Most pundits expect the Federal Reserve Board to start a gradual withdraw of its easy money policies in the near term. And while Fed Chair Jerome Powell stated at the end of the annual Jackson Hole Economic Symposium on August 27, 2021, “if the economy evolved broadly as anticipated, it could be appropriate to start reducing the pace of asset purchases this year,” he reiterated that the decision to taper the Fed’s $120 billion monthly asset purchases doesn’t mean it will be raising interest rates at the same time.

Bond investors have eagerly awaited news on the proposed timing of the Fed’s plans to begin tapering and have been looking for hints of when rates may start to rise. The combination of low interest rates and signs of rising inflation have investors concerned. The prospects of higher interest rates, while eagerly awaited, is a double-edged sword that will cause the value of current bonds to decline. Recall the inverse relationship between interest rates and bond prices. Most bond investors are hoping that the inevitable rate hikes occur at a slow enough pace that the extra added yield will compensate for the decline in value—from a bond fund perspective.

On Friday, September 3, the Department of Labor threw a wrench into the works after reporting the U.S. economy added just 235,000 jobs in August, far lower than the 720,000 forecasted by analysts. While some investors viewed the report as a reason for the Federal Reserve to delay its long-anticipated plan to taper its asset purchases, others were concerned by the combination of a slowdown in hiring with a surge in wage growth—a worrisome combination for the economy.

Most fixed income investors are not sure how to prepare for the end of a 40-year bull market in bonds. Until recently bond investors have benefitted from declines in interest rates and low relative inflation, leading to both capital gains and income distributions contributing to total returns for bond funds. And that is possibly on the verge of change.

With the graying of America, the proportional asset allocation away from stock funds (including ETFs) and into bond funds has grown considerably—rising from just a little less than 14% (+$1.4 trillion) of all assets under management in the U.S. fund business for 2008 to almost 20% (+$6.6 trillion) in 2021—see the dark blue segments in the chart below. Much of this now is on autopilot with automatic monthly investments into 401(k) and other qualified plans earmarked toward fixed income mutual funds and ETFs.

