Climate change is one of the major issues of our time, and the (hopeful) transition to a more climate-friendly economy presents both risks and opportunities for investors. Thus, many savvy investors are considering a company’s carbon footprint in their bottom-up company analysis. However, more than 80% of returns and risk over a longer (10+ year) time horizon are attributable to the strategic asset allocation, ie. how much to be invested broadly in certain countries and sectors, rather than in which specific companies.

Therefore, long-term investors are considering climate change in their overall economic assumptions that drive their asset allocation decisions. Climate risk can be broadly broken into physical risks — like wildfires, severe weather, or assets being under water (literally, not financially), and transition risks — like decreasing demand for fossil fuels.

Climate Scenario Analysis

According to a recent report by Ortec Finance for OPTrust, one of Canada’s largest pensions, physical risks are likely to manifest as of mid-century, and over the next decade, transition risks are key. Canada is relatively less vulnerable to physical risks, but with 20% of our exports coming from direct fossil fuel exports, and a relatively high marginal cost of producing fossil fuels, Canada is vulnerable to transition risks. Countries or regions that are better positioned to handle this transition could be seen as safe-havens by large institutional investors, and would therefore make good long-term investments. Canada is the 10th largest economy in the world.

We will look at how the rest of the 10 largest economies compare from a transitional climate-risk perspective, and which countries investors who are concerned about disruption from climate change might consider greater exposure to.

Metrics for Comparison

- First we consider the country’s GDP per unit of energy use (in this case kg of oil equivalent) to see which countries are the most, and least, energy efficient.

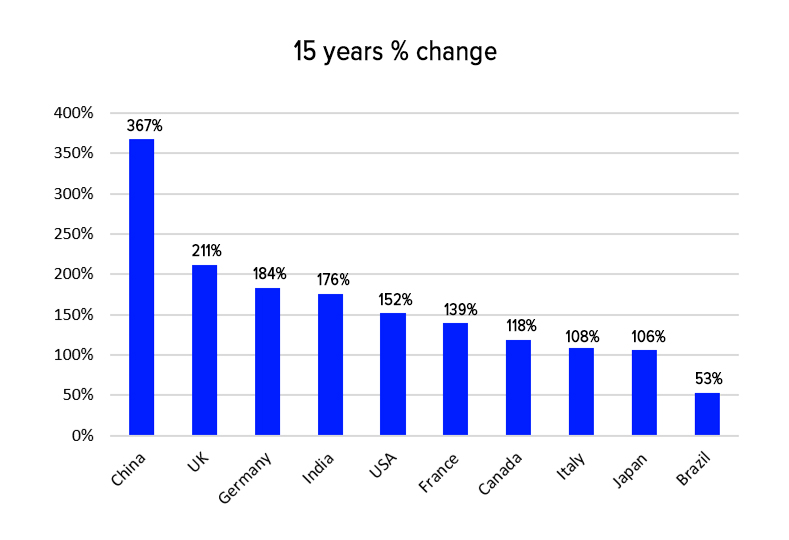

- Secondly we look at how this is trending, measured by the percent change over the past 15 years.

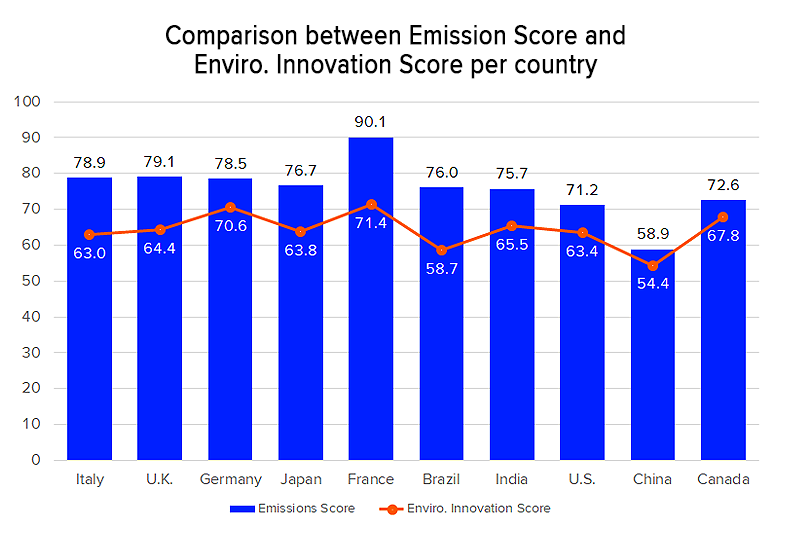

- Finally we will consider the company’s in that countries Refinitiv ESG scores. We will take the market-cap weighted average Emissions score and Environmental Innovation scores.

- The final column is how these countries rank relative to each other if all 4 data points are given equal consideration.

Europe Appears to be the Best Prepared

Europe appears to clearly be the most resilient to transitional climate change risk, with the 4 European countries ranking 1-4, topped by the UK. Investors interested in broad, passive exposure to Europe could consider Vanguard’s European Stock Index ETF (VGK) with a 0.09% MER. For pure UK exposure there is Franklin Templeton’s FTSE United Kingdom ETF, also with a 0.09% MER.

And for those interested in a more active, stock-picking approach, Persimmon (PSN.L) is a UK homebuilder that scores in the 100th percentile in Refinitiv’s StarMine Combined Alpha Ranking, and has the maximum amount of exposure to the UK economy as measured by Refinitiv’s StarMine Country of Risk Model.