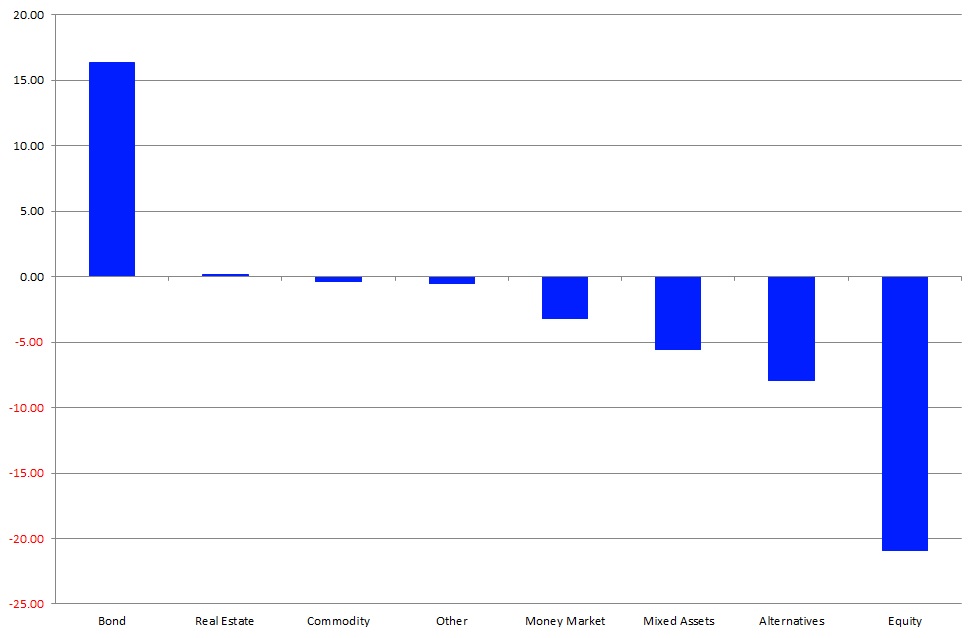

The negative trend with regard to fund flows in Europe continued in March even as the securities markets rebounded. As a consequence, March was the eleventh month in a row long-term mutual funds posted net outflows after 16 consecutive months of net inflows. Given the current interest rate environment, it was surprising that bond funds (+€16.4 bn) were once again the best-selling asset type in the segment of long-term mutual funds, followed by real estate funds (+€0.1 bn). All other asset types faced outflows: equity funds (-€20.9 bn), alternative UCITS funds (-€7.9 bn), mixed-asset funds (-€5.5 bn), “other” funds (-€0.5 bn), and commodity funds (-€0.4 bn).

These fund flows added up to overall net outflows of €18.8 bn from long-term investment funds for March. ETFs contributed inflows of €5.5 bn to these flows.

Money Market Products

Within the current environment, European investors continued to sell money market products. As a result, money market funds witnessed net outflows of €3.2 bn for March. ETFs investing in money market instruments contributed net outflows of €0.3 bn to these flows.

This flow pattern led the overall fund flows experienced by mutual funds in Europe to overall net outflows of €22.0 bn for March, and outflows of €58.3 bn for 2019 year to date.

Money Market Products by Sector

Money Market GBP (+€8.5 bn) was the best-selling sector overall. Money Market Global (+€0.4 bn), Money Market Other (+€0.2 bn), Money Market JPY (+€0.1 bn), and Money Market NOK (+€0.1 bn) rounded out the five best-selling sectors in the money market segment for March. At the other end of the spectrum, Money Market EUR (-€6.4 bn) suffered the highest net outflows overall, bettered by Money Market USD (-€5.5 bn) and Money Market EUR Leveraged (-€0.6 bn). Comparing this flow pattern with the flow pattern for February showed European investors further reduced their positions in the U.S. dollar and changed their opinion on the British pound sterling versus the euro. These shifts might have been caused by asset allocation decisions, as well as other reasons, such as for cash dividends or cash payments since money market funds are also used by corporations as replacements for cash accounts.

Graph 1: Estimated Net Sales by Asset Type, March 2019 (Euro Billions)

Source: Lipper at Refinitiv

Fund Flows by Sectors

Within the segment of long-term mutual funds, Bond Global USD Hedged (+€3.5 bn) was the best-selling sector, followed by Bond Emerging Markets Global in Hard Currencies (+€3.4 bn). Bond EUR Corporates (+€2.9 bn) was the third best-selling sector, followed by Bond EUR (+€1.9 bn) and Bond Global (+€1.8 bn).

