U.S. investors pushed equity funds to their fifth consecutive quarter of plus-side performance in Q2 2021 as they focused on the reopening of global economies, a commitment by the Federal Reserve Board to keep its easy money policy intact, and a goldilocks U.S. nonfarm payrolls report for May. For Q2 2021, the average equity fund and taxable fixed income fund posted a 6.36% and 1.55% return, respectively.

However, flows into mutual funds and ETFs continued to favor fixed income funds as investors evaluated the loftiness of equity prices and the global spread of the delta variance of the coronavirus while remaining concerned about inflation. Nonetheless, in a quasi-flight to safety and continued search for yield, bond investors pushed the 10-year Treasury yield down 29 basis points (bps) for Q2 to 1.45%.

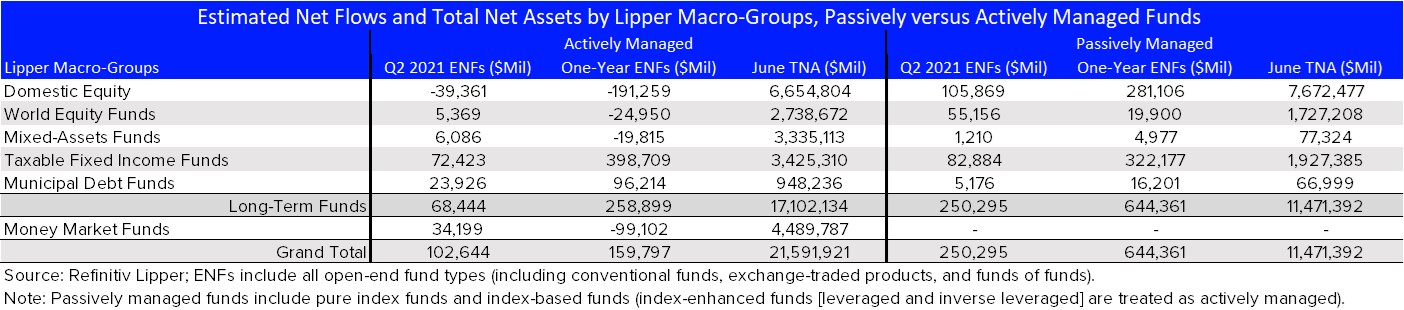

Long-term funds (equity and fixed income funds and ETFs, excluding money market funds) attracted some $318.7 billion for Q2. However, like in prior quarters, investors gravitated toward fixed income instruments, injecting $184.4 billion into taxable and tax-exempt fixed income funds, while their equity and mixed-assets fund cousins attracted $134.3 billion for the quarter.

Over the last few years, passively managed equity funds and ETFs outdrew their actively managed counterparts, while investors appeared to prefer actively managed fixed income products over passive.

However, for Q2, passively managed taxable fixed income funds (+$82.9 billion) outdrew actively managed taxable fixed income funds (+$72.4 billion) for the first time in recent memory. That said, actively managed municipal debt funds (+$23.9 billion for Q2) still outdrew their passively managed counterparts (+$5.2 billion).

Taking another slice of the data shown above and focusing on socially responsible investing (SRI) funds and the more recent emphasis on environmental, social, and governance (ESG) focused investment/screening practices, we saw similar passive versus active fund-flows trends for the quarter, while in contrast, actively managed taxable fixed income SRI/ESG funds still outdrew their passively managed cohorts for the quarter ended June 30, 2021.

Investors injected some $20.9 billion into SRI- and ESG-focused mutual funds and ETFs (collectively, responsible investing [RI] funds) during Q2 2021, bringing the one-year net inflows total to $70.4 billion.

In contrast to Q1 2021, estimated net flows into long-term RI funds for Q2—excluding money markets funds again—significantly favored passively managed RI funds (+$10.8 billion) over their actively managed RI brethren (+$5.9 billion). In comparison to their non-RI fund counterparts in both the active versus passive breakouts, all the Lipper RI fund macro-groups witnessed net inflows, including actively managed domestic equity RI funds. So, on the RI side of the fence, investors continue to embrace actively managed domestic equity funds while shunning actively managed domestic equity funds on the non-RI side.

We have written in the past about the stickiness of assets in this RI subset. Investors appear to be willing to put their money where their convictions are generally for the long haul when it comes to socially responsible investing practices.

Total asset under management continued to favor actively managed RI fund (+$537.2 billion) over their passively managed counterparts (+$127.2 billion). As we have mentioned before, this is more than likely a result of investors’ long-term commitment to SRI practices seen as early as the 1920s in the U.S., when one of the first publicly available SRI funds (Pioneer Fund) used negative screening practices to exclude tobacco, alcohol, and gambling investments from its portfolio. Since then, socially aware practices have continued to evolve and recently take on a more mainstream focus by investors as ESG pillars become standard metrics of investment evaluations.

Find out more about Refinitiv Lipper, one of the global leaders in independent fund performance data.

Join a growing community of asset managers and stay up to date with the latest research from Refinitiv and partners to help you inform your investment decisions. Follow our Asset Management LinkedIn showcase page.