The global ETF industry enjoyed general inflows over the course of January 2025.

These inflows occurred in a mainly positive but volatile market environment. The markets were driven by the effects around the inauguration of Donald Trump as the next U.S. president. On one hand, investors appreciated the expected positive impacts on the U.S. economy from the new administration. Meanwhile, they feared the impacts from possible tariffs, which may cause a global trade war as an unwanted side-effect and higher government spending on inflation and, therefore, on the resulting policies of the U.S. Federal Reserve. That said, the high valuations of the market leaders and the more hawkish statements from the U.S. Federal Reserve led to an environment in which investors are somewhat nervous and reacting quickly to any news that may impact the current market environment negatively.

That said, investors are not only focusing on economic news, as the geopolitical tensions in the Middle East—especially the developments around the Red Sea—are seen as a risk for the general economic growth in Western countries. While a possible peace agreement between Israel and the Hamas may lead to a lower price for oil, the activities of the Houthi rebels are still a concern since a number of shipping companies these days avoid the passage of the Suez channel. It is, therefore, to be expected that prolonged delivery times can cause some tensions for the still vulnerable delivery chains.

As mentioned above, market sentiment was also further driven by the expectations of investors for future central bank decisions. Since the different regions of the world are showing different growth patterns, it is to be expected that central banks will follow different paths with regard to their interest rate policies. Even as investors were already expecting less activity from the U.S. Federal Reserve, the somewhat hawkish statements of some Fed members led to concerns about the future policy of the Fed.

On the other hand, the European Central Bank (ECB) made rather dovish statements. Therefore, investors expect the interest rate in the Eurozone to decline significantly over the course of 2025. As a result, such different central bank activity may lead to a stronger U.S. dollar compared to the euro and other leading currencies. With regard to this, any statement from the Fed and other central banks may have the power to move the bond market in one or the other direction. In addition, fears of increasing debt in the U.S. might be the driver for further increasing interest rates on the long end of the yield curve, which may have held back inflows into medium and long-term bond ETFs, while the still inverted yield curves might be the drivers for the inflows into money market ETFs.

That said, inverted yield curves and especially long-term inverted yield curves are seen as an early indicator for a possible recession. However, there are no signs for a recession in the U.S. and most other major economies visible yet. But even as it looks like the yield curves are slowly normalizing, this does not mean that there is no recession possible in the major economies around the globe. This is especially true as some major economies lack economic growth and may need lower interest rates as stimulus. Despite these headwinds, the positive effects of lower interest rates seem to be more important for investors than the current state of some economies.

From an ETF industry perspective, the performance of the underlying markets led, in combination with the estimated net flows, to increasing assets under management (from €14,206.5 bn as of December 31, 2024, to €14,740.9 bn at the end of January). At a closer look, the decrease in assets under management of €534.4 bn for January was driven by the performance of the underlying markets (+€377.3 bn), while the estimated net inflows contributed (+€157.1 bn), to the development of the assets under management.

That said, a more detailed view of the estimated net flows by region shows that the fund flow trends were consistent for all regions. Nevertheless, some ETF domiciles faced outflows over the course of January 2025.

Table 1: General Overview on Global Assets Under Management and Estimated Fund Flows by Regions and Major ETF Domiciles (January 31, 2025)

Source: LSEG Lipper

Assets Under Management

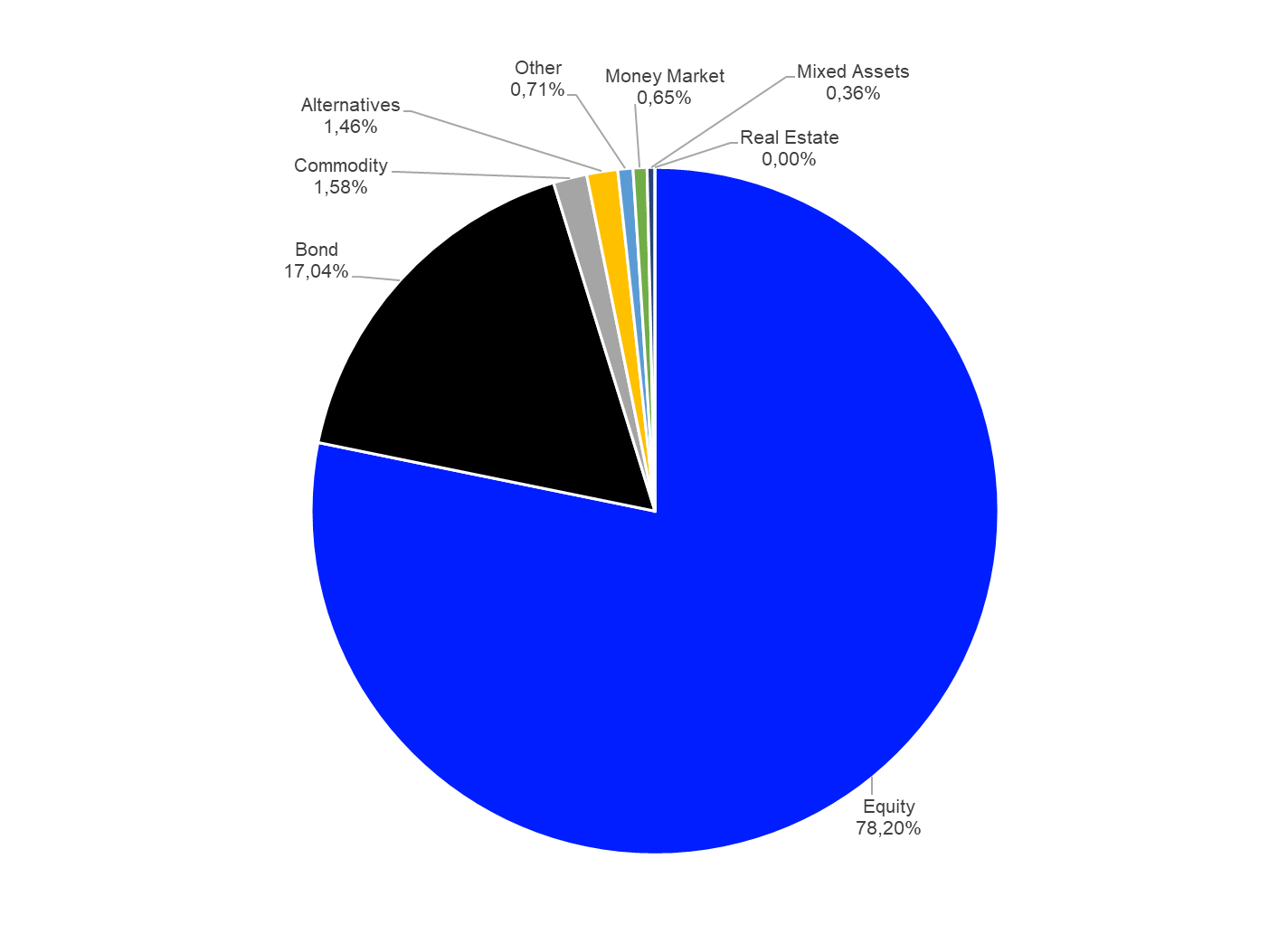

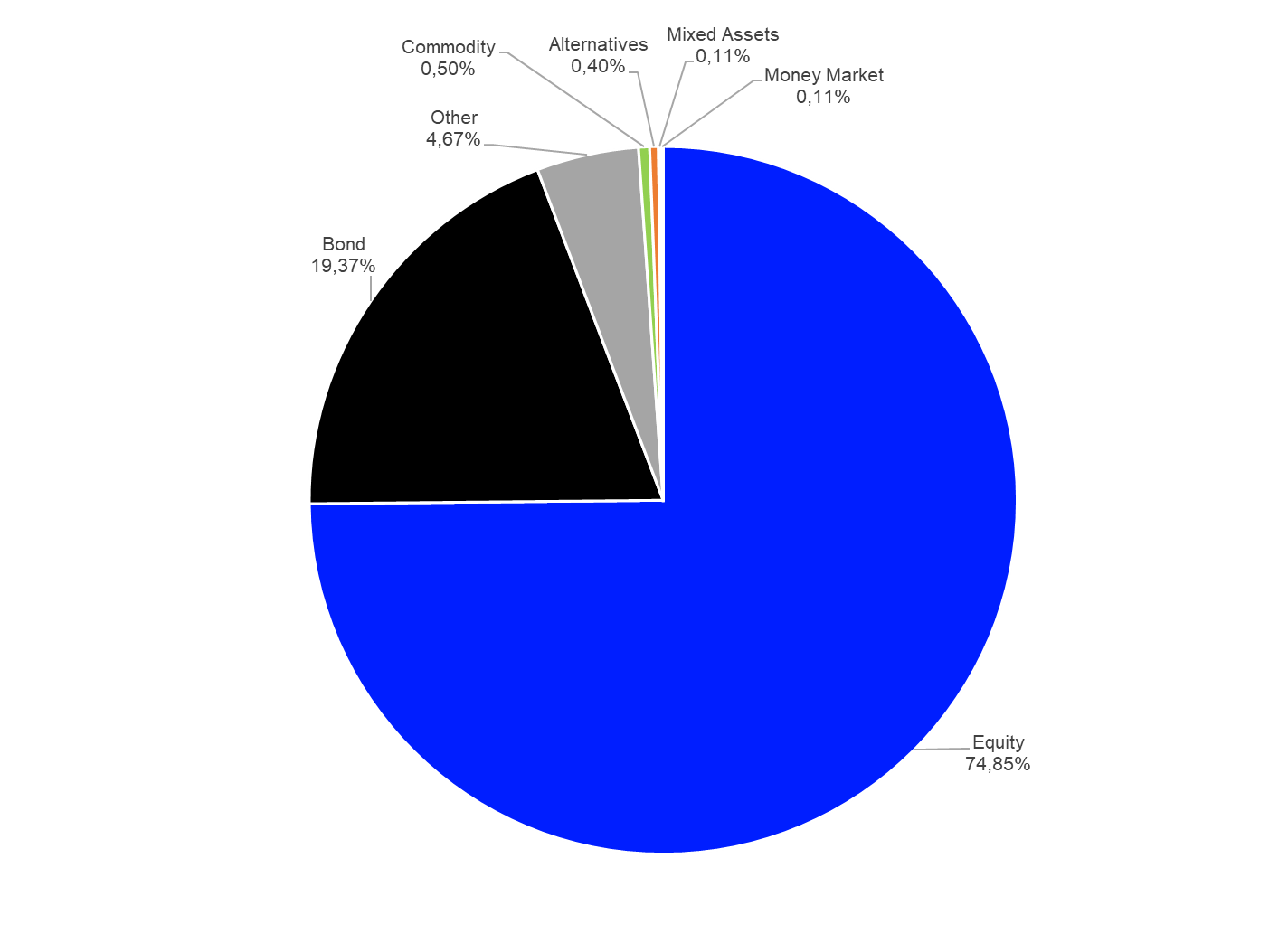

Assets under management in the global ETF industry decreased from $14,206.5 bn as of December 31, 2024, to $14,740.9 bn at the end of January 2025. The majority of these assets ($11,527.0 bn) were held in equity ETFs. This category was followed by bond ETFs ($2,511.2 bn), commodities ETFs ($232.8 bn), alternatives ETFs ($214.9 bn), “other” ETFs ($105.0 bn), money market ETFs (€96.3 bn), mixed-assets ETFs ($53.6 bn), and real estate ETFs (€0.03 bn).

Graph 1: Market Share Assets Under Management in the Global ETF Industry by Asset Type – January 31, 2025

Source: LSEG Lipper

Since this report covers a limited number of ETNs and ETCs, the so-called “structured notes” alongside ETFs, it is important to show the market share of assets under management of these products in comparison to ETFs to indicate the relevance and possible impact of these products for this study.