Graph 2: Ten Top Sectors, March 2019 (Euro Billions)

Source: Lipper at Refinitiv

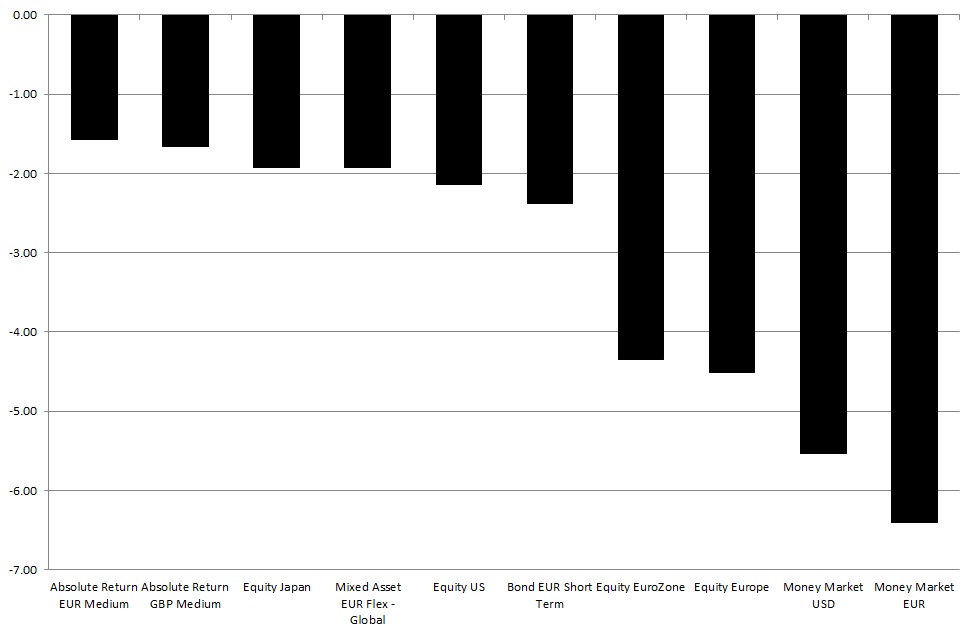

At the other end of the spectrum, Equity Europe (-€4.5 bn) suffered the highest net outflows from long-term mutual funds, bettered by Equity Eurozone (-€4.3 bn), Bond EUR Short Term (-€2.4 bn), Equity US (-€2.1 bn), and Mixed Asset EUR Flexible – Global (-€1.9 bn).

Graph 3: Ten Bottom Sectors, March 2019 (Euro Billions)

Source: Lipper at Refinitiv

Fund Flows by Markets (Fund Domiciles)

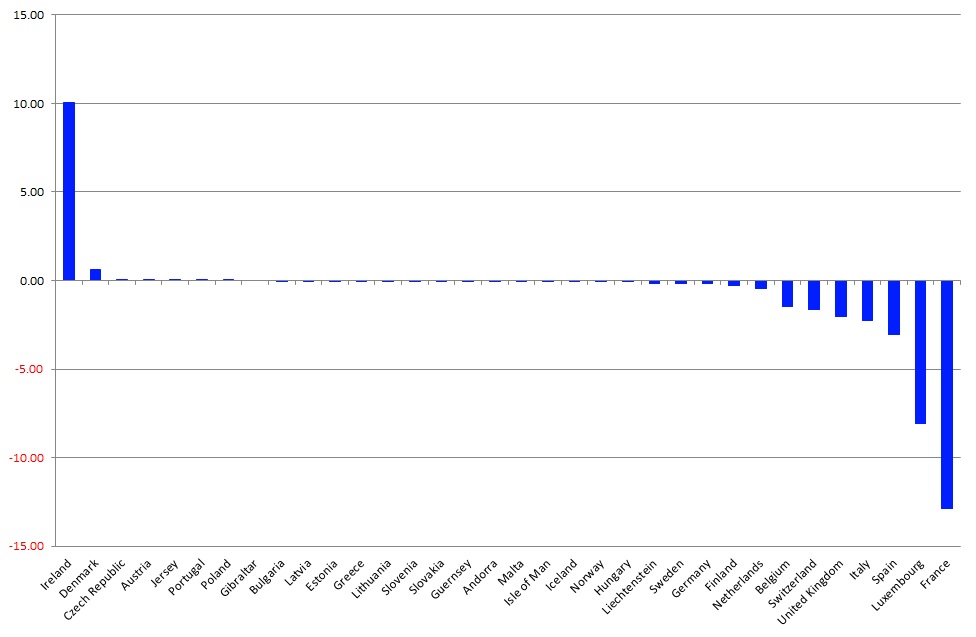

Single-fund domicile flows (including those to money market products) showed, in general, a negative picture for March, with only eight of the 34 markets covered in this report showing net inflows and 26 showing net outflows. Ireland (+10.0 bn)—driven by money market products (+€4.8 bn)—was the fund domicile with the highest net inflows, followed by Denmark (+€0.6 bn), Czech Republic (+€0.1 bn), Austria (+€0.1 bn), and Jersey (+€0.03 bn). On the other side of the table, France (-€12.9 bn)—driven by money market funds (-€7.5 bn)—was the fund domicile with the highest outflows, bettered by Luxembourg (-€8.1 bn) and Spain (-€3.1 bn).

