European investors were further in a risk-on mode over the course of September despite the increased volatility in securities markets. Given the general market environment, it was no surprise that September 2021 was a month with mixed results for the European fund industry since the promoters of mutual funds (-€20.5 bn) faced outflows, while the promoters of ETFs (+€13.0 bn) enjoyed inflows. The overall flow pattern in Europe showed that investors continued to be in risk-on mode in September as the general flow pattern was driven by money market products. In more detail, investors bought further into risky assets as long-term funds (+€48.7 bn) enjoyed inflows, while money market products (-€56.2 bn) faced high estimated net outflows. In line with this, Equity Global (+€10.4 bn) was the best-selling Lipper Global Classification for the month.

In more detail, equity funds (+€15.9 bn) were the best-selling asset type overall for the month. The category was followed by bond funds (+€15.1 bn), mixed-assets funds (+€13.3 bn), alternative UCITS funds (+€3.1 bn), real estate funds (+€2.4 bn), and commodities funds (+€0.03 bn). On the other side of the table, “other” funds (-€1.1 bn) and money market funds (-€56.2 bn), were the only asset types showing outflows.

Graph 1: Estimated Net Flows by Asset and Product Type – September 2021 (Euro Billions)

Source: Refinitiv Lipper

Money Market Products

With a market share of 9.84% of the overall assets under management in the European fund management industry, money market products are the fourth largest asset type. Therefore, it is worthwhile to briefly review the trends in this market segment. As the market environment normalized further, with the situation around the COVID-19 pandemic easing up, it was not surprising that European investors reduced their money market positions over the course of the year so far. In line with this expectation, money market funds faced outflows for the month (-€56.2bn) even as the volatility on the securities market increased. In line with their active peers (-€56.7bn), ETFs investing in money market instruments contributed estimated net outflows of €0.1 bn to the total.

