Unsurprisingly, given the increase in volatility in equity markets during the Refinitiv Lipper fund-flows week ended September 22, 2021, investors turned their backs on equity ETFs and mutual funds, redeeming a net $6.7 billion, while padding the coffers of taxable (+$5.9 billion) and tax-exempt (+$1.6 billion) bond funds (including ETFs).

During the flows week, investors shrugged off a better-than-expected August retail sales figure that handily beat analyst expectations and news that the Philadelphia Fed’s September activity index almost doubled from the prior month. Instead, they focused on the potential default by China’s giant property company Evergrande, U.S. debt ceiling jitters, and news from the Federal Reserve Board’s September policy setting meeting. The two former were drags on performance, while the latter sent markets to their best one-day rally in two months.

It truly was a tale of two cities this week when viewing stock performance. The Dow witnessed its worst one-day decline (-614.41 points, -1.8%) in nine weeks on Monday, September 20, as debt default concerns for China’s Evergrande rattled the market. Equities took a beating as investors evaluated the possible impact a default by debt laden Evergrande might have on the broader market and after the CBOE Market Volatility Index (VIX) jumped to its highest level (28.47%) since May.

However, by the end of the fund-flows week, talks of restructuring Evergrande and news that China’s central bank reportedly injected liquidity into its markets helped ease some of the initial concerns in the markets of a potential financial contagion similar to what occurred when Lehman Brothers failed in 2008. For the day, the Dow, NASDAQ Composite, and S&P 500 each closed up about 1.0%

Performance

The average equity fund was only down 0.07% for the fund-flows week. Natural Resources Funds (+1.75%, including ETFs) posted the strongest returns for the week in the equity universe, followed by Small-Cap Growth Funds (+1.10%), Commodities Base Metals Funds (+1.09%), and Financial Services Funds (+1.07%) as investors turned to out-of-favor and cyclical issues. Precious Metals Equity Funds (-3.21%, aka gold miners funds) witnessed the largest declines for the week, bettered by Utility Funds (-1.63%).

In addition, investors cheered the Fed’s decision to keep its bond-buying program and interest rates unchanged—at least for now. Stocks trimmed some of the early day gains after Federal Reserve Chair Jerome Powell said plans to taper its bond buying program could be announced at the Fed’s November FOMC meeting and it could start raising interest rates in 2022. Despite some mid-flows-week swings, the 10-year Treasury yield finished the week up just one basis point to 1.32% (although it did see a nine basis points increase on Thursday, September 23, closing at 1.41%).

The average taxable fixed income fund declined 0.25% for the week, with Loan Participation Funds (+0.05%, aka leveraged or bank loan funds) and Short High Yield Funds (+0.01%) posting the only positive returns of the classifications in the fixed income universe. Emerging Markets Hard Currency Debt Funds (-0.81%) experienced the largest losses for the flows week, followed by Emerging Markets Local Currency Debt Funds (-0.75%), General U.S. Treasury Funds (-0.71%), and Inflation Protected Bond Funds (-0.58%).