While ETFs held $14,345.5 bn, or 97.32%, of the overall assets under management, the structured notes covered in this report held $395.4 bn, or 2.68%, of the overall assets under management covered in this report at the end of January 2025.

Graph 2: Market Share Assets Under Management in the Global ETF Industry by Product Type – January 31, 2025

Source: LSEG Lipper

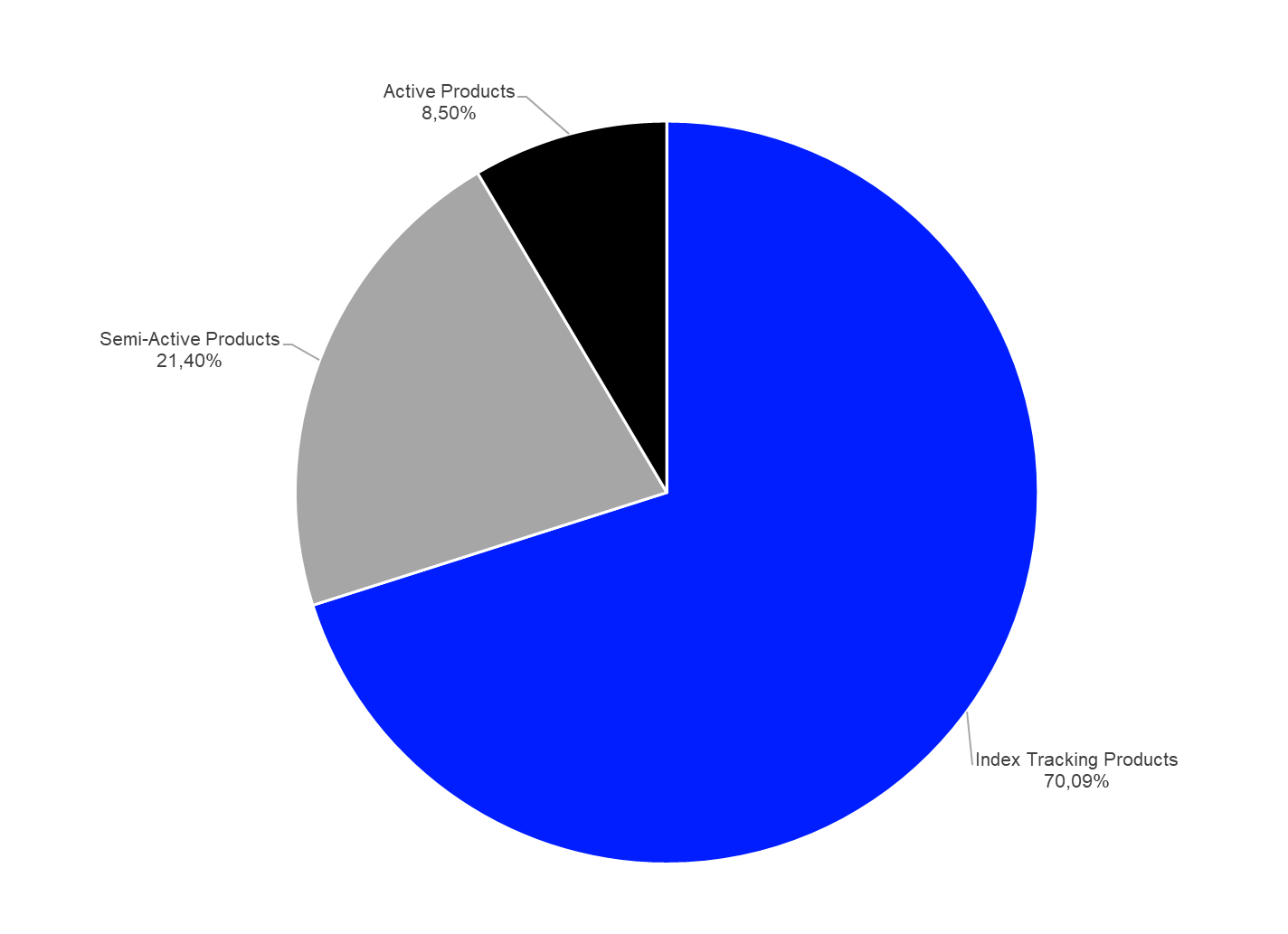

Since ETFs are product wrappers which are used for passive index tracking products and active/semi-active strategies, it is important to shed a light on these two different product categories. Market observers expect more growth in the segment of active/semi-active products in the future since an increasing number of active managers are starting to launch ETFs not linked to an index or ETF share classes of existing actively managed mutual funds. It is expected that this trend will continue since the patent on ETF share classes held by Vanguard expired in April 2023.

Nevertheless, it is no surprise that index tracking products held the vast majority of the overall assets under management in the global ETF industry ($10,332.2 bn or 70.09%), while ETFs which aim to outperform an index or are not linked to an index at all held $4,408.7bn, or 29.91%, of the overall assets under management at the end of January 2025.

Graph 3: Market Share Assets Under Management in the Global ETF Industry by Management Approach – January 31, 2025

Source: LSEG Lipper

Assets Under Management Factor-Based ETFs

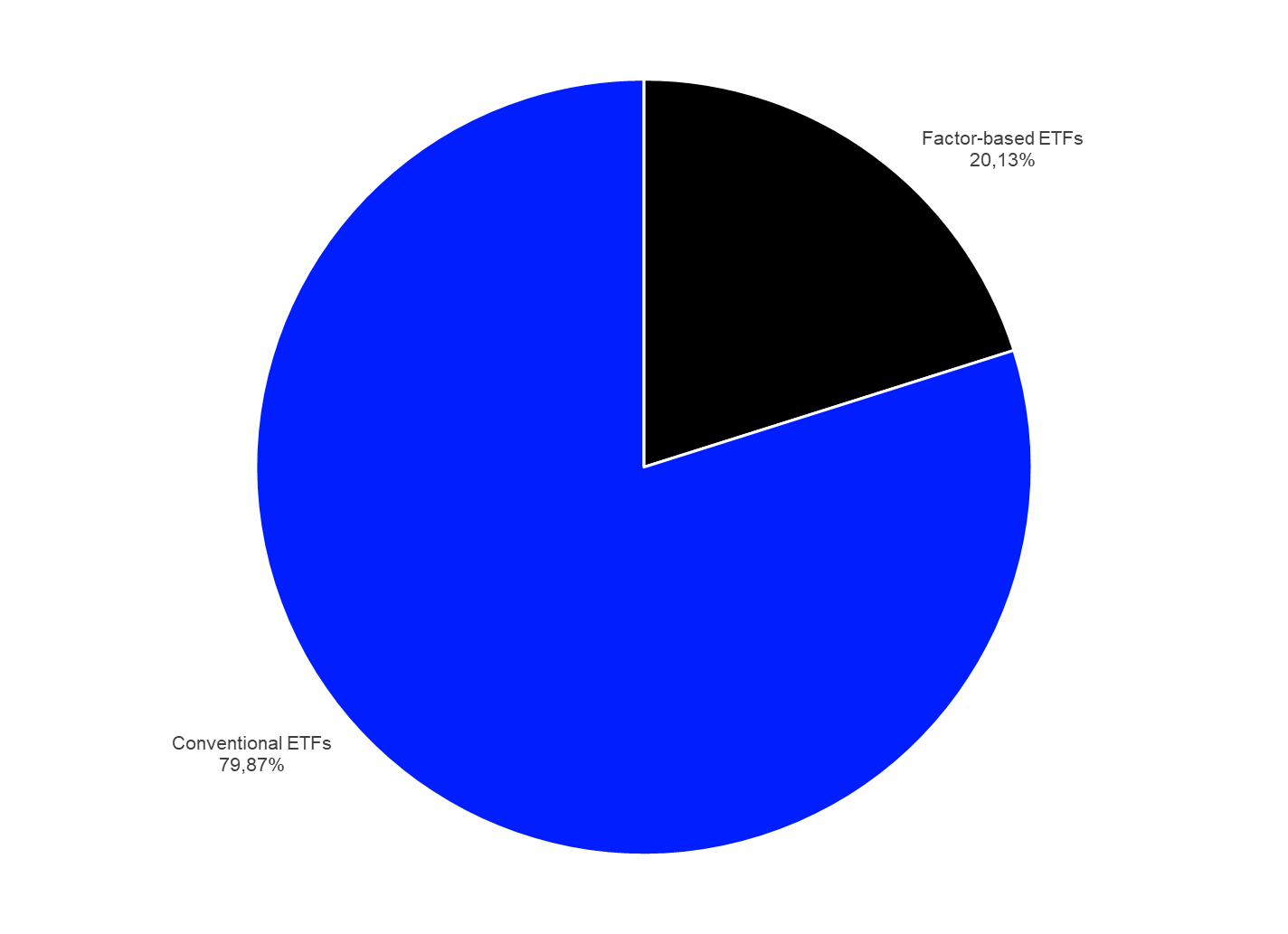

Since products which follow a factor-based strategy—the so-called smart beta products—can be found under both product types, it makes sense to highlight the high overall market share of factor-based products. Overall, factor-based products held assets under management of $2,967.5 bn at the end of January, which means in turn these products had an overall market share of 20.13%. The high percentage of the assets under management in factor-based ETFs shows that these products, which have been seen as marketing-driven product launches in the past, have become mainstream investments over time.

Graph 4: Market Share Assets Under Management in the Global ETF Industry Factor-Based ETFs vs Conventional ETFs – January 31, 2025

Source: LSEG Lipper

It is actually no surprise that investors around the globe use factor-based ETFs within their portfolios since these products offer access to a broad range of factors which have proven that they can be exploited to deliver additional returns for investors over longer time periods. Nevertheless, the potential outperformance of a given factor is often dependent on the right timing of the investment since single factors do not deliver a consistent outperformance. When it comes to this, it is no surprise that the global ETF industry developed products which use multiple factors. These products should be easier to use for investors since the usage of multiple factors removes the need for market timing.

The graph below shows the variety of factor strategies which are available to investors.