Graph 4: Estimated Net Sales by Fund Domiciles, March 2019 (Euro Billions)

Source: Lipper at Refinitiv

Within the bond sector, funds domiciled in Luxembourg (+€9.7 bn) led the table, followed by Ireland (+€9.1 bn), Norway (+€0.4 bn), Denmark (+€0.4 bn), and Sweden (+€0.4 bn). Bond funds domiciled in Spain (-€1.6 bn), France (-€0.9 bn), and Italy (-€0.5 bn) were at the other end of the table.

For equity funds, products domiciled in Germany (+€0.4 bn) led the table for March, followed by funds domiciled in Denmark (+€0.2 bn), Austria (+€0.1 bn), Portugal (+€0.01 bn), and Guernsey (+€0.01 bn). Meanwhile, Luxembourg (-€11.4 bn), France (-€2.8 bn), and Ireland (-€2.0 bn) were the domiciles with the highest net outflows from equity funds.

In regard to mixed-asset products, the U.K. (+€0.3 bn) was the domicile with the highest net inflows, followed by funds domiciled in Austria (+€0.1 bn), Germany (+€0.1 bn), Denmark (+€0.02 bn), and Portugal (+€0.02 bn). In contrast, Luxembourg (-€2.9 bn), France (-€1.1 bn), and Italy (-€1.1 bn) were the domiciles with the highest net outflows from mixed-asset funds.

Switzerland (+€0.1 bn) was the domicile with the highest net inflows into alternative UCITS funds for March, followed by Belgium (+€0.01 bn), Finland (+€0.01 bn), Austria (+€0.004 bn), and Andorra (+€0.001 bn). Meanwhile, Luxembourg (-€3.1 bn), the U.K. (-€1.8 bn), and Ireland (-€1.2 bn) were at the other end of the table.

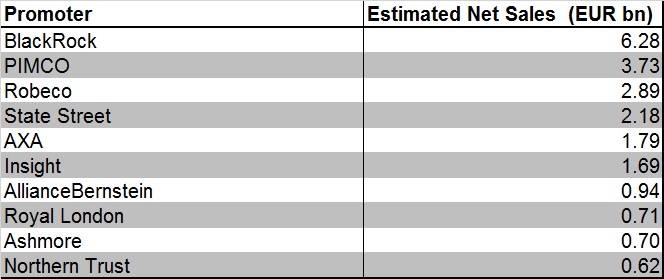

Fund Flows by Promoters

BlackRock was the best-selling fund promoter for March overall—driven by money market products (+€4.4 bn)—with net sales of €6.3 bn, ahead of PIMCO (+€3.7 bn) and Robeco (+€2.9 bn).

Table 1: Ten Best Selling Promoters, March 2019 (Euro Billions)

Source: Lipper at Refinitiv

Considering the single-asset classes, BlackRock (+€4.0 bn) was the best-selling promoter of bond funds, followed by PIMCO (+€3.9 bn), UBS (+€1.4 bn), AB (+€1.2 bn), and Vanguard Group (+€0.9 bn).

Within the equity space, Robeco (+€2.0 bn) led the table, followed by Union Investment (+€1.2 bn), Lindsell Train (+€0.3 bn), Eastspring (+€0.3 bn), and Jyske Invest (+€0.3 bn).

Flossbach von Storch (+€0.3 bn) was the leading promoter of mixed-asset funds in Europe, followed by La Caixa (+€0.2 bn), Union Investment (+€0.2 bn), JP Morgan (+€0.2 bn), and Aberdeen Standard Investments (+€0.2 bn).

BMO (+€0.2 bn) was the leading promoter of alternative UCITS funds for the month, followed by Flossbach von Storch (+€0.1 bn), DWS Group (+€0.1 bn), Mercer (+€0.1 bn), and PIMCO (+€0.1 bn).

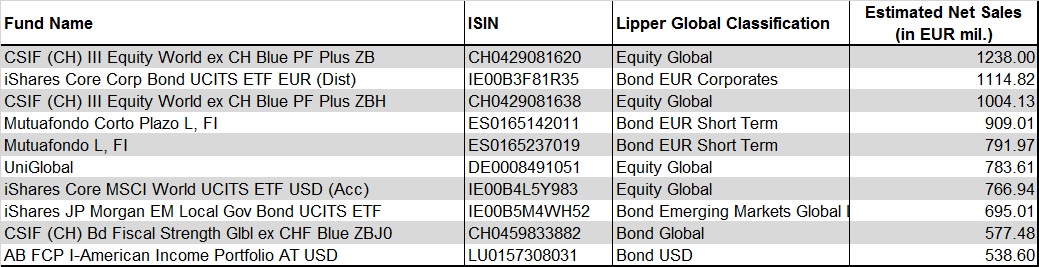

Best-Selling Funds

The 10 best-selling long-term funds gathered at the share-class level total net inflows of €8.4 bn for March. Bond funds dominated the ranking of the asset types with regard to the 10 best-selling funds (+€4.6 bn), followed by equity funds (+€3.8 bn).

Table 2: Ten Best Selling Long-Term Funds, March 2019 (Euro Millions)

Source: Lipper at Refinitiv

The views expressed are the views of the author, not necessarily those of Lipper or Refinitiv.