Fund Flows

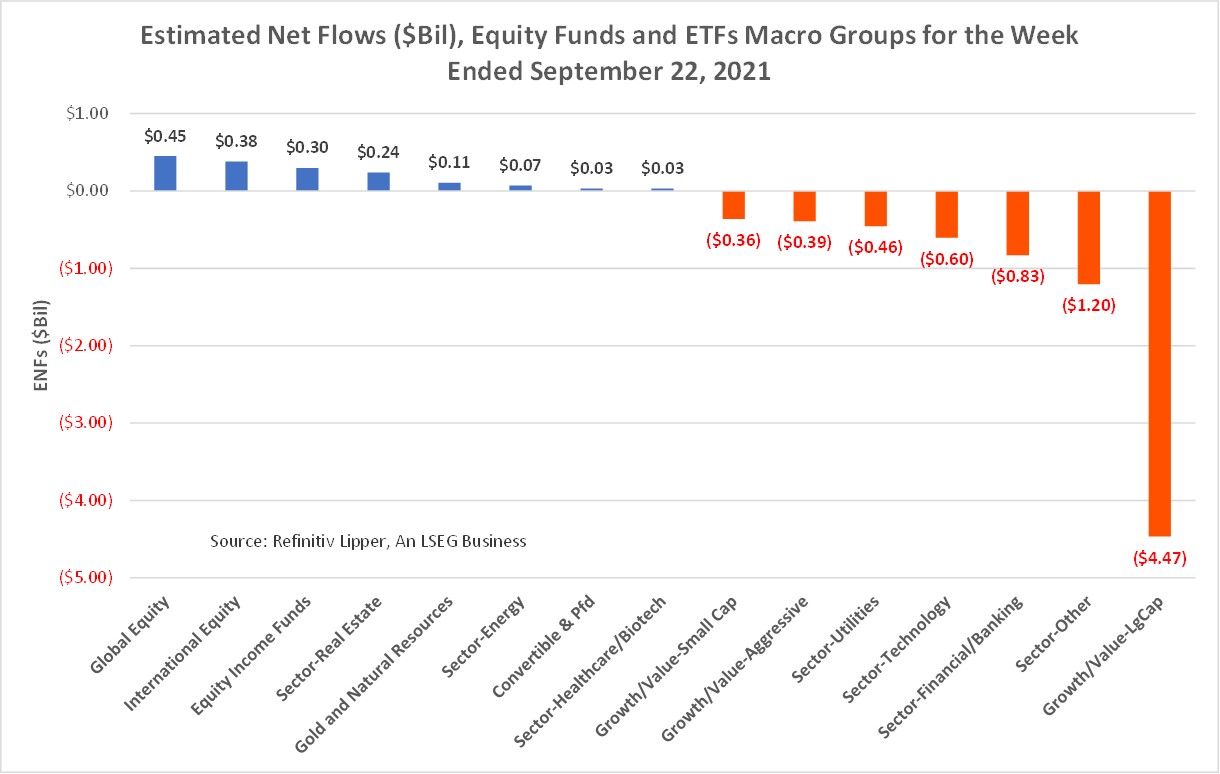

While equity funds (including ETFs) witnessed net outflows of $6.7 billion for the fund-flows week, the lion’s share was primarily attributed to a $4.5 billion outflows from large-cap funds and $1.2 billion from the commodities-heavy sector-other macro-group. We did also see net inflows in global equity funds (+$451 million) and international equity funds (+$380 million). In the equity fund and ETF universe, ProShares UltraPro QQQ ETF (TQQQ, +$1.1 billion), ProShares S&P 500 Dividend Aristocrats ETF (NOBL, +$986 million), and John Hancock Disciplined Value Mid Cap Fund, Institutional Share Class (JVMIX, +$570 million) individually attracted the largest amounts of net new money, while SPDR S&P 500 ETF (SPY, -$4.0 billion) and Invesco S&P 500 Equal Weight ETF (RSP, -$1.5 billion) experienced the largest individual net redemptions of the week.

Taxable Bond Funds (+$5.9 billion) attracted the largest net inflows of the four broad macro-groups this week, bringing their string of net inflows to 40 consecutive weeks. With uncertainty in the bond markets on the rise, given the Fed telegraphing its likely tapering of bond purchases in November and possible hike in interest rates in 2022, investors injected the largest amount of net new money this week into government-Treasury funds and ETFs (+$2.3 billion). They were followed by the go-anywhere flexible funds (+$1.8 billion) macro group, corporate investment grade debt funds (+$1.5 billion), and corporate high-yield funds (+$536 million). International & global debt funds (-$254 million) experienced the largest weekly net outflows, bettered by government-Treasury & mortgage funds (-$116 million).

In the taxable fixed income universe, iShares 20+ Year Treasury Bond ETF (TLT, +$621 million), iShares iBoxx $ High Yield Corporate Bond ETF (HYG, +$552 million), and iShares 7-10 Year Treasury Bond ETF (IEF, +$516 million) attracted the largest amounts of net new money of all individual taxable fixed income ETFs. Meanwhile, MetWest Total Return Bond Fund, I Shares (MWTIX, -$1.5 billion), iShares iBoxx $ Investment Grade Corporate Bond ETF (LQD, -$857 million), and SPDR Bloomberg Barclays High Yield Bond ETF (JNK, -$527 million) handed back the largest individual net redemptions for the week.

Refinitiv Lipper delivers data on more than 330,000 collective investments in 113 countries. Find out more.

Join a growing community of asset managers and stay up to date with the latest research from Refinitiv and partners to help you inform your investment decisions. Follow our Asset Management LinkedIn showcase page.