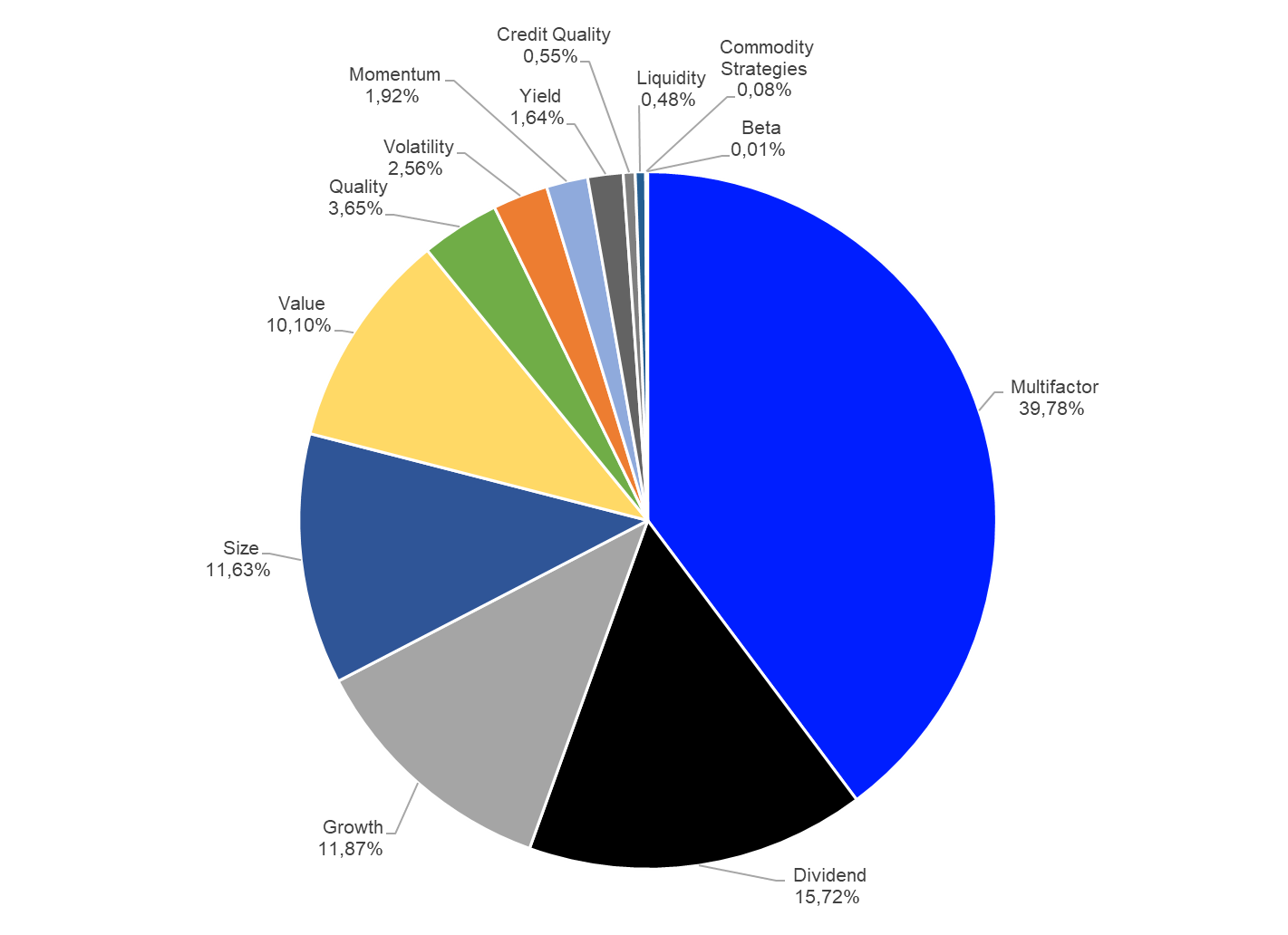

As multifactor ETFs are convenient products, it is no surprise that these products held the highest assets under management in the segment of factor-based ETFs ($1,180.5 bn). They are followed by ETFs using dividends as a selection factor ($466.6 bn), ETFs using the growth factor ($352.3 bn), size factor ETFs ($345.2 bn), and ETFs using the value factor ($299.7 bn).

Graph 5: Market Share Assets Under Management of Single Factors within the Factor-based ETF Universe – January 31, 2025

Source: LSEG Lipper

Assets Under Management ESG-Related ETFs

Since sustainable investing is one of the major topics for investors around the globe, it is no surprise that the global ETF industry offers sustainable products. The products available use different strategies and sustainable investment credentials. It is noteworthy, therefore, that not all ETFs which have implemented some kind of sustainable investment credentials can be seen as sustainable or ESG products. Nevertheless, this statistic marks all ETFs which state the use of at least one ESG-related credential to determine the constituents of its index as ESG-related, while ETFs which do not use any sustainable investment credentials are marked as conventional ETFs.

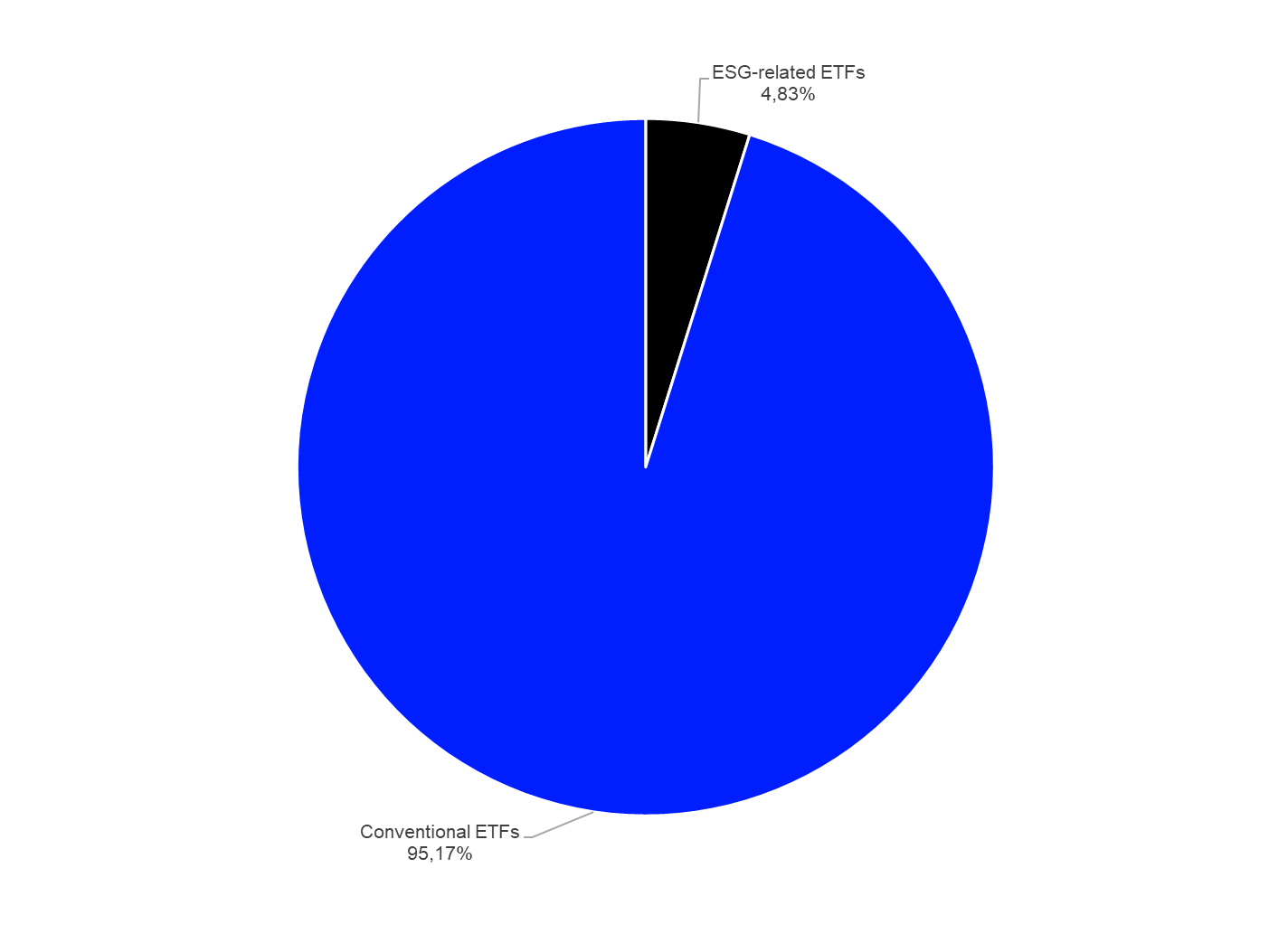

Given the fact that most portfolios are still benchmarked against conventional indices, it is not surprising that conventional ETFs ($14,029.5 bn) held the vast majority of the assets under management in the global ETF industry while their ESG-related peers held $711.4 bn in assets under management at the end of January 2025.

Graph 6: Market Share Assets Under Management in the Global ETF Industry ESG-Related ETFs vs Conventional ETFs – January 31, 2025

Source: LSEG Lipper

Since there are currently a lot of regulatory initiatives underway to tackle “greenwashing,” especially with regard to the alignment of fund names with the actual fund strategy and the usage of ESG credentials within the securities selection process, we might see a lot of change when it comes to the usage of ESG credentials in fund names or the fund-related literature. As a consequence, these changes might lead to significantly lower assets under management in ESG-related funds over the course of the next few months since fund and ETF promoters want to avoid being accused of practising greenwashing.

Given the overall market structure of the global ETF industry, it is no surprise that equity ETFs ($532.5 bn) held the highest assets under management in the segment of ESG-related ETFs. They were followed by bond ETFs ($137.8 bn), “other” ETFs ($33.2 bn), commodities ETFs ($3.6 bn), alternatives ETFs ($2.8 bn), mixed-assets ETFs ($0.8 bn), and money market ETFs ($0.8 bn).

Graph 7: Market Share Assets Under Management of ESG-Related ETFs by Asset Type – January 31, 2025

Source: LSEG Lipper

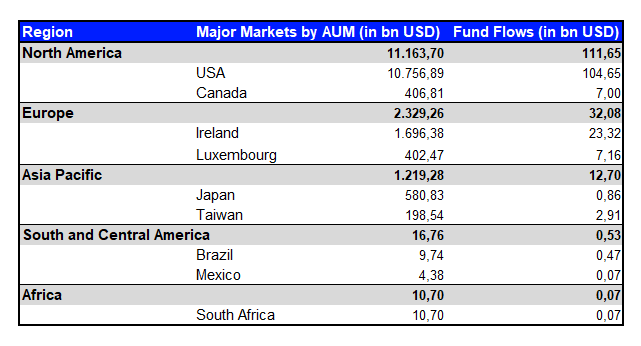

Assets Under Management by Region

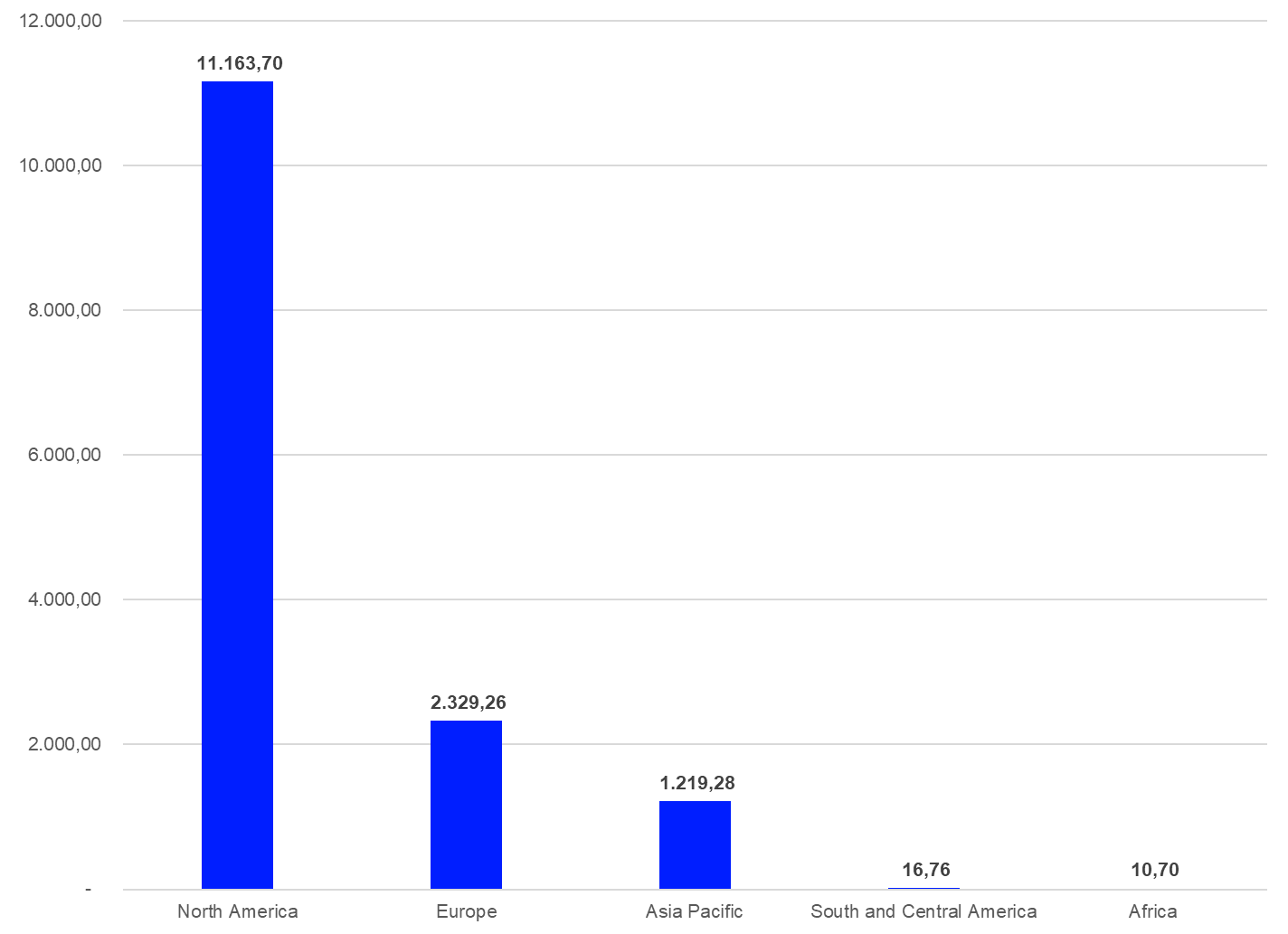

ETFs domiciled in North America ($11,163.7 bn) held the highest assets under management in the global ETF industry at the end of January 2025. They were followed by ETFs domiciled in Europe ($2,329.3 bn), ETFs domiciled in the Asia Pacific region ($1,219.3 bn), ETFs domiciled in South and Central America ($16.8 bn), and ETFs domiciled in Africa ($10.7 bn).