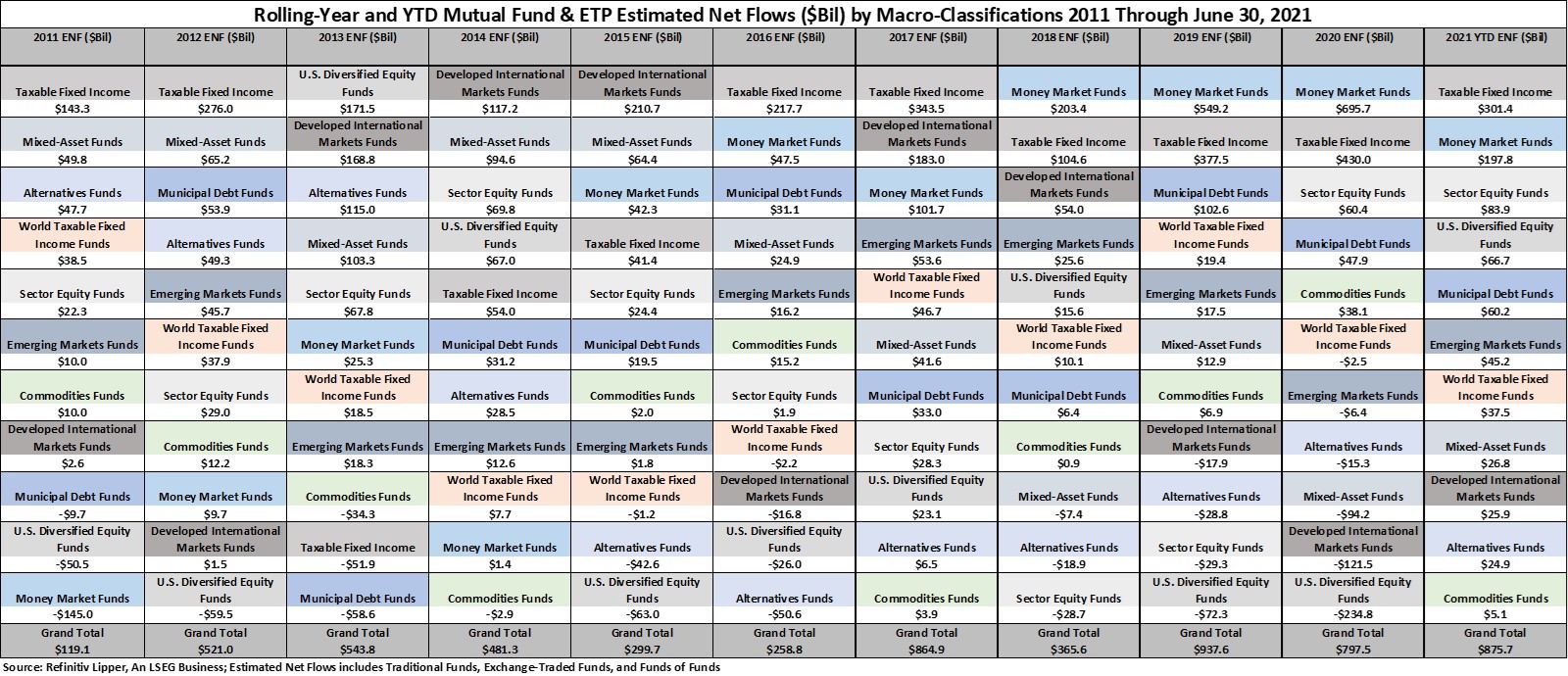

Even as pundits continue to raise the alarm of the impact rising interest rates might have on bond funds, investors continue to inject net new money into both taxable and tax-exempt bond funds, with the former being a primary attractor of investors’ assets in eight of the last 11 years, including through Q2 2021.

Concerns of perceived lofty valuations in the equity market have given taxable fixed income funds the continued advantage over equity funds in the fund-flows arena despite the concerns of rising interest rates and growing inflation. So far for Q3 (through the fund-flows week ended September 8, 2021), taxable bond funds (including ETFs) have attracted the largest amount of net inflows, taking in $81.6 billion, followed by equity funds (+$61.2 billion) and municipal bond funds (+$23.4 billion), while money market funds (-$36.0 billion) have suffered net redemptions.

And while Core Bond Funds (aka corporate investment-grade bond funds) have been the primary attractor of investors’ assets year to date—attracting $103 billion—we’ve seen a recent influx of investors padding the coffers of Short Investment-Grade Debt Funds (+$51.1 billion, YTD), Inflation Protected Bond Funds (+$47.8 billion), Multi-Sector Income Funds (+$39.6 billion), and Loan Participation Funds (+$33.5 billion) as investors and their advisors look for fixed income funds that might weather the nascent rise in interest rates better than other longer dated/higher duration products.

In fact, for Q3 so far, Short Investment-Grade Debt Funds have outdrawn all other taxable fixed income fund classifications, taking in a little under $15.8 billion, followed by Inflation Protected Bond Funds (+$10.5 billion), Multi-Sector Income Funds (+$9.7 billion), Core Bond Funds (+$7.7 billion), and Loan Participation Funds (+$5.7 billion). We have also seen a recent interest in funds that focus on real assets and income-oriented equity gaining a little traction, with equity income funds and sector real-estate funds taking in $7.9 billion and $2.9 billion, respectively, for Q3 as investors seek alternative income opportunities in a possible rising interest rate environment.

Refinitiv Lipper delivers data on more than 330,000 collective investments in 113 countries. Find out more.

Join a growing community of asset managers and stay up to date with the latest research from Refinitiv and partners to help you inform your investment decisions. Follow our Asset Management LinkedIn showcase page.