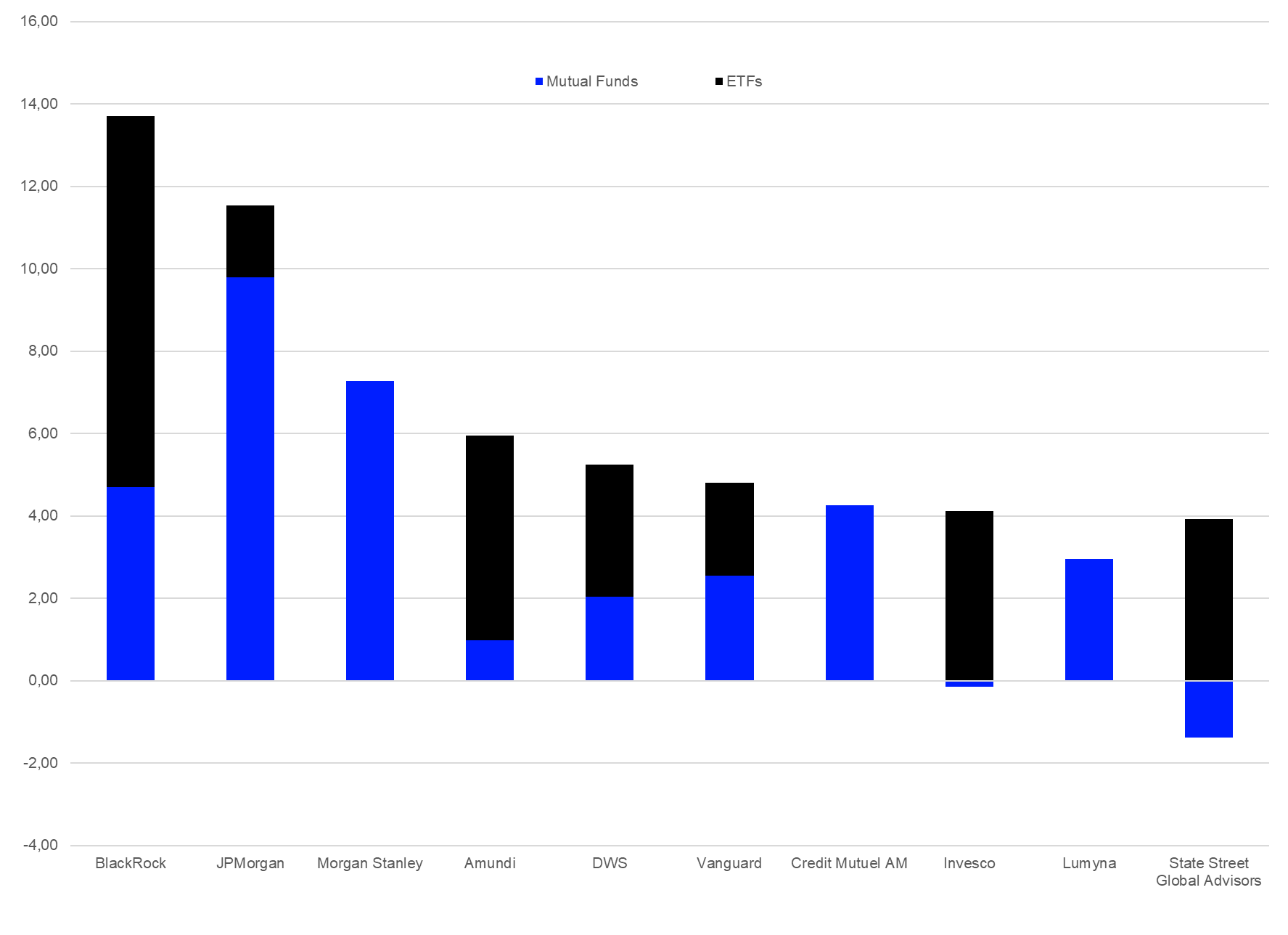

Fund Flows by Promoters, Year to Date

BlackRock (+€142.6 bn) is the best-selling fund promoter in Europe over the course for the year 2024, ahead of DWS Group (+€49.5 bn), JPMorgan (+€44.3 bn), Vanguard (+€39.7 bn), and HSBC (+€36.2 bn).

A view of the flow split by products over the year-to-date period gives an even clearer view of the importance of ETFs for the sales success of those promoters who have a respective product offering since BlackRock, Vanguard, DWS, State Street Global Advisors, Amundi, and Invesco all enjoyed higher inflows into ETFs than into their mutual funds.

Graph 7: Ten Best-Selling Fund Promoters in Europe, January 1 – December 31, 2024 (Euro Billions)

Source: LSEG Lipper

This article is for information purposes only and does not constitute any investment advice.

The views expressed are the views of the author, not necessarily those of LSEG Lipper or LSEG.