Graph 8: Assets Under Management in the Global ETF Industry by Region – January 31, 2025 (in bn USD)

Source: LSEG Lipper

In more detail, the U.S. was the largest single country ETF domicile ($10,756.9 bn) at the end of January 2025, followed by Ireland ($1,696.4 bn), Japan ($580.8 bn), Canada ($406.8 bn), and Luxembourg ($402.5 bn). These five ETF domiciles account for assets under management of $13,843.4 bn, or 93.91%, of the overall assets under management in the global ETF industry.

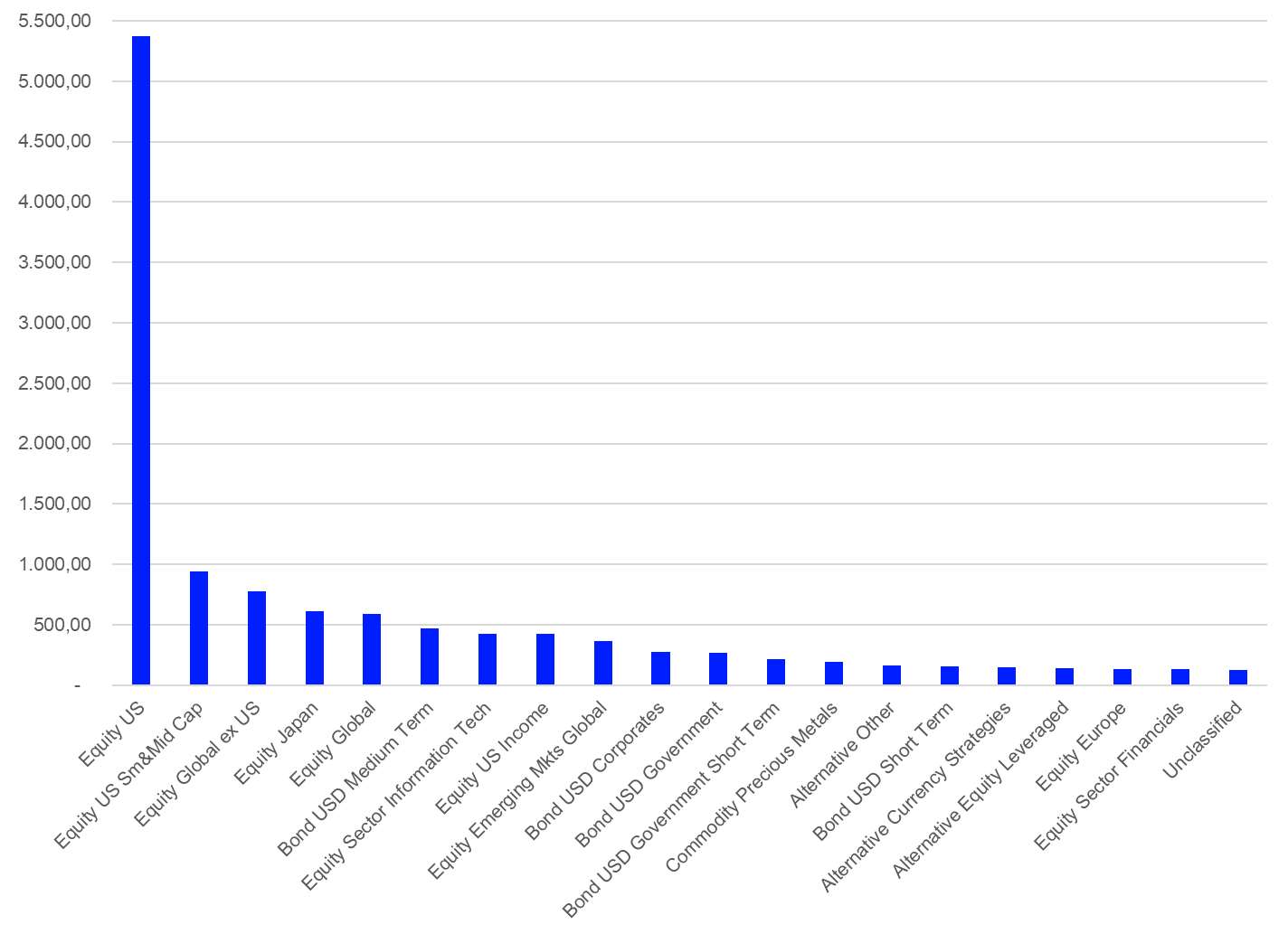

Assets Under Management by Lipper Global Classification

Equity U.S. held by far the highest assets under management ($5,369.9 bn) of the 286 Lipper Global Classifications covered in this report. It was followed by Equity U.S. Small & Mid Cap ($943.5 bn), Equity Global ex-U.S. ($775.6 bn), Equity Japan ($610.2 bn), and Equity Global ($590.7 bn).

Graph 9: The 20 Largest Lipper Global Classifications by Assets Under Management – January 31, 2025 (in bn USD)

Source: LSEG Lipper

A closer review of the assets under management by Lipper Global Classification shows that the 10 largest classifications held $10,256.8 bn, or 69.59%, of the overall assets under management of the global ETF industry, while the largest 20 classifications account for $11,938.9 bn, or 81.00%, of the overall assets under management in the global ETF industry at the end of January 2025.

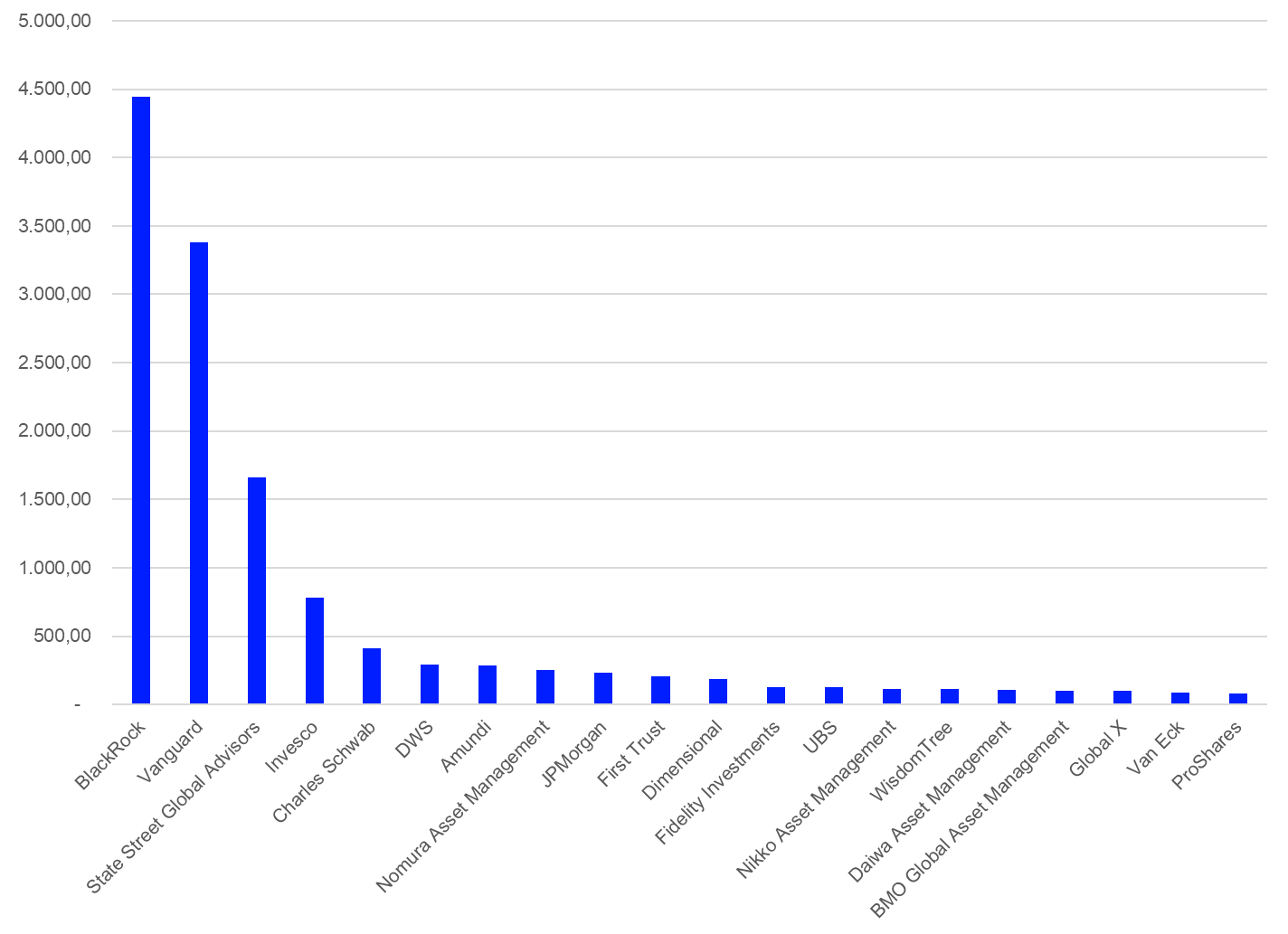

Assets Under Management by Promoters

BlackRock (iShares) is the largest promoter of ETFs globally ($4,440.9 bn). It is followed by Vanguard ($3,380.6 bn), State Street Global Advisors (SPDR) ($1,657.4 bn), Invesco ($783.9 bn), and Charles Schwab Investment Management ($408.2 bn).

Graph 10: Assets Under Management of the 20 Largest ETF Promoters Globally – January 31, 2025 (in bn USD)

Source: LSEG Lipper

As graph 10 shows, the assets under management in the global ETF industry are even more highly concentrated at the promoter level than at the domicile or classification level.

The three top ETF promoters globally account for assets under management of $9,478.8 bn, or 64.31%, of the overall assets under management. Meanwhile, the 10 top promoters account for $11,935.9 bn, or 80.98%, of the overall assets under management, and the 20 top promoters account for $13,073.9 bn, or 88.70%, of the assets under management held by ETFs globally.

Global ETF Flows

The global ETF industry enjoyed healthy overall inflows of $157.1 bn over the course of January 2025.