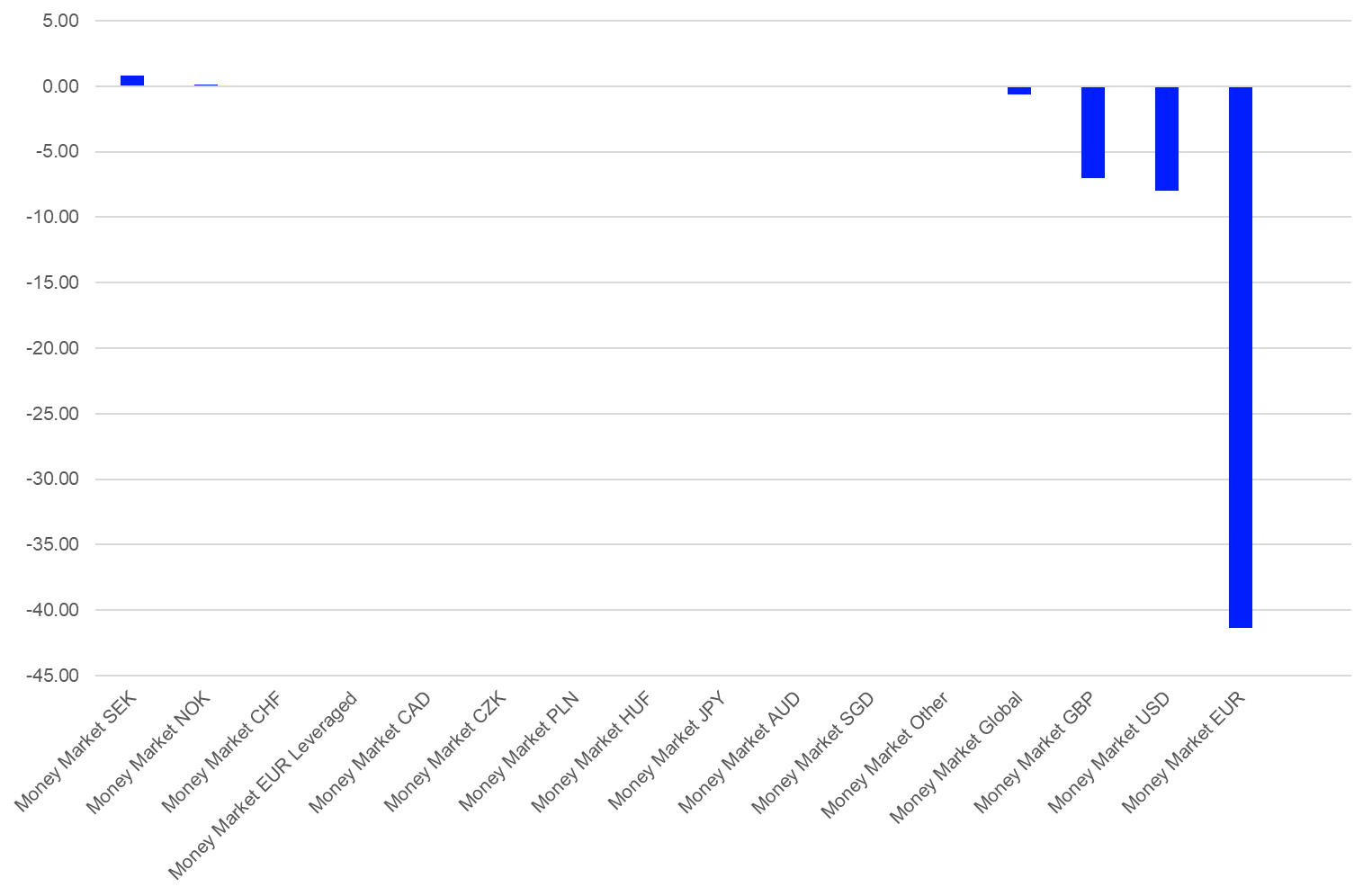

Money Market Products by Lipper Global Classification

In more detail, Money Market SEK (+€0.8 bn) was the best seller within the money market segment, followed by Money Market NOK (+€0.1 bn) and Money Market CHF (+€0.04 bn). At the other end of the spectrum, Money Market EUR (-€41.4 bn) suffered the highest net outflows overall, bettered by Money Market USD (-€8.0 bn) and Money Market GBP (-€7.0 bn).

This flow pattern revealed that European investors sold money market products denominated in the euro, USD, and GBP, while not buying back other money market products. These flows might be a sign that European investors are still in a risk-on mode even as the volatility in the securities market has increased over the course of the month. In conjunction with the asset allocation decisions of portfolio managers, these shifts in the money market segment might have also been caused by corporate actions such as cash dividends or cash payments, since money market funds are also used by corporations as replacements for cash accounts.

Graph 2: Estimated Net Flows in Money Market Products by LGC – June 2021 (Euro Billions)

