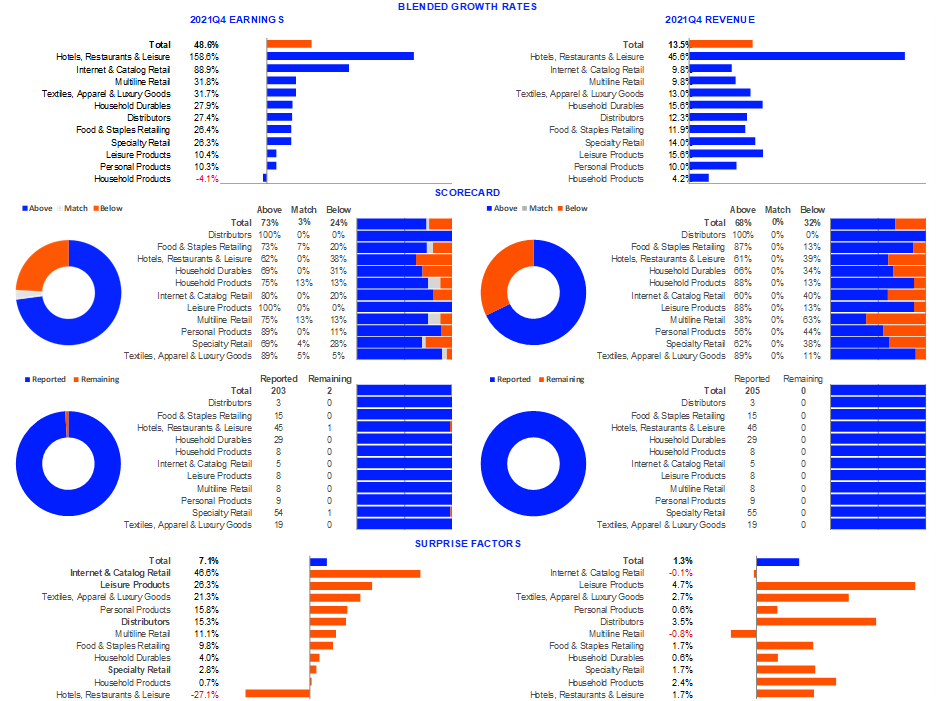

Ninety-nine percent of companies in our Retail/Restaurant Index have reported Q4 2021 EPS. Of the 203 companies in the index that have reported earnings to date, 73% have reported earnings above analyst expectations, 3% matched and 24% reported earnings below analyst expectations. The Q4 2021 blended earnings growth estimate is 48.6%.

The Q4 2021 blended revenue growth estimate is 13.5%. Sixty eight percent have reported revenue above analyst expectations, and 32% reported revenue below analyst expectations.

Exhibit 1: Refinitiv Earnings Dashboard

Source: I/B/E/S data from Refinitiv

Lululemon Q4 2021 earnings

Lululemon reported stronger-than-expected earnings but missed revenue expectations. Still, revenue grew 23.1% from a year-ago, despite supply chain issues, higher commodity, shipping and rising labor costs. Its e-commerce sales business grew 16% on top of difficult comparisons from a year ago of 92%. Its e-commerce business accounts for nearly half of its total revenue (49.6% of sales).

Moreover, Lululemon saw traffic increase 50% in the fourth quarter. This momentum continued into the first quarter. As a result, the company is very optimistic for its 2022 performance. Lululemon’s guidance “calls for 24% to 26% top line growth and 19% to 23% adjusted EPS growth” for Q1 2022 (Source: Lululemon Q4 2021 Earnings Call).

The growth story at Lululemon is compelling. They are now expanding into tennis and golf apparel, which is an opportunity to gain even more market share. Their menswear revenue grew 28%, outperforming its womenswear revenue growth of 20%, on a 2-year CAGR basis. They continue to expand internationally, with a plan to open 40 new stores globally in 2022.

Still, Lululemon acknowledged that they are still experiencing delays across their global network, mostly related to ocean transportation. As a result, the retailer will continue to lean mostly on air freight, which will help avoid low inventory levels.

What’s more, earnings are of good quality. According to the StarMine Earnings Quality model, the company scores a 93 out of a possible 100. Its high score suggests that profits could be from sustainable sources. The company’s cash flow and operating efficiency components also suggest the company is a top performer in these areas.

Exhibit 2: Lululemon StarMine Earnings Quality Model Score

Source: Eikon

Athleisure market

Athleisure is here to stay. Analysts polled by Refinitiv are bullish on the trend, especially given that many are still working from home. Both Nike and Lululemon continue to see revenue growth and are projected to continue seeing growth in 2022.

Exhibit 3: Athleisure Revenue and Net Income Results: 2019 – 2021

Source: Refinitiv I/B/E/S