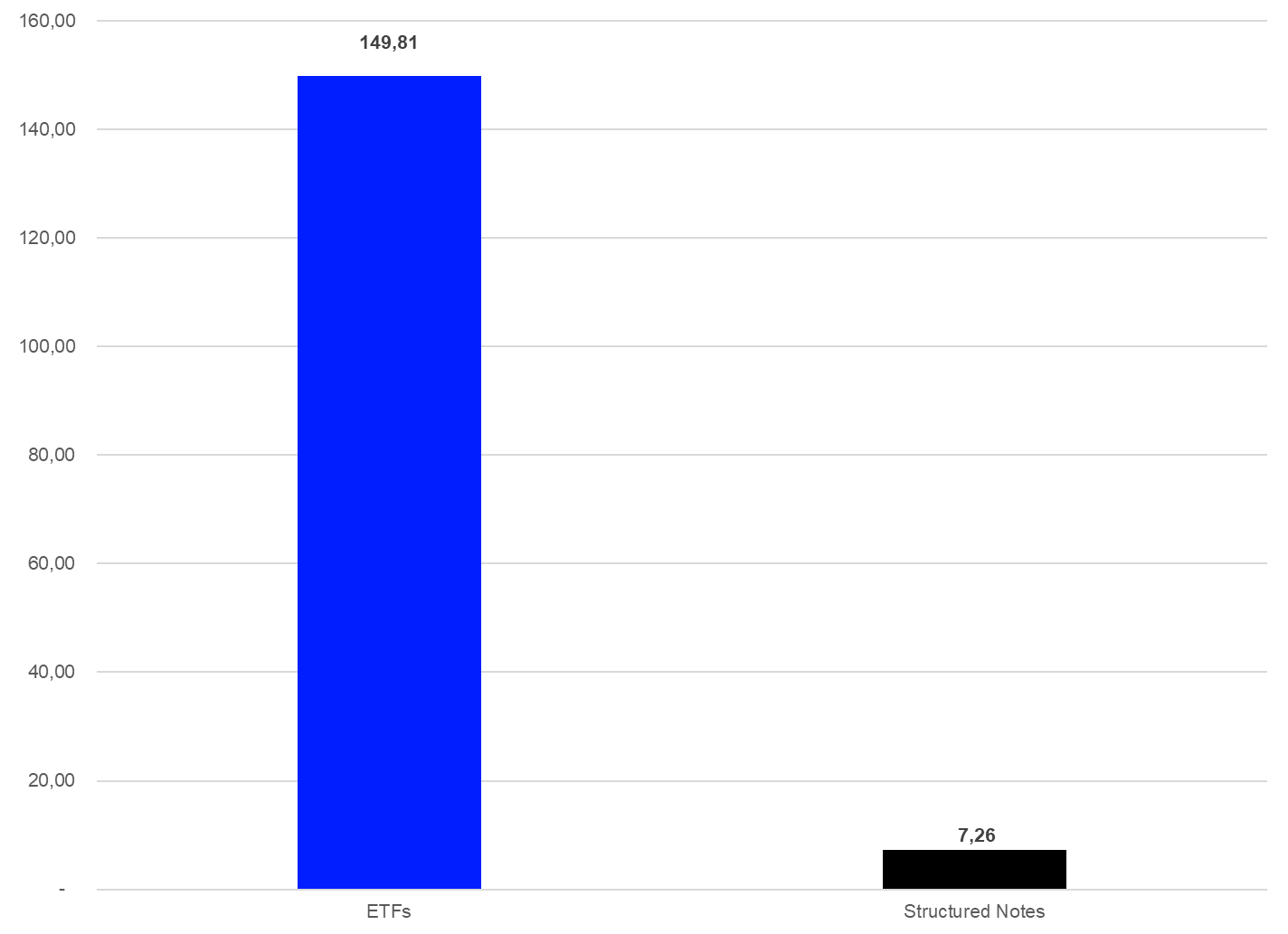

As mentioned before, this report covers a limited number of structured notes alongside ETFs. It is important to split the overall estimated fund flows between these two product types to indicate the relevance and possible impact of structured notes for this study.

ETFs enjoyed estimated net inflows of $149.8 bn over the course of January, while structured notes had estimated net inflows of $7.3 bn over the same time period.

Graph 11: Estimated Net Sales by Product Type, January 1, 2025 – January 31, 2025 (in bn USD)

Source: LSEG Lipper

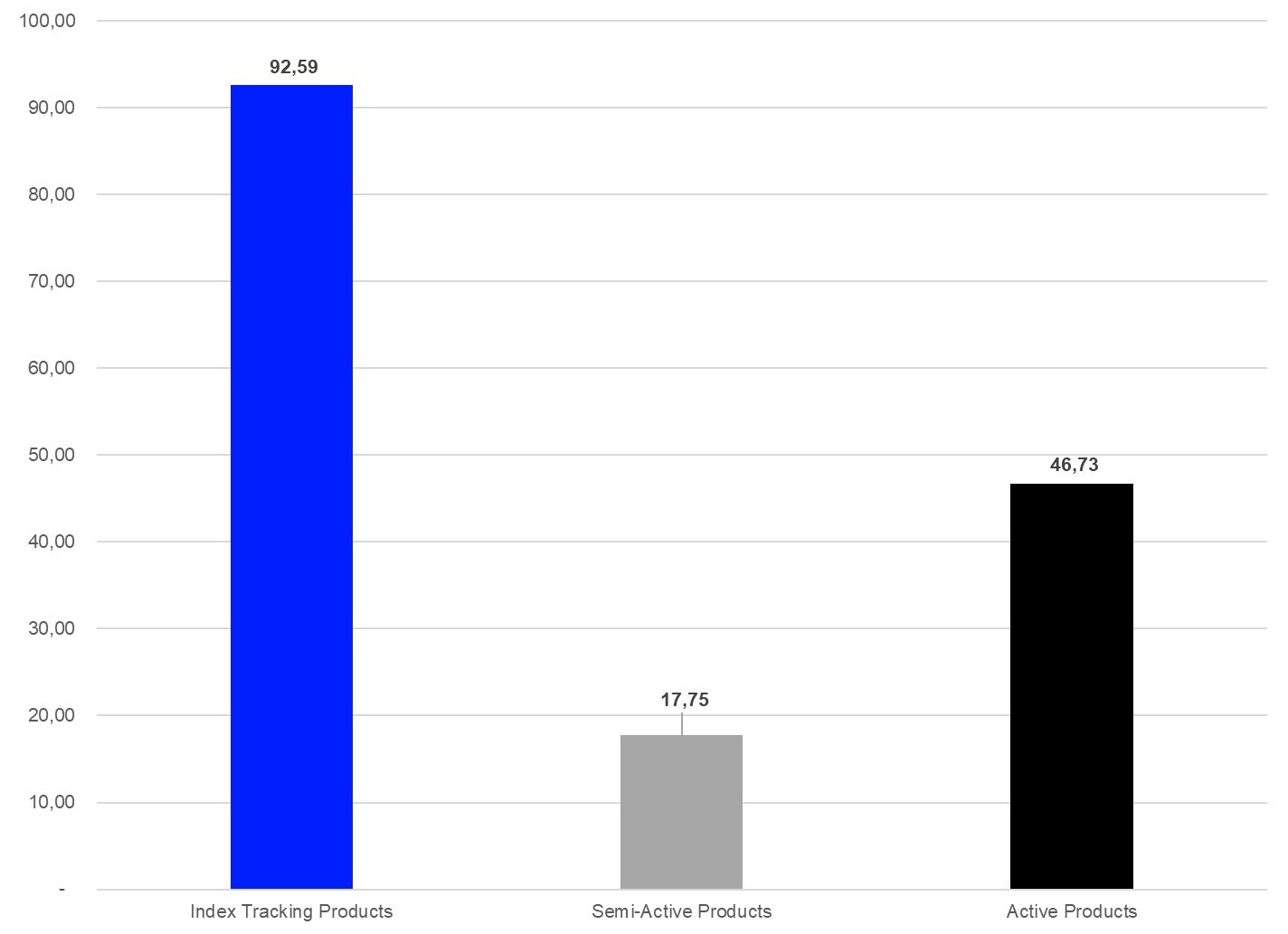

As mentioned before, ETFs can be managed with different approaches. They may use a passive approach (index tracking) where the portfolio of the respective ETF is tied to an index, or an active/semi-active approach where the fund manager has the aim to outperform an index or is not linked to an index at all.

Index tracking products enjoyed the vast majority of the estimated net inflows (+$92.6 bn) over the course of the month, while active/semi-active products enjoyed estimated net inflows of $64.5 bn over the same time period.

Graph 12: Estimated Net Sales by Management Approach, January 1, 2025 – January 31, 2025 (in bn USD)

Source: LSEG Lipper

These flow numbers show that there is a trend toward active/semi-active ETFs since the market share of the overall estimated net flows of these products (41.05%) is much higher than their market share of the assets under management (29.90%). This means active/semi-active products grow faster than the overall ETF industry and will therefore grow their market share relative to other ETF categories.

Global ETF Flows in Factor-Based ETFs

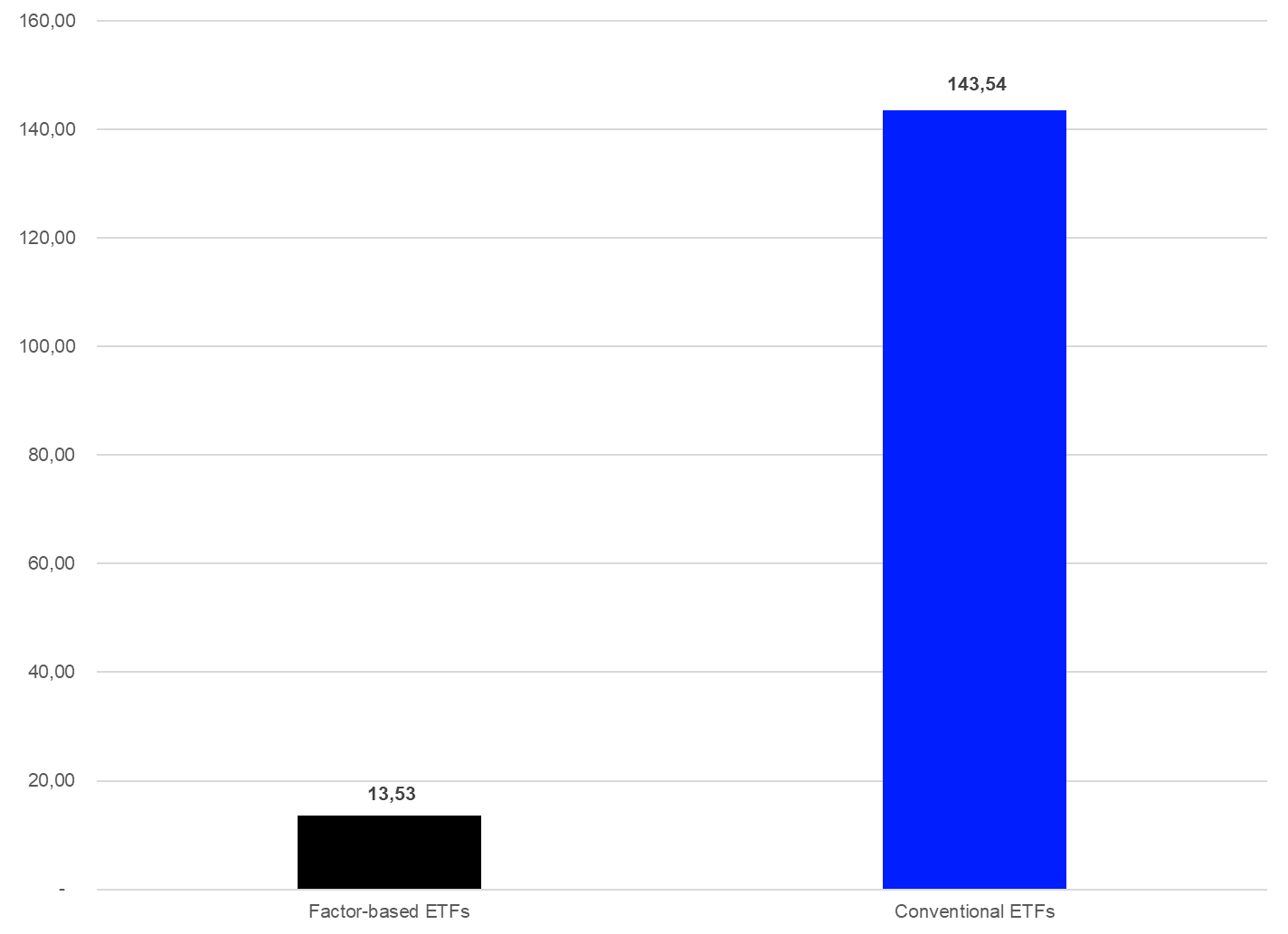

Since products which follow a factor-based strategy held a high overall market share of the assets under management in the global ETF industry, it makes sense to review the estimated net flows for these products. Especially as some market observers have already stated that active/semi-active ETFs may displace factor-based ETFs in the near future. That said, this statement can’t be proven by fund flow numbers since factor-based products enjoyed inflows of $13.5 bn over the course of January, while their conventional peers posted inflows of $143.5 bn.

