The assets under management in the European ETF industry are highly concentrated at the classification level. Even as one would expect that the AUM are concentrated at the classification level since this reflects the asset allocation views of the investors—which are in general rather streamlined than widely diverging—the level of concentration might be surprising.

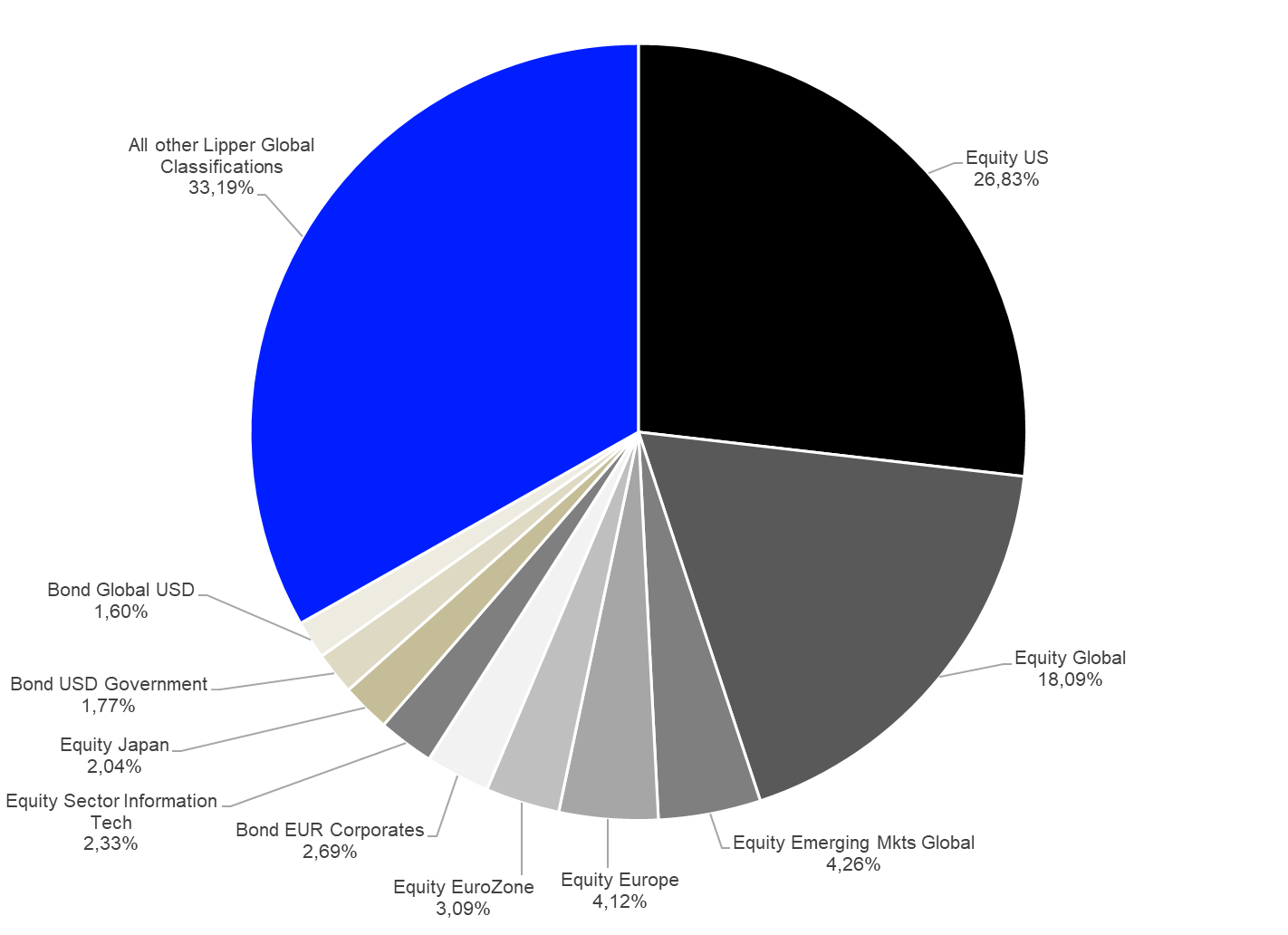

ETFs classified as Equity U.S. held 26.83% of the overall assets under management at the end of December 2024. The second largest classification, Equity Global, held 18.09% of the overall AUM and Equity Emerging Markets Global held 4.26%. Given the fact that Equity U.S. and Equity Global are somewhat core asset classes in the portfolios of European investors, one could argue that this level of concentration is somewhat normal since these two classifications may represent two of the largest building blocks in the portfolios of European investors.

If the assumption that European investors are using ETFs as building blocks for their core exposures were true, other core asset classes such as Equity Europe should also hold high assets under management. In fact, Equity Europe (4.12% market share) is the fourth largest classification in the European ETF industry and Equity Eurozone comes in as number five (3.09%). This means that European equities do not play a major role for European ETF investors, even if one combines the AUM of the two classifications. That said, one needs to bear in mind that a high number of investors follow one of the major global equity indices regarding the asset allocation of their portfolios. This implies that Equity U.S. should be by far the largest classification as it is the largest region in all market capitalization weighted indices, followed by Europe.

Graph 1: Market Share of the 10-Largest Lipper Global Classifications by Assets Under Management (December 31, 2024)

Source: LSEG Lipper

This means that the high concentration of assets under management in the European ETF industry can be considered normal. That said, one should be surprised that ETFs classified as Equity Emerging Markets Global play such an important role in the European ETF industry since emerging markets are normally considered as inefficient markets where active fund managers should be able to outperform the market (indices). The same is true for sixth (Bond EUR Corporates -2.69%) and seventh (Equity Sector Information Technology -2.33%) largest classifications. Even as it is to be expected that market share of these three classifications might be driven by market trends and might therefore be a subject to change in the future, one can assume that some European investors prefer to implement their exposure to non-core asset classes via passive instruments. In other words, one may conclude that these European investors prefer the pure beta of these asset classes over a possible outperformance.

This article is for information purposes only and does not constitute any investment advice.

The views expressed are the views of the author, not necessarily those of LSEG.