The second quarter of 2019’s earnings season kicked off with a flood of bank earnings reports. Fourteen of the 19 companies within the S&P 500’s bank industry have reported 19Q2 earnings and revenue. While the majority of companies within the industry beat top and bottom line expectations, they fell short on some industry key performance indicators (KPI’s).

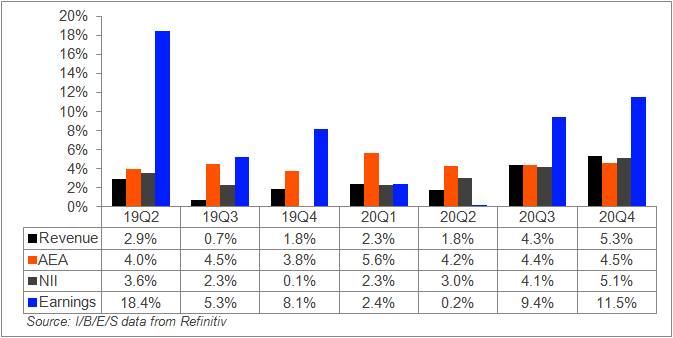

Exhibit 1: S&P 500 Bank Industry YoY Growth Rates

The S&P 500 bank industry is expected to see 19Q2 YoY revenue increase 2.9% and earnings increase 18.4%. Of the companies that reported, 78.6% beat revenue estimates, which came in 1.7% above expectations. The majority of the industry (64.3%) reported earnings higher than analysts’ consensus. In aggregate, earnings were 4.3% greater than anticipated. The majority of the industry may have beaten the headline numbers, but they missed industry KPI’s such as net interest margin (NIM) and net interest income (NII).

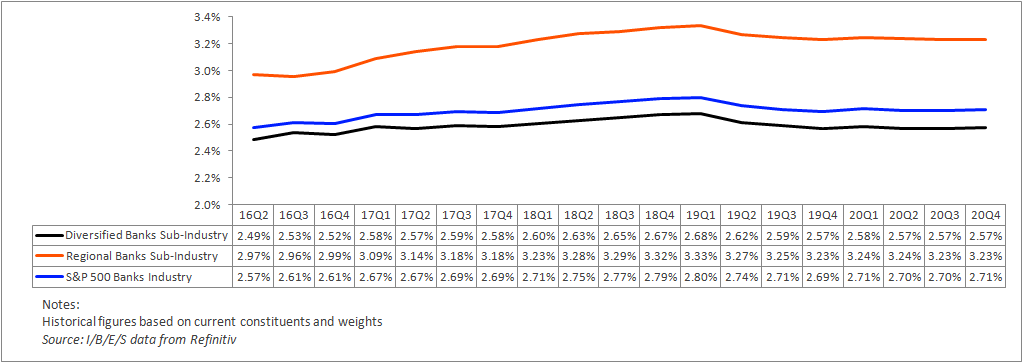

Exhibit 2: S&P 500 Bank Industry Net Interest Margins by Sub-Industry

Thirteen of the 14 banks missed 19Q2 NIM and NII estimates. In aggregate, 19Q2 NII came in 0.6% below consensus. 19Q2 NIM for the banks industry declined 1.0 basis points (bps) to 2.74% from the prior year and 6.6 bps sequentially. While 19Q2 NII increased 3.6 YoY it failed to outpace average earning asset (AEA) growth, which gained 4.0% from the prior year.

SunTrust Banks Inc (STI.N) reported a 3.2% YoY gain in 19Q2 NII to $1,535.0 million. However, NIM for the quarter of 3.16% vs. analysts’ estimates for 3.24% is expected to be the largest YoY decline (12 bps) for the S&P 500 bank industry. SunTrust noted higher funding costs and declines in short-term and long-term interest rates as margins pressures. William Henry Rogers, SunTrust Banks Inc – Chairman & CEO, spoke about the outlook and margin pressures saying, “Bigger picture, it’s clear that our clients remain optimistic about the economy and are committed to making ongoing investments, both personally and in their businesses. Offsetting the strong loan growth we delivered was pressure on the net interest margin given increased funding costs and rate dynamics.”

Bank of America Corporation (BAC.N) reported 19Q2 NIM of 2.44% vs. consensus of 2.46%. This was up 6 bps YoY and down 7 bps sequentially. NII for the quarter grew 5.9% from the prior year, but came in 0.8% below estimates at $12,338 million. Speaking about the outlook Paul M. Donofrio, Bank of America Corporation – CFO, said, “In the second half of the year, we expect NII to benefit from growth in loans and deposits as well as an additional day of interest in Q3. However, lower rates are expected to have three primary negative effects. First, yields on floating rate assets should continue to decline from short-term rate reductions. Second, lower long-term rates may continue to stimulate mortgage refinancings, causing increased write-off of bond premiums. And third, reinvestment rates on securities and mortgages will dilute current portfolio yields.”

Looking ahead analysts currently anticipate NIM will contract as AEA growth is expected to outpace NII.

Republication or redistribution of Reuters content, including by framing or similar means, is prohibited without the prior written consent of Reuters. Reuters and the Reuters logo are registered trademarks, and trademarks of the Thomson Reuters group of companies. For additional information on Reuters photographic services, please visit the web site at http://pictures.reuters.com