Nevertheless, compared to the overall estimated net inflows into ETFs globally the market share of factor-based ETFs from the estimated overall ETF flows (8.61%) is lower than their market share of assets under management (20.13%).

Graph 13: Estimated Net Flows in the Global ETF Industry Factor-Based ETFs vs Conventional ETFs – January 1, 2025 – January 31, 2025 (in bn USD)

Source: LSEG Lipper

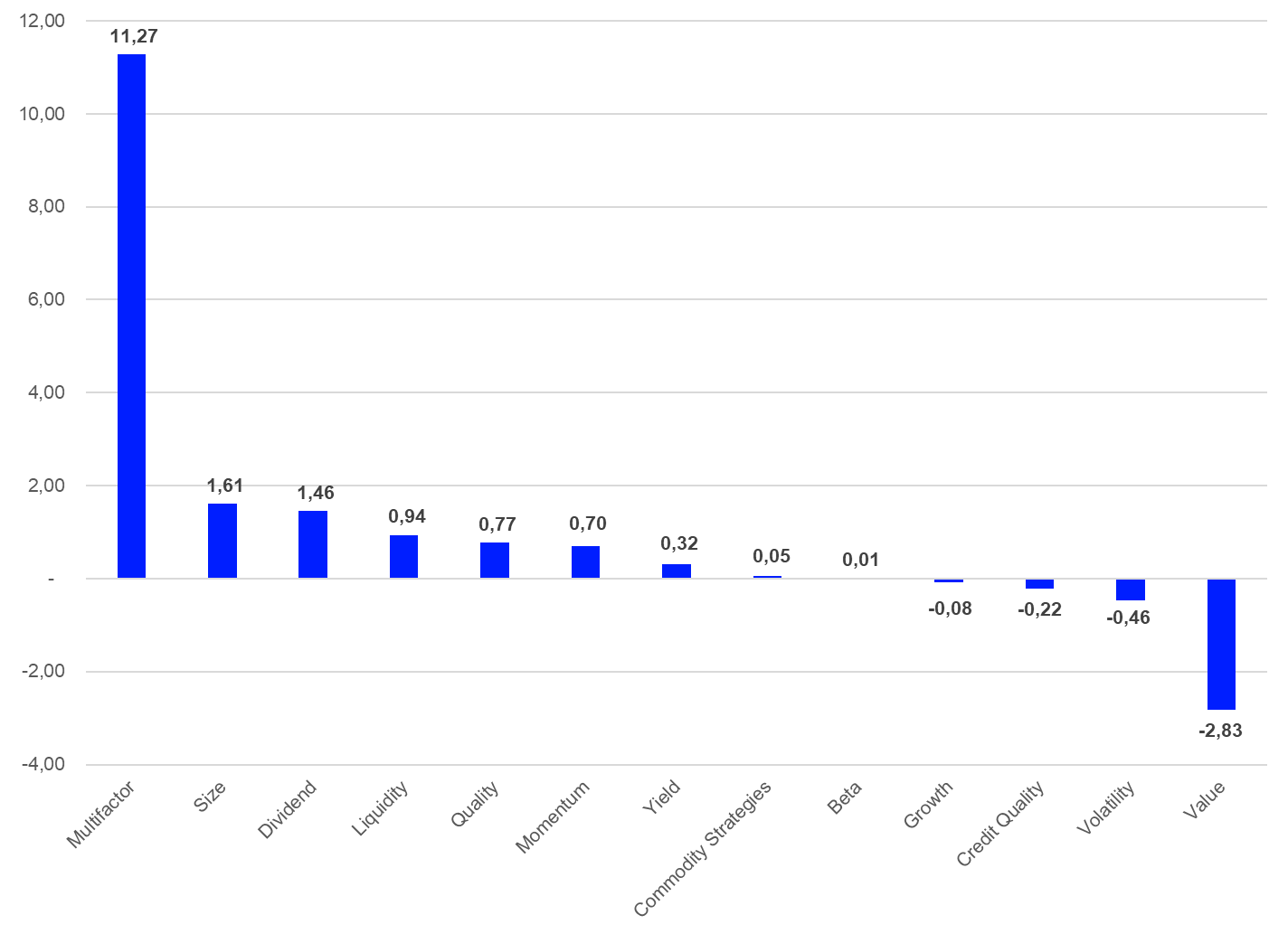

Multifactor was the best-selling strategy within the segment of factor-based ETFs (+$11.3 bn). They are followed by ETFs using the size factor (+$1.6 bn), ETFs using the dividend factor (+$1.5 bn), liquidity factor ETFs (+$0.9 bn), and ETFs using the quality factor (+$0.8 bn).

Graph 14: Estimated Net Flows of Single Factors Within the Segment of Factor-Based ETFs – January 1, 2025 – January 31, 2025 (in bn USD)

Source: LSEG Lipper

On the other side of the fund flows league table, factor-based ETFs using the value factor (-$2.8 bn) were facing the highest outflows. The category was bettered by ETFs using the volatility factor (-$0.5 bn) and ETFs using the credit quality factor (-$0.2 bn).

Global ETF Flows in ESG-Related ETFs

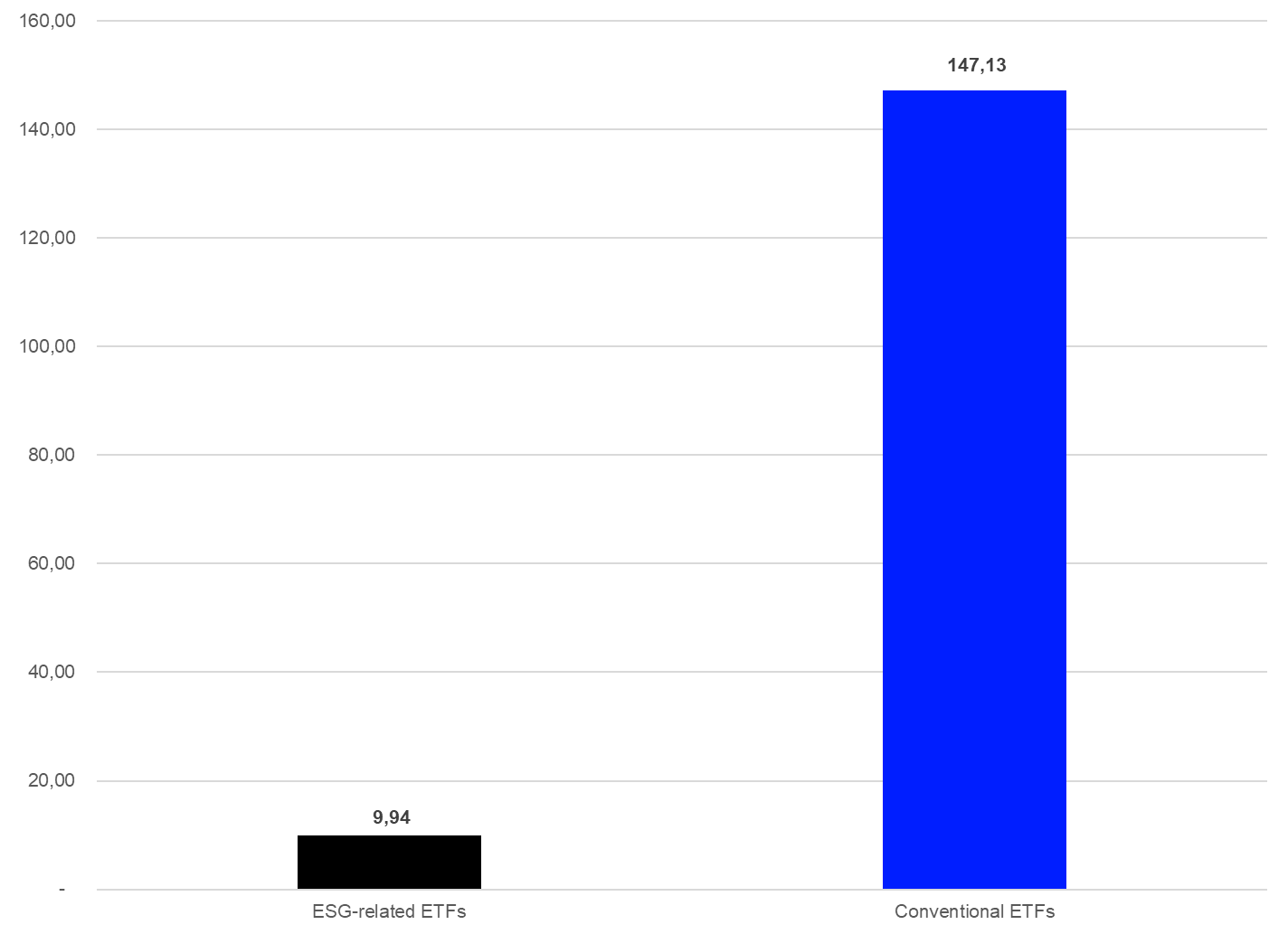

Given the fact that sustainable investing is a hot topic in the global investment industry, it is surprising that ESG-related ETFs enjoyed estimated net inflows of only $9.9 bn over the course of January. These inflows must be seen in the light of the still ongoing discussions about greenwashing and regulatory issues, as well as political headwinds in some jurisdictions.