Source: Refinitiv Lipper

Fund Flows by Lipper Global Classifications

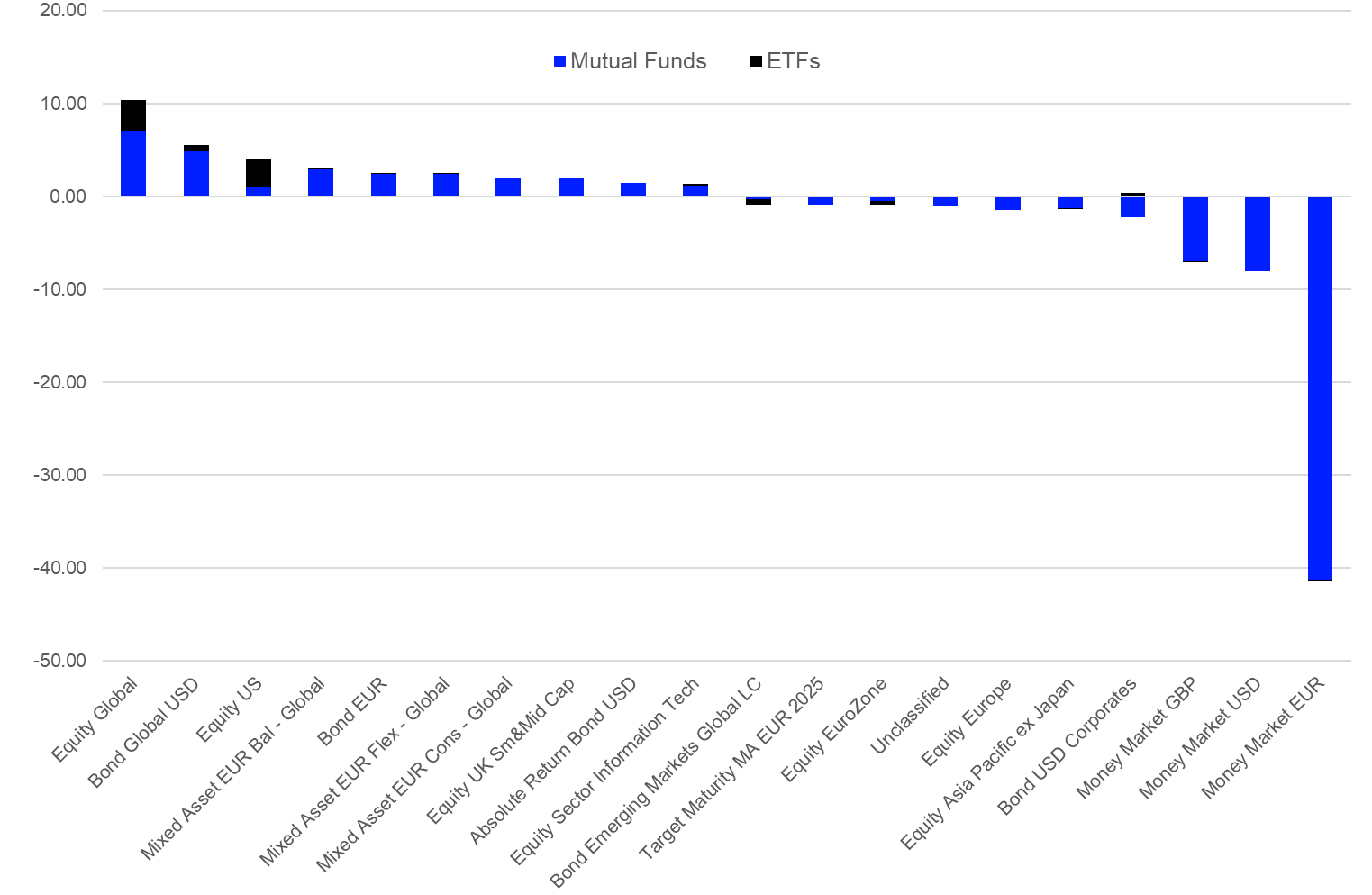

With regard to the overall sales for September, it was not surprising that Equity Global (+€10.4 bn) dominated the table of the 10 best-selling peer groups by estimated net flows. It was followed by Bond Global USD (+€5.5 bn), Equity US (+€4.1 bn), Mixed Assets EUR Balanced – Global (+€3.0 bn), and Bond EUR (+€2.5 bn).

Graph 3: Ten Best- and Worst-Selling Lipper Global Classifications by Estimated Net Sales, September 2021 (Euro Billions)

Source: Refinitiv Lipper

On the other side of the table, Money Market EUR (-€41.4 bn) faced the highest estimated net outflows for September, bettered by Money Market USD (-€8.0 bn) and Money Market GBP (-€7.0 bn).

It is noteworthy that the estimated flows in money market sectors are not only a reflection of asset allocation decisions of investors since these products are also used by corporates as a replacement for cash accounts.