Graph 15: Estimated Net Flows in the Global ETF Industry ESG-related ETFs vs Conventional ETFs – January 1, 2025 – January 31, 2025 (in bn USD)

Source: LSEG Lipper

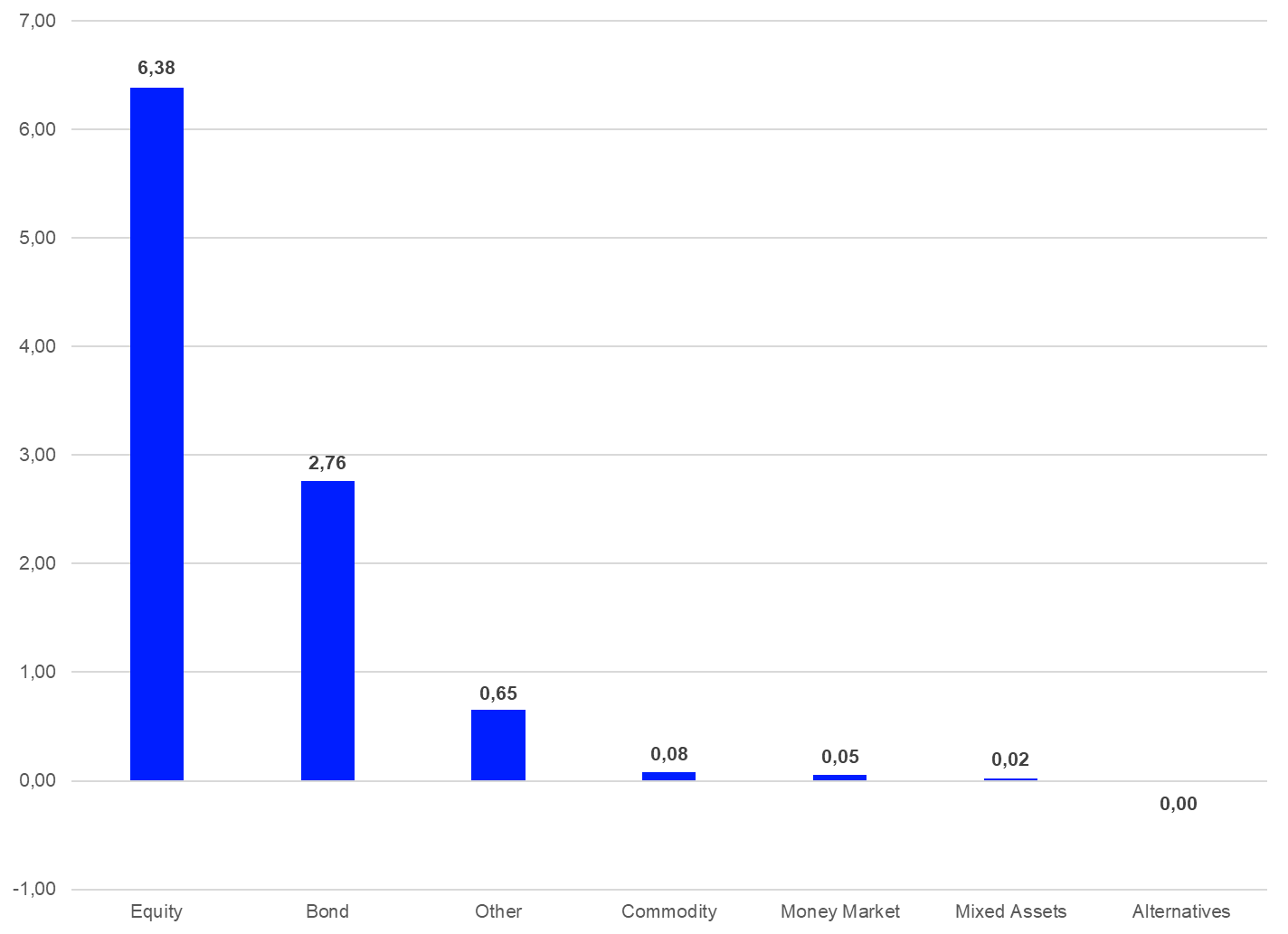

With regard to the overall market structure and the general fund flow trend, it is not surprising that equity ETFs (+$6.4 bn) enjoyed the highest estimated net inflows in the segment of ESG-related ETFs for January. They were followed by bond ETFs (+$2.8 bn), “other” ETFs (+$0.7 bn), commodities ETFs (+$0.1 bn), money market ETFs (+$0.05 bn), and mixed-assets ETFs (+$0.02 bn). On the other side of the table, alternatives ETFs (-$0.002 bn) were the only asset type which faced outflows.

Graph 16: Estimated Net Flows of ESG-related ETFs by Asset Type – January 1, 2025 – January 31, 2025 (in bn USD)

Source: LSEG Lipper

Global ETF Flows by Region

By reviewing the estimated flows in the global ETF industry by fund domicile and the respective regions, one needs to bear in mind that some domiciles have specific advantages or disadvantages when it comes to ETF distribution. The U.S. is, for example, a single market and can take profit from the size of the overall market, while in Europe every market is or at least can be an ETF domicile, which means that the local markets are much smaller.

That said, the EU countries have established a fund regulation (Undertakings in Collective Investments and Transferable Securities, or UCITS) which enables the fund and ETF industry to cross-list all products which are registered for sale in one EU country into another EU country. Since UCITS has become such a well-recognized regulatory standard for mutual funds and ETFs, some countries in South and Central America, as well in Asia, allow UCITS funds to be cross-listed and sold to local investors. It is fair to say that there is no other regulatory framework available that allows funds to be distributed in various countries around the globe. Other mutual recognition agreements, such as those between Hong Kong and China or Hong Kong and Taiwan, are only bilateral and have no global reach. This means that the estimated flows for European ETFs in January also include flows from South and Central America, as well as from Asia.

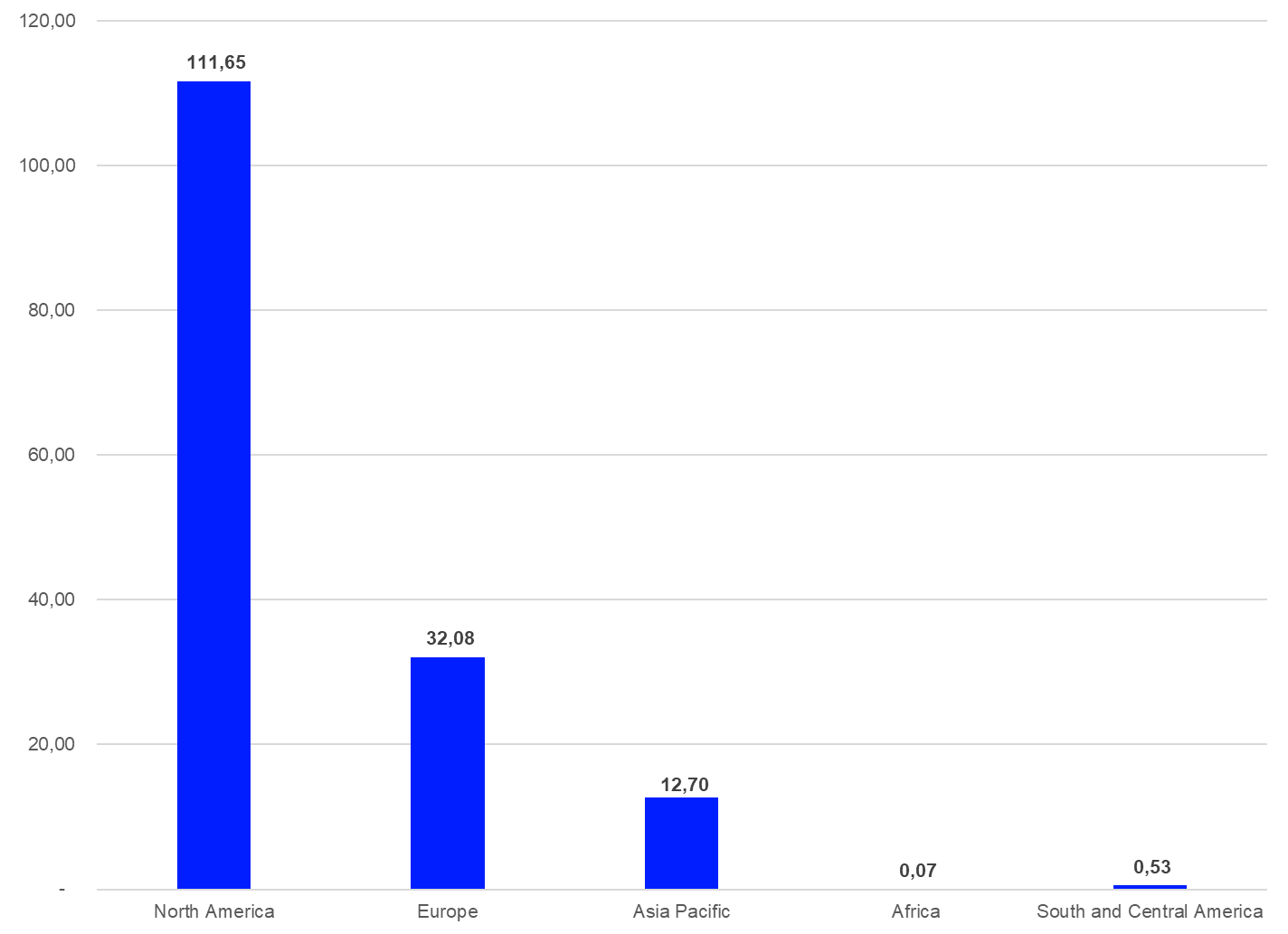

As to be expected, ETFs domiciled in North America (+$111.7 bn) enjoyed the highest estimated net inflows for January 2025. They were followed by ETFs domiciled in Europe (+$32.1 bn), Asia Pacific (+$12.7 bn), South and Central America (+$0.5 bn), and (South) Africa (+$0.1 bn).

Graph 17: Estimated Net Flows in the Global ETF Industry by Region, January 1, 2025 – January 31, 2025 (in bn USD)

Source: LSEG Lipper

In more detail, the U.S. (+$104.7 bn) was the single fund domicile with the highest estimated net inflows for January. It was followed by Ireland (+$23.3 bn) and Luxembourg (+$7.2 bn).

Global ETF Flows by Asset Type

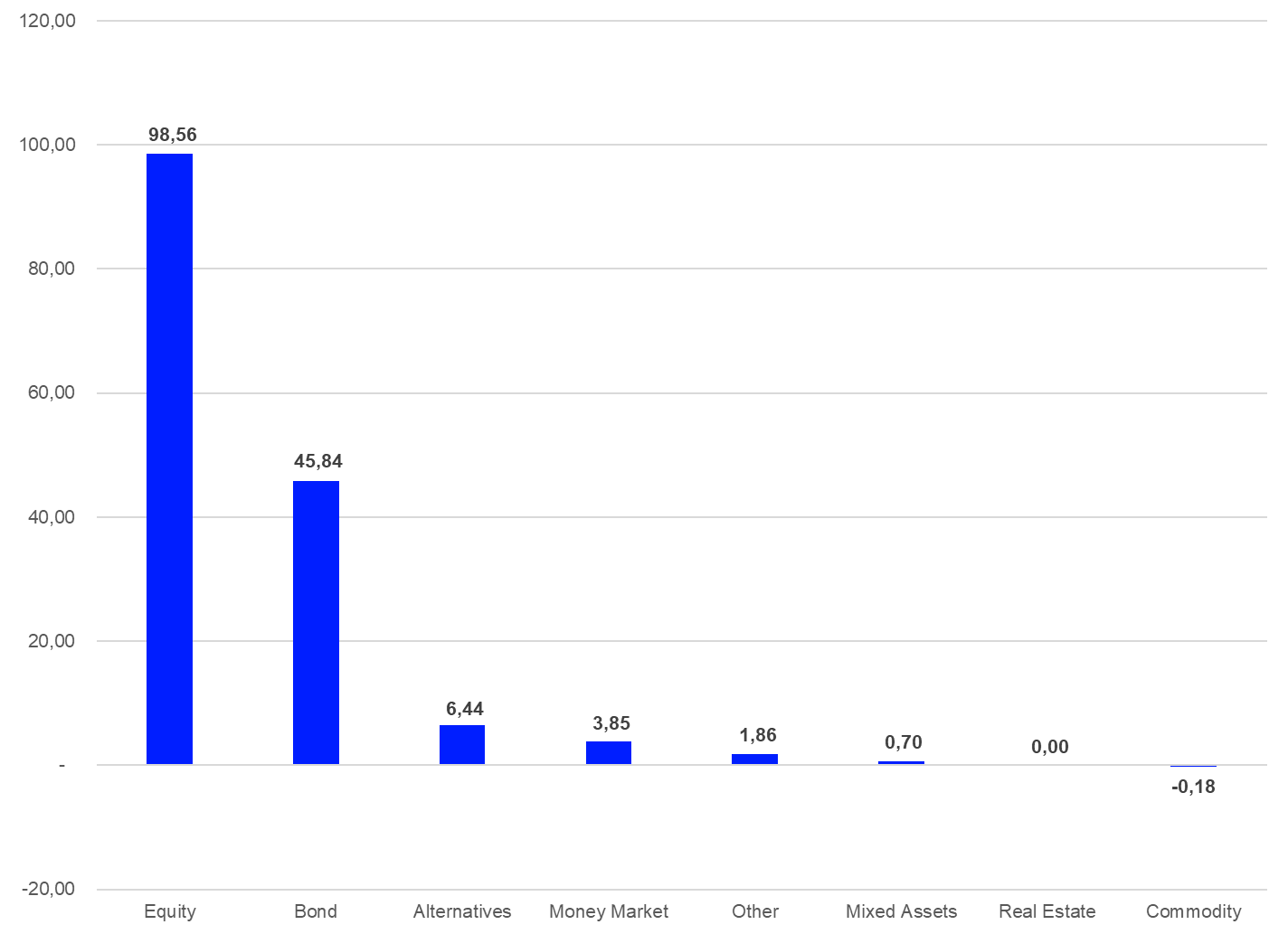

Given the overall market environment, it was not surprising that equity ETFs (+$98.6 bn) were the best-selling asset type for January 2025. They were followed by bond ETFs (+$45.8 bn), alternatives ETFs (+$6.4 bn), money market ETFs (+$3.9 bn), “other” ETFs (+$1.9 bn), mixed-assets ETFs (+$0.7 bn), and real estate ETFs (+$0.004 bn). On the other side of the table, commodities ETFs (-$0.2bn) were the only asset type which faced outflows over the course of the month.