Fund Flows by Promoters

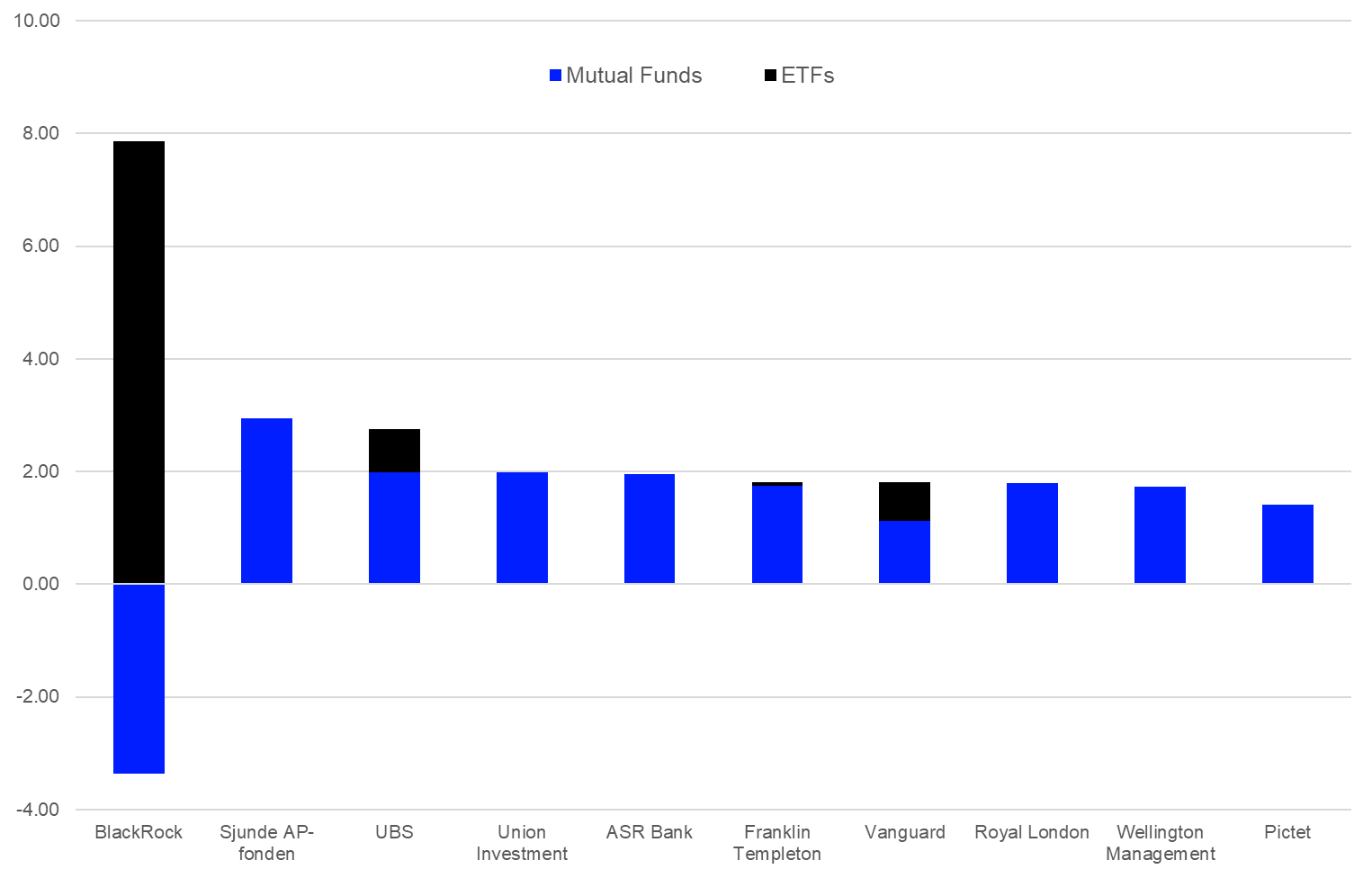

BlackRock (+€4.5 bn) was the best-selling fund promoter in Europe for September, ahead of Sjunde AP-fonden (+€3.0 bn), UBS (+€2.8 bn), Union Investment (+€2.0 bn), and ASR Bank (+€2.0 bn). Given the product ranges of the top five promoters and the overall fund flow trends, it was not surprising to see that ETFs played a vital role for the position of BlackRock in the table of the 10 best-selling fund promoters in Europe.

With regard to the overall flow pattern at the promoter level, it is noteworthy that the flows for BlackRock (-€15.4 bn) have been impacted by the outflows from money market products.

Graph 4: Ten Best-Selling Fund Promoters in Europe, September 2021 (Euro Billions)

Source: Refinitiv Lipper

Considering the single-asset classes, BlackRock (+€3.7 bn) was the best-selling promoter of bond funds, followed by UBS (+€3.4 bn), Pimco (+€1.2 bn), Vanguard (+€0.6 bn), and JPMorgan (+€0.5 bn).

Within the equity space, BlackRock (+€8.2 bn) led the table, followed by Franklin Templeton (+€2.3 bn), ASR Bank (+€1.7 bn), Goldman Sachs (+€1.6 bn), and Amundi (+€1.4 bn).

Allianz (+€1.3 bn) was the leading promoter of mixed-assets funds in Europe, followed by Union Investment (+€1.0 bn), Argenta (+€0.9 bn), Scottish Widows (+€0.7 bn), and DWS Group (+€0.6 bn).

Sjunde AP-fonden (+€2.9 bn) was the leading promoter of alternative UCITS funds for the month, followed by Wellington Management (+€1.2 bn), Insight (+€0.5 bn), DWS Group (+€0.4 bn), and Aegon Asset Management (+€0.4 bn).