Graph 18: Estimated Net Sales by Asset Type, January 1, 2025 – January 31, 2025 (in bn USD)

Source: LSEG Lipper

The fact that equities were the best-selling asset type for the month might be a sign that investors are further in risk-on mode with regard to their risk appetite. In addition, the inflows into bond ETFs could be seen as a sign that investors might adapt to the ending of the interest hiking cycle of central banks around the globe. Therefore, this positioning might be seen as a bet that inflation will decrease further.

Global ETF Flows by Lipper Global Classifications

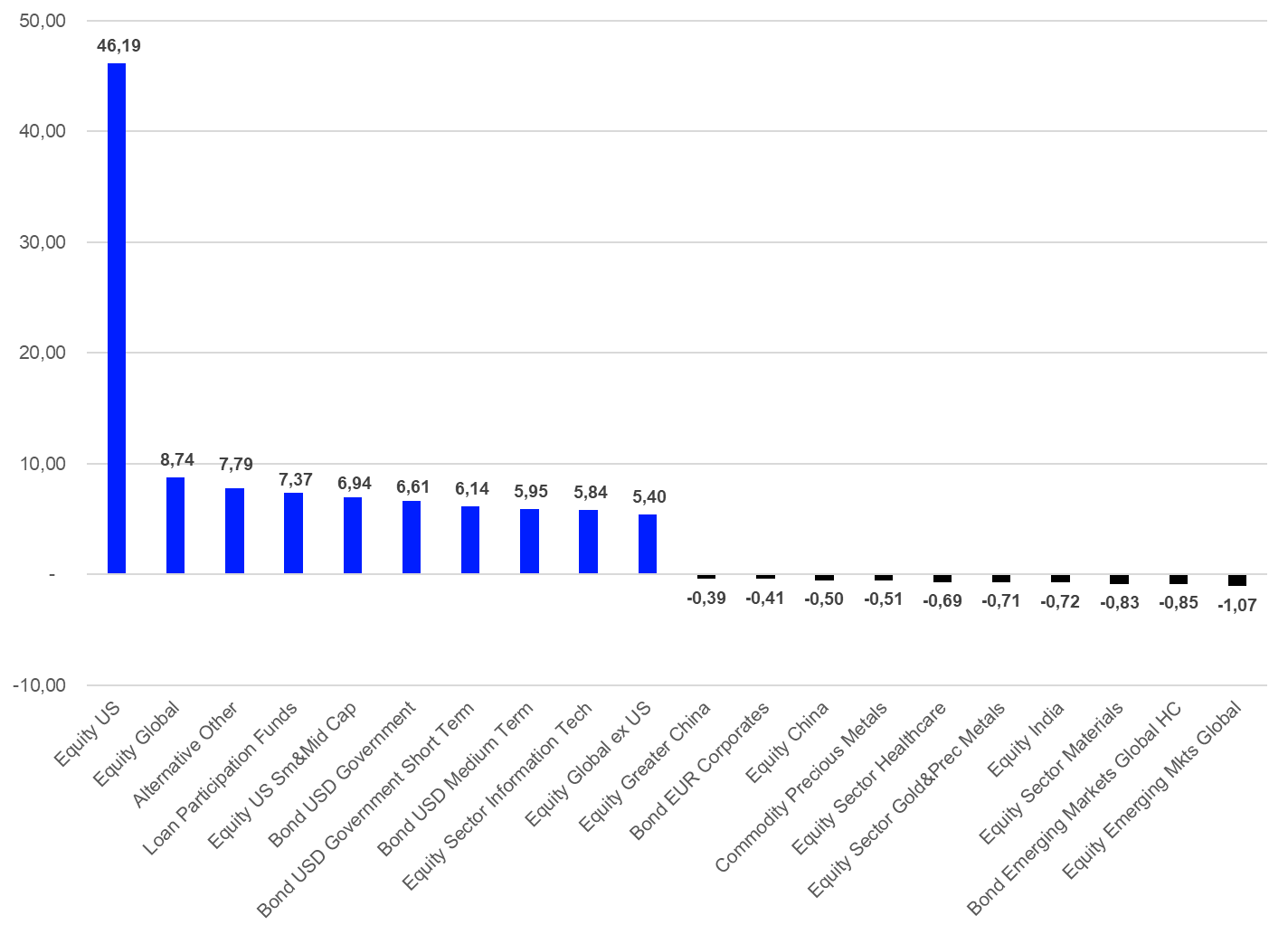

A closer look at the best and worst Lipper Global Classifications by estimated net flows for January shows that investors are further in risk-on mode with regard to their risk appetite. This is because the table of the 10 best-selling Lipper Global Classifications is composed of five equity, three bond, and two alternatives classifications. Equity U.S. (+$46.2 bn) was once again the best-selling classification for the month. The category was followed by Equity Global (+$8.7 bn), Alternative Other (+$7.8 bn), Loan Participation Funds (+$7.4 bn), and Equity U.S. Small and Mid-Caps (+$6.9 bn).

Graph 19: Ten Best- and Worst Lipper Global Classifications by Estimated Net Sales, January 1, 2025 – January 31, 2025 (in bn USD)

Source: LSEG Lipper

On the other side of the table, Equity Emerging Markets Global (-$1.1 bn) faced the highest outflows. The category was bettered by Bond Emerging Markets Global in Hard Currencies (-$0.9 bn), Equity Sector Materials (-$0.8 bn), Equity India (-$0.7 bn), and Equity Sector Gold & Precious Metals (-$0.7 bn).

More generally, the flow trends for the classifications with the highest estimated outflows in January indicate that investors are adjusting their portfolios to the current economic environment.

Global ETF Flows by Promoters

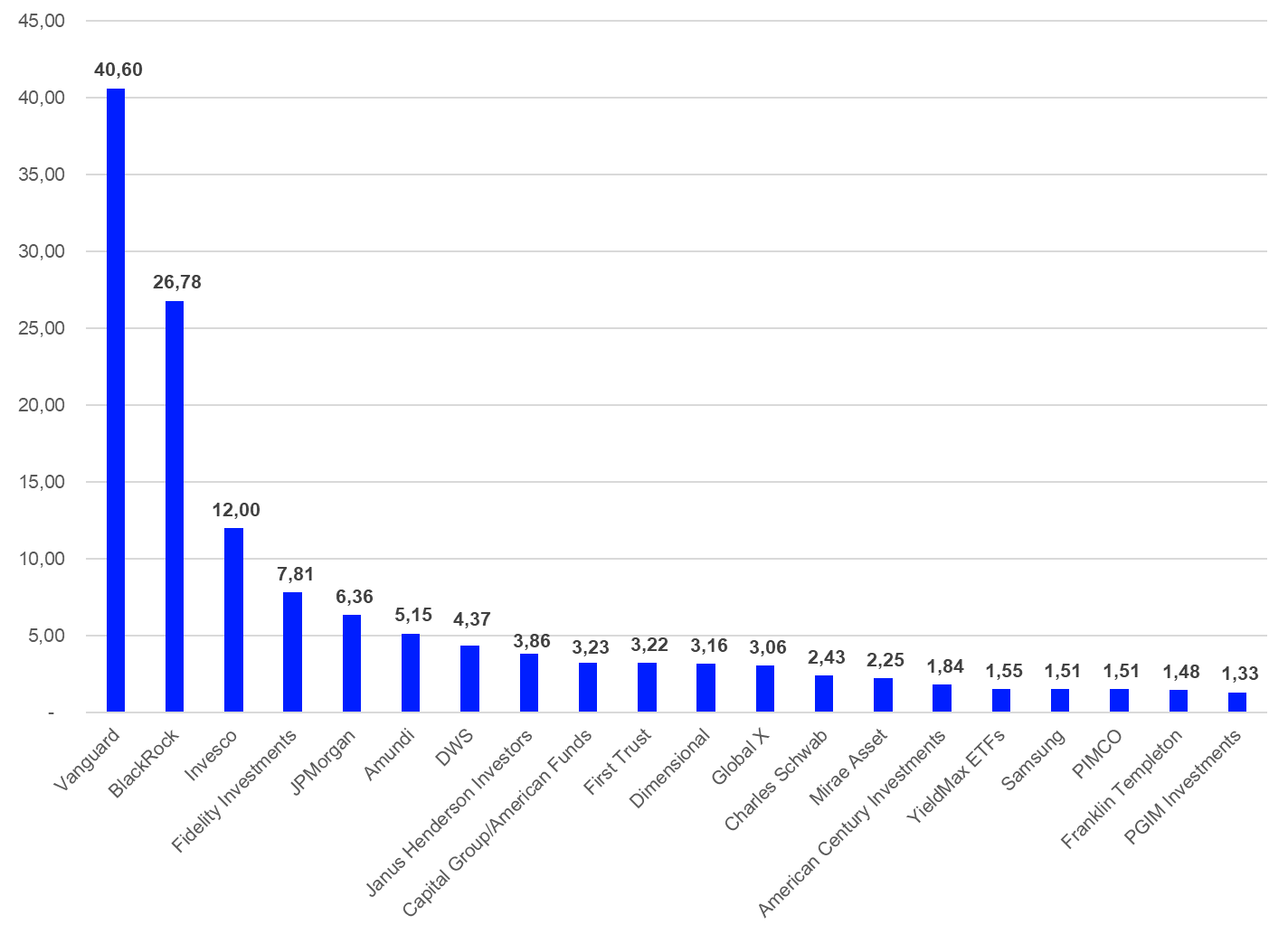

Vanguard (+$40.6 bn) was the best-selling ETF promoter globally for the month, ahead of BlackRock (iShares) (+$26.8 bn), Invesco (+$12.0 bn), Fidelity Investments (+7.8 bn), and JPMorgan (+6.4 bn).

Graph 20: Twenty Best-Selling ETF Promoters Globally, January 1, 2025 – January 31, 2025 (in bn USD)

Source: LSEG Lipper

Overall, the 20 best-selling ETF promoters account for estimated net inflows of $133.5 bn.

This article is for information purposes only and does not constitute any investment advice.

The views expressed are the views of the author, not necessarily those of LSEG.