Fund Flows by Fund Domiciles

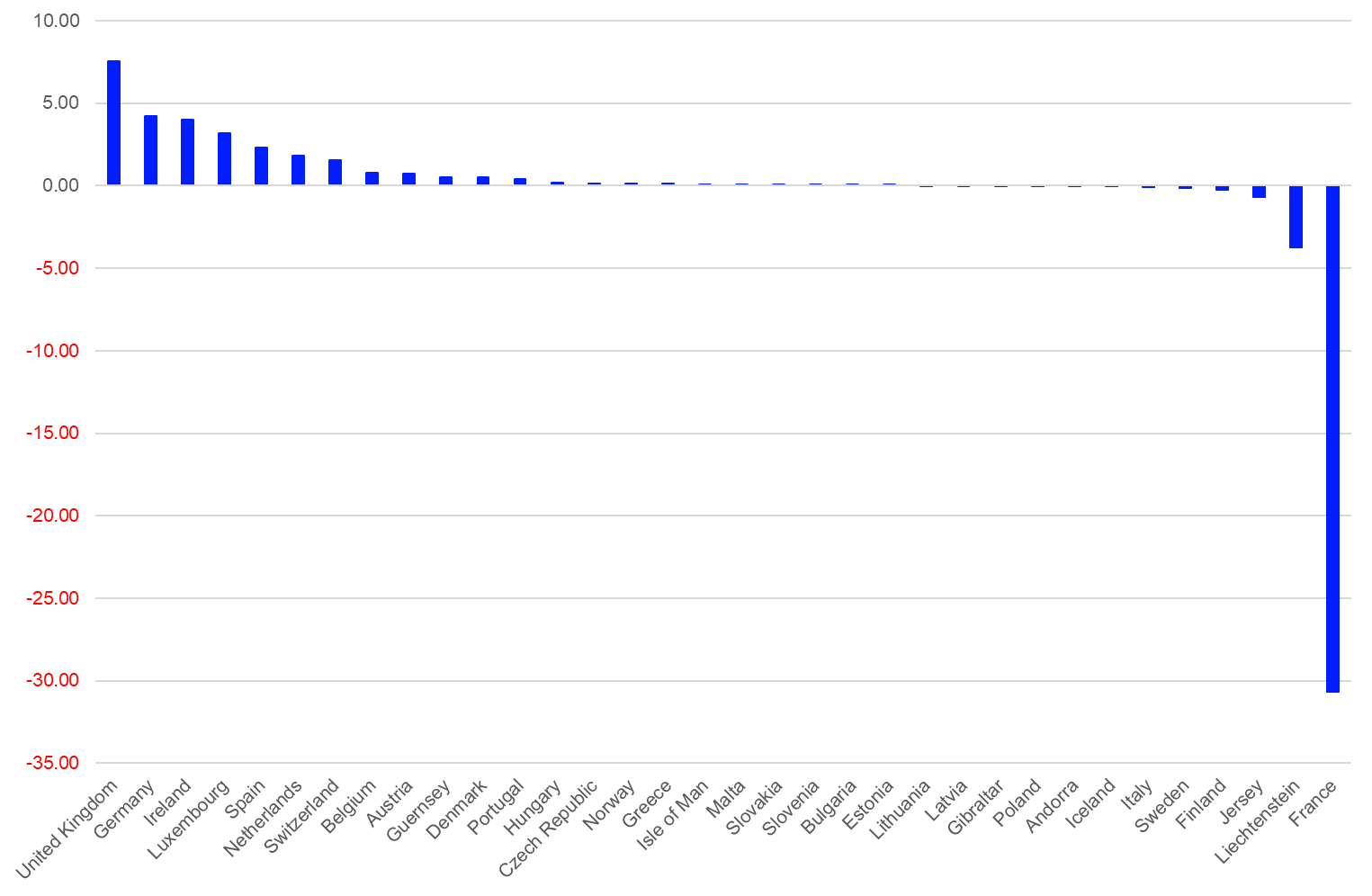

Single-fund domicile flows (including those to money market products) showed, in general, a positive picture during September. Twenty-two of the 34 markets covered in this report showed estimated net inflows, and 12 showed net outflows. The UK (+€7.6 bn) was the fund domicile with the highest net inflows, followed by Germany (+€4.2 bn), Ireland (+€4.0 bn), Luxembourg (+€3.2 bn), and Spain (+€2.3 bn). On the other side of the table, France (-€30.7 bn) was the fund domicile with the highest outflows, bettered by Liechtenstein (-€3.7 bn) and Jersey (-€0.7 bn). It is noteworthy that the fund flows for Luxembourg (-€14.2 bn), Ireland (-€14.7 bn), and France (-€29.2 bn) were impacted by the outflows within the money market segment.

Graph 5: Estimated Net Sales by Fund Domiciles, August 2021 (Euro Billions)

Source: Refinitiv Lipper

Within the bond sector, funds domiciled in Ireland (+€8.6 bn) led the table, followed by Luxembourg (+€3.1 bn), Switzerland (+€1.7 bn), Sweden (+€0.6 bn), and Belgium (+€0.6 bn). Bond funds domiciled in Liechtenstein (-€0.9 bn), Italy (-€0.2 bn), and Finland (-€0.1 bn) were at the other end of the table.

For equity funds, products domiciled in Ireland (+€9.3 bn) led the table for the month, followed by Luxembourg (+€4.8 bn), the UK (+€4.7 bn), the Netherlands (+€1.5 bn), and Germany (+€1.3 bn). Meanwhile, Liechtenstein (-€2.8 bn), Sweden (-€1.6 bn), and Belgium (-€1.1 bn) were the domiciles with the highest estimated net outflows from equity funds.

Regarding mixed-assets products, Luxembourg (+€6.2 bn) was the domicile with the highest estimated net inflows, followed by Spain (+€1.7 bn), Germany (+€1.4 bn), the UK (+€1.0 bn), and Austria (+€0.5 bn). In contrast, Jersey (-€0.3 bn), Poland (-€0.02 bn), and Andorra (-€0.01 bn) were the domiciles with the highest estimated net outflows from mixed-assets funds.

Luxembourg (+€3.4 bn) was the domicile with the highest estimated net inflows into alternative UCITS funds for the month, followed by Ireland (+€0.7 bn) and Germany (+€0.2 bn). Meanwhile, France (-€0.7 bn), Italy (-€0.2 bn), and the Netherlands (-€0.1 bn) were at the other end of the table.

The views expressed are the views of the author, not necessarily those of Lipper or Refinitiv.